DailyFX.com -

Talking Points

- With US equity markets plunging this week, financial news media has been quick to point

out movement in the bond market as the key catalyst.

- Certain measures of the US Treasury yield curve have started to invert, sparking fears

that the US economy is heading towards a recession within the next two years.

- However, the two key yield spreads that traders need to watch – the 3m5s and 2s10s – have

yet to invert, so recession fears should be contained for now.

See the DailyFX Economic Calendar and see what live coverage for key event

risk impacting FX markets is scheduled for next week on the DailyFX Webinar Calendar.

US equity markets have been struggling the past few days, with a variety of reasons being

offered up: Brexit; the US-China trade war; and the Federal Reserve’s rate hike path, among others. But a new explanation has

appeared in recent days, one that has yet to make an appearance in 2018, or really at any point in the past decade: the inversion

of the US Treasury yield curve.

Why Do Investors Look at the Yield Curve?

The yield curve, if it’s based on AA-rated corporate bonds, German Bunds, or US Treasuries, is

a reflection of the relationship between risk and time for debt at various maturities. A “normal” yield curve is one in which

shorter-term debt instruments have a lower yield than longer-term debt instruments. Why? Put simply, it’s more difficult to predict

events the further out into the future you go; investors need to be compenstated for this additional risk with higher yields. This

relationship produces a positive sloping yield curve.

When looking at a government bond yield curve (like Bunds or Treasuries), various assessments

about the state of the economy can be made at any point in time. Are short-end rates rising rapidly? This could mean that the Fed

is signaling a rate hike is coming soon. Or, that there are funding concerns for the federal government. Have long-end rates

dropped sharply? This could mean that growth expectations are falling. Or, it could mean that sovereign credit risk is receding.

Context obviously matters.

Does the US Treasury Yield Curve Inversion Matter?

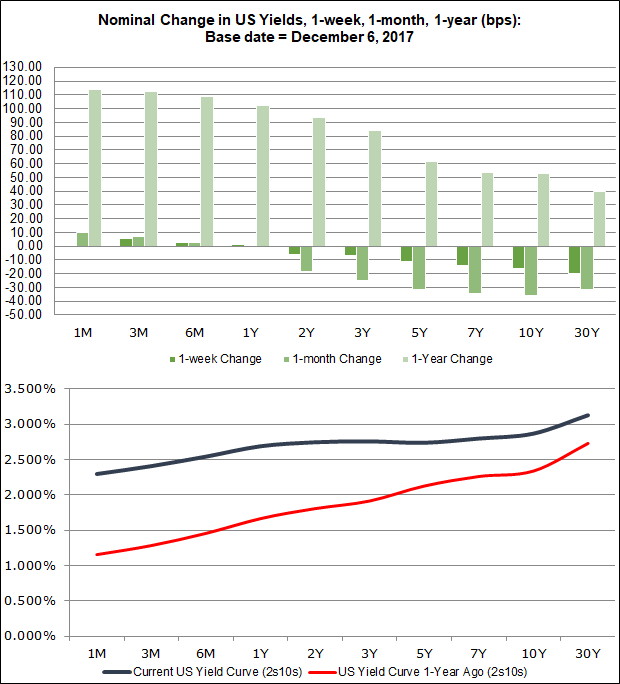

It’s true that part of the US Treasury yield curve started to invert this week. We’ve seen

both 2- and 3-year yields rise above 5-year yields. The “flattening” of the yield curve over the past year, predating this week’s

inversion, is rather apparent when comparing the shape of the yield curve today relative to that from last December:

US Treasury Yield Curve (December 6, 2018) (Table 1)

The knee-jerk reaction by many market participants, but mainly financial news media, has been

to declare the inversion of the US Treasury yield curve as a harbinger of a forthcoming recession. The stats speak for themselves:

yield curve inversions predict recessions (more on this shortly).

While there are certainly good reasons for concern – the US-China trade war, the fading

impulse of fiscal stimulus from the Trump tax plan, a housing market that is looking weaker amid higher interes rates – its best to

take a step back.

Let’s Ask the Professor

Amid all of the talk about the US Treasury yield curve inverting this week, the Duke

University finance professor who is the godfather of yield curve analysis (his 1986 dissertation explored the concept of using the

yield curve to forecast recessions) gave an interview to NPR (which can be listened to here). Professor Campbell Harvey made

a few key points regarding the yield curve inversion which traders should take to heart:

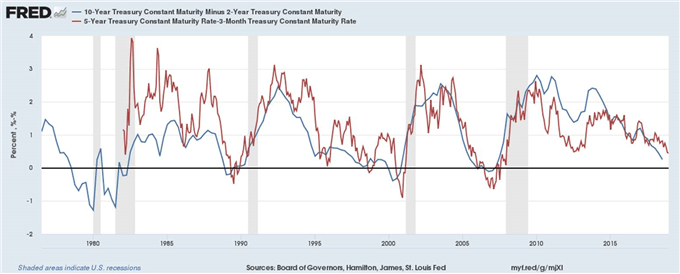

1) The model Harvey used initially looked at the 3-month, 5-year spread (3m5s), and

conventional wisdom points to the 2-year, 10-year (2s10s) spread as the yield curve; all of the concern this week about the 2-year,

5-year (2s5s) and 3-year, 5-year (3s5s) spreads inverting did not interest him, given that they as shorter-maturity instruments

didn’t qualify as “short-term” enough in his model;

US Treasury Yield Curves: 3m5s and 2s10 (1975 to 2018) (Chart 1)

2) The yield curve inversions being discussed now are not significant. According to his

research, the yield curve needs to invert for at least one full quarter (or three months) in order to give a true predictive signal

(since the 1960s, a full quarter of inversion has predicted every recession correctly);

3) Regardless of the 3m5s and 2s10s curves not inverting this week, Harvey still believes the

period of aggressive flattening is significant and it the yield curve is

signaling slower economic growth for the US, but not yet a

recession.

Read more: US Dollar Unable to Rally Even as Risk Appetite Erodes

--- Written by Christopher Vecchio, CFA, Senior Currency Strategist

To contact Christopher Vecchio, e-mailcvecchio@dailyfx.com

Follow him on Twitter at@CVecchioFX

View our long-term forecasts with theDailyFX Trading

Guides

original

source

DailyFX provides forex news and

technical analysis on the trends that influence the global currency markets.

Learn forex trading with a free practice account and trading charts from IG.