For several years, there has been a growing chorus in the mining industry that the next bull market for the uranium sector was (is) overdue. That chorus is now reaching a crescendo, and it’s based upon supply/demand parameters that are stark and unequivocal.

For several years, there has been a growing chorus in the mining industry that the next bull market for the uranium sector was (is) overdue. That chorus is now reaching a crescendo, and it’s based upon supply/demand parameters that are stark and unequivocal.

Adding additional complexity and opportunity to this equation is a major political “wildcard”. More on that later.

Massive supply/demand imbalance

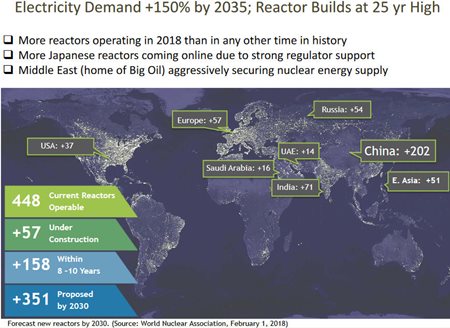

On the demand side, there are currently more nuclear reactors in operation globally than at any other time. But the real story with uranium demand is the future growth in the nuclear industry that has already been telegraphed.

(click to enlarge)

Even if all of these plans/proposals don’t come to fruition, the nuclear industry is projecting to double in size – by as early as 2030. Those demand parameters alone are enough to get the attention of any serious mining investor. However, the supply side of this equation is equally significant.

As the nuclear industry is entering an unprecedented growth phase, supply isn’t growing along with this. In fact, the mine supply of uranium has been shrinking. It’s not only marginal uranium operations that have been coming off line.

Some of the largest (and highest-grade) mines for some of the world’s largest uranium producers have been mothballed in recent years. Perhaps the highest profile announcement in this respect was Cameco’s closure of its huge McArthur River/Key Lake uranium mine – one of the world’s highest-grade uranium operations, that took effect in January 2018. Restarting production in these operations is neither fast nor cheap.

(click to enlarge)

Uranium demand is high and projected to increase dramatically. Supply is falling because prices are so low that some of the world’s most robust uranium operations are unable to break even at current, rock-bottom levels. The world needs much more uranium and the only way that this additional supply can be brought on line is at much higher prices for U3O8.

That’s the Big Picture for the uranium market. Experienced mining investors can clearly see the opportunity implied by these extremely lop-sided supply/demand fundamentals. So where is the “wildcard”?

U.S. Commerce Department investigation

This wildcard actually has two dimensions, with the first one at the political level. By now, any mining investor who has been following the uranium industry will be aware of new political rumblings from the U.S. government with respect to uranium imports into the United States.

A Reuters headline from July 2018 encapsulates this subject:

U.S. Commerce launches national security probe into uranium imports

There are several reasons why investors can and should take serious heed of this news. First, the Trump government has already initiated protectionist measures that have affected dozens of different sectors – and seriously altered supply/demand parameters in some of them.

Attaching an additional exclamation point to this headline is that this probe is framed in “national security” terms. Some of the largest exporters of refined uranium to the U.S. are governments with whom the United States now has frosty diplomatic relations.

Sources and shares of U.S. purchases of uranium produced in foreign countries in 2017:

- Canada–35%

- Australia–20%

- Russia–18%

- Kazakhstan–12%

- Uzbekistan–5%

- Hungary, Malawi, Namibia, Niger, South Africa, Ukraine, and unknown–10%

[source: U.S. Energy Information Administration]

Some investors may look at this news and immediately view this as a threat to all uranium imports into the U.S. However, that is an overly alarmist (and simplistic) position.

The reality is that even if the United States announced a new national objective of “uranium independence” as a result of this Commerce Department probe, at best this would be a long-term policy initiative for the U.S. nuclear industry. It could never be a near-term reality.

Understanding this requires an internal look at the U.S. nuclear industry. It’s a picture that can be summarized in one word: dependence. This is immediately apparent via a quote from the previous Reuters article.

[U.S. Commerce Secretary Wilbur] Ross added that the U.S. production of uranium has fallen to 5 percent of U.S. consumption needs from 49 percent in 1987. [emphasis mine]

[U.S. Commerce Secretary Wilbur] Ross added that the U.S. production of uranium has fallen to 5 percent of U.S. consumption needs from 49 percent in 1987. [emphasis mine]

The equation here is pretty simple. The U.S. presently gets 1/20th of the uranium it consumes from domestic sources and two, new nuclear reactors are under construction. The U.S. is already the world’s largest producer of nuclear energy.

This makes the United States the largest consumer of yellowcake. Meanwhile, developing a uranium mine in the United States involves navigating through a labyrinth of different bureaucracies – with competing agendas and extremely protracted review processes.

While a few smaller uranium projects in the United States are near or ready to go into production, this represents a drop in the bucket in meeting the U.S.’s enormous supply deficit. If the Commerce Department finds there is a “national security threat” here and recommends curtailing imports from some of the U.S.’s major external suppliers, what then?

Canada: the supply solution for the U.S. nuclear industry

It doesn’t require a skilled detective or market genius to predict where the United States will look if it suddenly needs a huge, new source of uranium supply, over (at least) the short and medium term.

Canada is close. Canada is friendly. Not only does Canada have large (known) uranium resources, but this country boasts many of the world’s richest deposits of uranium, with most of those deposits occurring in the world-famous Athabasca Basin of northern Saskatchewan.

Start with a uranium market that has a serious supply/demand imbalance. Throw in a wildcard that could skew this equation much more dramatically for the world’s single-largest uranium market. What does it add up to?

If the Commerce Department investigation finds there is a “national security threat” with respect to the U.S. supply of uranium (and don’t forget the U.S.’s large military demand for uranium) then this creates a government-driven imperative for much more U3O8 from “safe/friendly” sources. There is only one means of achieving such a supply objective over even the medium term: a separate, higher “U.S. price” for yellowcake to stimulate additional supply.

How high?

No one has been following the industry closer than the investment banking unit of Cantor Fitzgerald. It has been banging the drum for several years that the long-term “all-in sustaining cost” for U3O8 for the uranium industry is US$80 per pound. That forecast remains unchanged.

The most recent spot price quote for U3O8 was US$29.00 per pound. And even that anemic price is up substantially from earlier this year, where the price dipped briefly below US$20 per pound. This implies a long-term “U.S. price” for uranium of at least $80 per pound (and perhaps higher). More importantly, the near-term price necessary to bring sufficient additional supply online in Canada and the U.S. would need to approach that level.

Those parameters create the very possible scenario of a feeding frenzy within Canada’s Athabasca Basin – the most-obvious (only?) known source of yellowcake that could meet U.S. supply concerns over the medium term. For investors, the time to get in is before this scenario crystallizes and valuations have baked-in this higher price level.

One company that is already positioned for this imminent scenario is Fission 3.0 Corp. (TSX: V.FUU, OTCQB: FISOF, Forum). This uranium project generator offers four investment drivers to catch the attention of serious mining investors:

- A deep (and award-winning) management team

- A large “property bank” of prospective uranium properties in the Athabasca Basin

- Near-term, blue sky potential with its “Patterson Lake North” uranium project

- Strong institutional support

Investors wanting to get a closer look at Fission 3.0 will soon have their opportunity. Stockhouse will be presenting a full-length feature article on this Company early in the New Year.

www.fission3corp.com

FULL DISCLOSURE: Fission 3.0 Corp. is a paid client of Stockhouse Publishing.