RE:RE:RE: Mcreath is wrongfdfd12 wrote:

Go do the math that he did.

It is obvious he did it wrong.

I put the numbers.

Look at the Alpha article and just make substitutions

for the ration at 10 instead of 7.5 which is is now.

Very simple math.

Mcreath said I did the math but he did it wrong.

fdfd you got one over McCreath. Good on you. McCreath had a brain fart. Here is how Seekingalpha broke it down.

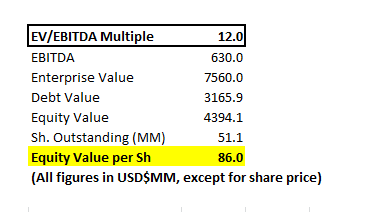

Base Case for a Concordia Buyout

I would use a 12x EBITDA to figure out the buyout price. This is below the 14x from the recent deals for reasons mentioned above.

The base case scenario indicates a buyout price of $86USD or around $112CAD for each Concordia share.

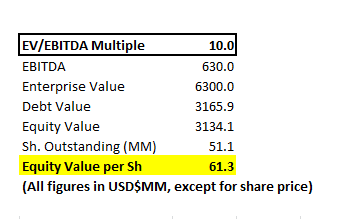

Worst Case for a Concordia Buyout

I think the worst case scenario would be a 10x EBITDA multiple. 10x would be considered a great deal for a private equity firm taking control of an entire company. We haven't seen such a low multiple since the last financial crisis.

$61USD or $80CAD is likely to be the floor that Blackstone would pay for Concordia shares.