Emerging Markets Still Undervalued, Global Capital

Economics / Emerging MarketsAug 07, 2011 - 06:11 AM

By: John_Mauldin

As will be clear below, I had finished an earlier version of this week's e-letter, but the events of the last few minutes require a few paragraphs. As I write at the end of the letter, Bloomberg kept their satellite truck here in Maine, as they had got advance warning of the downgrade by S&P of US debt and wanted to interview a number of the economists here, including your humble analyst. I can't rewrite the letter at this late hour, but will send you additional comments on Monday. And you can go to www.bloomberg.com and see everyone's remarks, including mine. It will be there somewhere, they promise me.

As will be clear below, I had finished an earlier version of this week's e-letter, but the events of the last few minutes require a few paragraphs. As I write at the end of the letter, Bloomberg kept their satellite truck here in Maine, as they had got advance warning of the downgrade by S&P of US debt and wanted to interview a number of the economists here, including your humble analyst. I can't rewrite the letter at this late hour, but will send you additional comments on Monday. And you can go to www.bloomberg.com and see everyone's remarks, including mine. It will be there somewhere, they promise me.

And now, a few questions and observations are in order.

First, as I walked to the area where the Bloomberg was shooting to go on, Jim Bianco and John Silvia told me that S&P had downgraded the Fed. I laughed and said, "If you guys want to make me look like a fool on TV, you have to at least make up a credible lie." They kept insisting it was true. I finally asked Mike McKee of Bloomberg and Barry Ritholtz, who was on-air, if it was true. They claimed it was, too. I was still wondering if they were setting me up, but even Roubini (who wouldn't do that to me) said it was true.

So, if the Fed, which doesn't issue credit and can print money, can be downgraded because it holds AA+ debt, then why and how in hell can the ECB, which holds hundreds of billions of euros of the junk debt of Greece and Ireland and insolvent banks not be downgraded on Monday? And the Bank of Japan? REALLY? What are these guys smoking? Do we now downgrade GNMA? Of course. And the FDIC? What the hell will repos do on market open? The NY Fed says it won't affect anything. Don't ask me, I just work here. And how can you rate France AAA? And still give AA or more to Italy when the market is saying they are getting close to junk?

Side bet for Monday. This could make me look like an idiot, but I think treasury yields fall as the risk-off trade increases. Can this come at a worse time for a nervous market? By the way, maybe you want to go long Kimberly Clark, as they make Depends (the adult diapers here in the US, for my non-US readers), because sales are going to skyrocket all across the financial markets.

Can we say Endgame, gentle reader? Madness. And now on to the regular letter. More to follow Monday.

This week I write from Maine, where, when we landed in the float plane at Leen's Lodge in Grand Lake Stream on Thursday, we learned that the market had closed down 512 points. I was in the plane with Nouriel Roubini and Jim Bianco (plus a Fed official to be named later), where for whatever reason we could get reception on and off (no phone works at the lodge). We were just watching the market fall. It is fun to sit next to Roubini as a market crashes. He knows ALL the market crash jokes.

So, as is my normal routine for this fishing trip to Maine, I take the week off and invite a guest columnist in. This year it is Keith Fitz-Gerald, whom I have heard speak twice and have started reading. He has lived all over the world and spends a lot of the year in Japan, and is a true expert on emerging markets. I am a fan of investing in emerging markets (as I agree they are the future) but do not consider myself anywhere close to Keith's level of expertise. So this week we take a look at the case for emerging markets.

If you are interested in subscribing to Keith's letter and learning more about emerging markets, you can follow this link. It's fairly inexpensive and my readers get half off. Now, let's jump in, and I will end with some closing comments.

The Case for Going Global Is Stronger Than Ever

By Keith Fitz-Gerald Chief Investment Strategist, Money Map Press

If we have learned anything from the current financial mess, it's that building wealth is dependent on rational analysis, careful decision making, and risk management. That's why sticking close to home at a time when our markets are more uncertain than ever is a recipe for disaster and absolutely the wrong thing to do. Not only will you miss out on the world's fastest-growing markets, but the odds are exceptionally high that you will miss as much as 50% or more in potential returns over the next decade.

Don't get me wrong.

If you choose to "stay home" or go with what you know, which is what a lot of investors are doing right now, chances are you will probably do okay. After all, there will eventually be a U.S. economic recovery and a market rebound.

But know this.

You will have to watch others outperform you by 50%, 75%, even 100% or more - for years to come. Adding insult to injury, you'll have to deal with the ever-present knowledge that you could have been one of them.

If you can live with this, fine ... but most investors I know won't be able to.

The U.S. Markets Are Still In Trouble

Despite widespread belief inside the Beltway that the U.S. economy is on the mend, reality is that it's going to be a long time before U.S. markets return to normal - if there is such a thing anymore.

Our real estate markets are likely to be hobbled for a decade or longer, our consumers are badly scarred, chronic unemployment is likely to be a permanent fixture in the economic landscape for at least the next few years, and the personal deleveraging we're seeing as most Americans pull in their horns is really still in its infancy.

Factor in the evisceration of our national wealth, the debt debacle on both sides of the Atlantic, feckless leadership, and regulators who are trying to make up lost ground for having missed the crisis in formation, and we have a real witch's brew, the results of which cannot be understated, especially when it comes to capital markets.

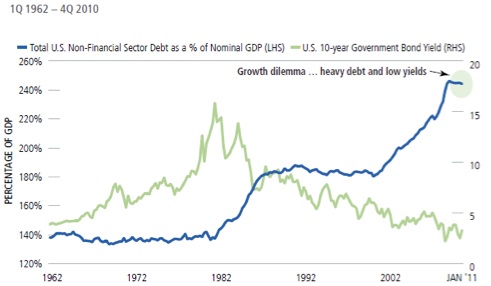

Government bond markets, as I have noted many times in presentations around the world, are pricing in slow-growth to no-growth expectations, as evidenced by the 10-year notes, which have historically reflected growth-rate expectations for the so-called developed world. This is especially problematic given the debt carried by the United States and most of its colleagues.

Figure 1: Source: Bloomberg, Federal Reserve Bank of St. Louis, Calamos.com

The numbers are even starker when viewed through the lense of forward-looking annual real yield on ten-year treasuries, which pencils out to a paltry 0.6%, assuming annualized inflation of 2.4% a year.

Obviously the inflation numbers are highly suspect, as is anything coming out of Washington these days, but this is what we've got to work with.

I find myself struck by a terrible sense of déjà vu, because the U.S. - debt deal or not - appears to be charting a course down the same troubled path Japan has trod since 1990, which is something I first noted in early 2000, based upon my first-hand experience in that nation.

Unfortunately, this path is likely to be characterized by the same problems: sovereign debt overburden that makes the Greeks look positively miserly, stagnant national wealth, and slow GDP growth despite trillions in "stimulus" that is unlikely to create any real returns whatsoever.

As bleak as this sounds, however, I also find myself salivating, because history shows that periods of great crisis are really just opportunities in disguise.

Case in point, many emerging markets are now emerging in name only. They've become "BEEs" or Big Emerging Economies, with superior risk-reward characteristics, newly unbridled consumer power, and - gasp - some element of adult supervision when it comes to fiscal fitness.

Not surprisingly, their bond markets are pricing in an entirely new set of expectations, 6%-9% growth, and capital markets that may exceed $300 trillion by 2025, according to proprietary research ... more than 60% of which will come from outside the established players of the United States, the EU, and Japan.

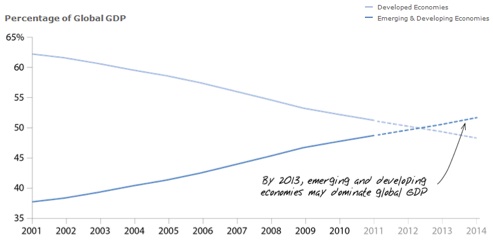

At a time when we are hamstrung by our own problems, this is hard to imagine. But it's not difficult to understand: since WWII, developed countries have contributed ever less to global growth.

It's not that we're falling off the map. In fact, quite the opposite is happening, and other nations are simply coming up to speed.

Figure 2: Source: PIMCO, Haver Analytics, IMF, FGRP

What's more, many of the same emerging markets we used to regard as little more than entertaining backwater trading partners are now some of the world's biggest foreign creditors. Virtually all have large reserves, and the importance of this development cannot be understated.

Here's why.

In contrast to years past, when a financial crisis would have erupted into a fiscal crisis, countries like China, Brazil, and others have seen their currencies strengthen. This makes their dollar-denominated debt easier to repay, especially as a creditor, because any weakness in the currency actually improves fiscal accounts.

At the same time, being a net external creditor gives emerging-market policy makers economic flexibility that simply wasn't possible a decade ago. As a result, many emerging economies, particularly the BEEs, can now provide a sort of countercyclical stimulus that is capable of stimulating domestic demand, even as they become less reliant on their exports. This is why China, for example, has not crashed and Brazil refuses to buckle.

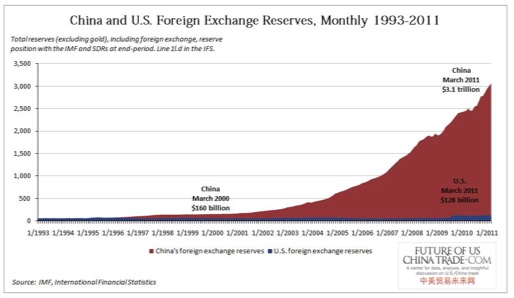

According to the International Monetary Fund, worldwide official foreign exchange holdings reached $9.69 trillion in the first quarter of 2011. That's a 17% increase year-over-year in aggregate.

As of the end of Q1 2011, total foreign exchange holdings by advanced economies were $3.16 trillion, and total foreign exchange holdings by emerging and developing economies were approximately double that, or $6.53 trillion.

If your jaw is not on the floor already, consider China. As of March 2011, China had $3.1 trillion in reserves all by itself, while the U.S. showed merely $128 billion in the proverbial piggy bank.

This means in no uncertain terms that some nations, like our own, have little or no wealth to draw upon while others could recapitalize their financial systems several times over and still have change left.

Undercapitalization Makes Emerging Economies More Efficient & Developed Economies Less Efficient

History shows that one of the single biggest drags on any economy is something I call overcapitalized infrastructure. What this means is that, dollar for dollar, there is so much money available that investments become a process of overallocation or overcapitalization. Or both.

In simple language, this means there's simply too much money chasing too few quality opportunities, so things tend to get bid up or overcapitalized in the process - like houses, cars, credit card debt, and mortgages. All of which are, in reality, generally depreciating assets that create nothing more than the illusion of profits for very short periods of time.

Under this scenario, labor productivity generally rises but capital productivity generally falls, which is why government analysts are flying blind ... they cannot tell the difference.

On the other hand, the BEEs and many emerging markets do not have such troubles. At least not yet.

If anything, they've got the reverse to contend with: extremely competitive labor that's fueled by a powerful combination of ambition and generally growing capital efficiency.

What's more, because they are starting from an incredibly low base, it doesn't take a lot to get them moving in the right direction. Many, in fact, are able to engineer a level of capital efficiency that far outstrips our own, led most notably by China, Brazil, and India. And, thanks to millions of underemployed people in low-productivity jobs, they have a huge human reservoir from which to draw for decades to come. We don't.

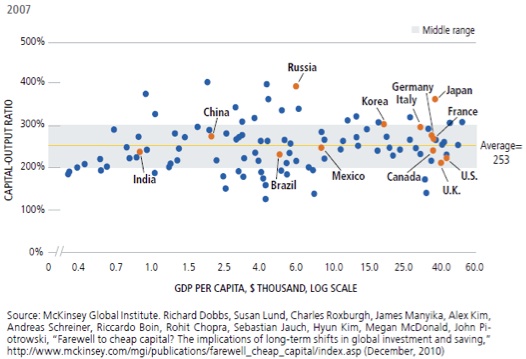

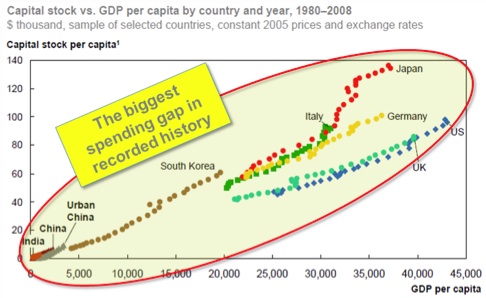

According to the McKinsey Global Institute, the average capital output worldwide by country is 253, meaning that it takes 253 dollars in capital stock to generate $100 of global GDP. A nation like China can achieve this with a GDP "investment" per capita of between $1,500-$2,500 per person, whereas the United States requires more than $40,000 and has a capital stock ratio of approximately 205%.

What this suggests is that high-GDP-per-capita nations require more money to maintain the same relative efficiency as nations with low GDP-per-capita ratios.

It's no wonder, then, that while the West is forced to contend with a proverbial albatross around our necks that's defined by sovereign debt and badly broken social contracts that nobody wants to relinquish, other nations are embarking on a grand runway of growth that will result in the greatest game of capital "catch-up" the world has ever seen.

Figure 3: Source: IMF, McKinsey & Co., FGRP

Emerging Markets Still Undervalued

Obviously this raises some interesting questions, especially when it comes to which markets may represent the best investment opportunities.

Here, too, the data is quite clear.

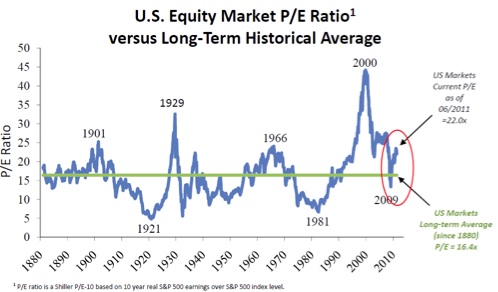

According to a July 2011 report from Investment Market Risk Metrics, US markets still appear overvalued, even though they are down substantially from other peaks over the last 131 years.

Figure 4: Source: Pension Consulting Alliance - Investment Market Risk Metrics

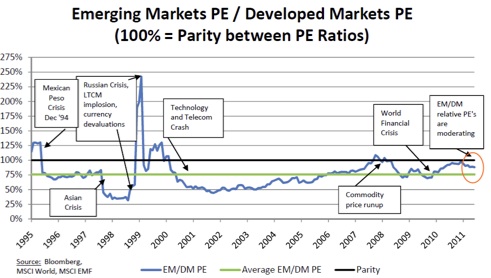

On the other hand, emerging markets still appear cheap. Granted they're not at the levels we witnessed in 2008-2009 or in the early 2000s, but one can make the argument they're undervalued even now. And therefore more worthy of investment than their Western counterparts.

Figure 5: Pension Consulting Alliance - Investment Market Risk Metrics

Global Capital Shift Is Accelerating

Against this backdrop, it's no wonder that money is leaving the nanny states of the West and headed to the Far East, as well as to nations that are backed at least partially by natural resources. This includes portions of the Middle East and South America, too.

In perhaps the ultimate irony, our own weak dollar policies, TARP, and QE2 have actually made this capital flight worse, because they have diminished the value of the dollar. So until Washington stops jawboning and actually does something productive that makes money feel welcome here, this will continue.

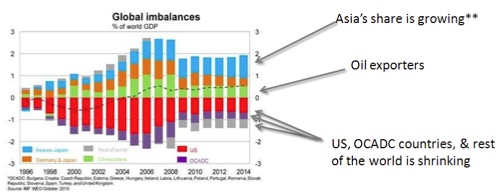

Many investors think this is new, but in reality it's just the continuation of a trend that began shortly after WWII, when approximately 75% of the world's economic activity took place within our borders. We just don't remember.

Today, that figure is reversed, and various sources estimate that as much as 75% of the world's daily economic activity now takes place outside our borders.

Some chalk this up to the myth of American industrial might and superiority. In reality we won by default, because the rest of the world was quite literally in ashes and hadn't yet taken the field.

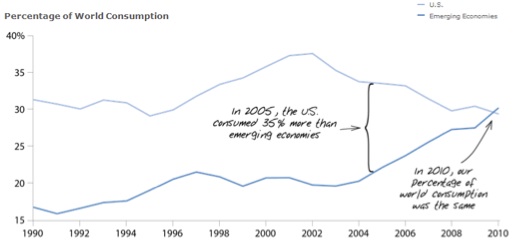

Now, however, they're ready to play, which is why the trend in global consumer spending looks like a ski jump, even as the United States' share of that is in decline or at best flatlining.

Figure 6: Source: PIMCO, Credit Suisse, FGRP, IMF

As to how things will look in a few innings, what we're dealing with is simply a numbers game, especially when it comes to consumption.

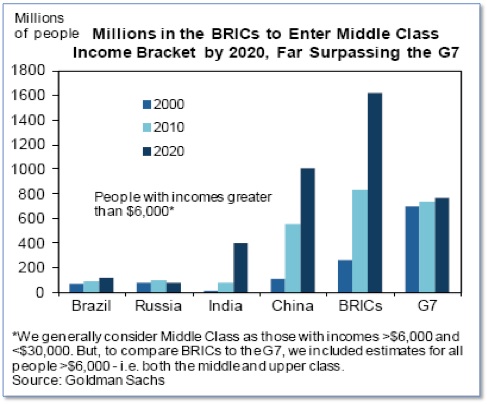

People forget, for example, that China's middle class alone is estimated to be more than 300 million people strong. Factor in India and much of South America and you are talking about an unprecedented increase in consumerism that may ultimately involve as many as 3 out of every 5 people alive on the planet today - that's entirely outside our borders.

The Biggest Growth Will Be in the Most Obvious Places (and Sectors)

When I look at the world of the past and the world of our future, some things jump out. Chief among them is the immediate effect that newly emerging nations will have on things the rest of us take for granted - like infrastructure and infrastructure-related holdings - which are among my top choices at the moment and have been since this crisis began.

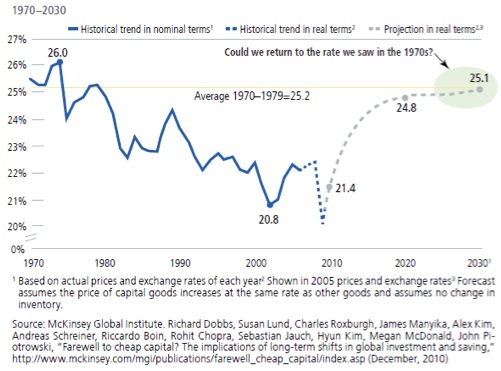

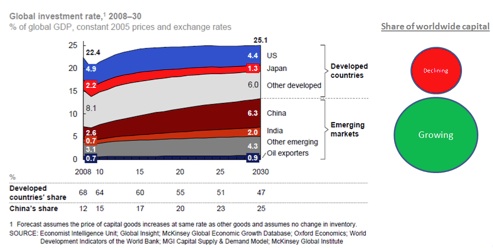

As recently as 1970, approximately 25% of global GDP was invested in infrastructure, which is defined as fixed assets and equipment by the McKinsey Global Institute. Not surprisingly, this declined to 20% in 2010, leading many analysts to mistakenly believe that global growth was slowing.

Figure 7: Global Investment Rate as a % of GDP, Calamos.com

Nothing could be farther from the truth.

What is actually happening is that the world is being split into a two-speed economy: those countries capable of creating high-productivity capital investments and those that cannot create such things absent huge, misguided stimulus programs and bailouts.

The former are much more attractive investments, because they are characterized by growth, while the latter should generally be avoided because they will be a drag on capital for decades to come, absent a complete simultaneous fiscal reset.

Generally speaking, this suggests moving away from American-, European-, and Japanese-centric choices and into companies that favor the faster growth of emerging markets and BEEs, regardless of where they are domiciled, i.e., on the NYSE, London, or Tokyo exchanges.

Doing so will help investors capitalize on burgeoning domestic growth while at least partially isolating their portfolios from the inevitable slowdowns and stagnant capital "stock" discussed above. It's worth noting that an increasingly large percentage of exports that were once bound for our shores are being refocused to other emerging markets, suggesting that future growth will be even less dependent on developed market stability than it is now, which is a pretty scary thought if you're not prepared for it.

By the numbers, this too is pretty straightforward.

Unfortunately, this is where it gets tricky and where we must depart from the past when it comes to our investments.

Conventional Diversification Won't Cut It Any Longer

For millions of investors, the very notion of diversification is appealing: to split your assets up so that no one decline will take everything down at once. Unfortunately, with everything going on now, this is like rearranging the deck chairs on the Titanic, and about as effective.

Today's financial markets need a concentration of assets that's characterized by significant emphasis on creditor nations versus debtor nations. At the same time, investors who don't want to get left far behind would be wise to fill their portfolios with companies I call the "glocals," or big multinational firms with strong "fortress" balance sheets, experienced managers, and globally recognized brands. Technology, connectivity, and indirect resource plays all come to mind here, as do dividends, which help offset the risks we take as a part of the investing process.

I also believe that investors want to generally be long resources and commodities for the foreseeable future. Both will be great places to hang out as the West comes apart, while also providing a meaningful inflation hedge. If things don't come apart, that's great, because they'll zoom higher on demand as it resumes.

And finally, I think investors who buy into the international growth that is our future will take advantage of a definite currency bias that will keep your money involved with the efficient capital countries while generally avoiding the slackers, except in very specific instances and only then with risk capital.

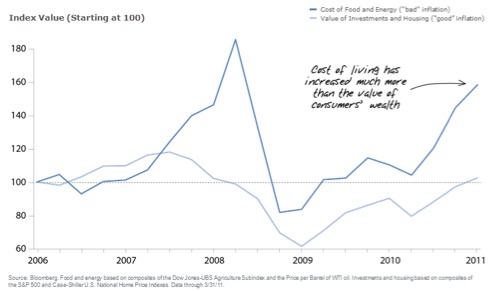

You can figure out pretty quickly which is which by looking at the cost of living versus value of investments. Anytime you see the former overwhelming the latter, it's time to go, as is the case for the United States and Europe now.

Figure 8: Source: PIMCO

Risks (and there are plenty)

No discussion on emerging markets would be complete without addressing the 800-pound gorilla in the room - China. Love it or hate it, that nation is on the move.

More bluntly, China will affect every investment class on the planet for the next 100 years, which is why investors would be wise to come to terms with it. I think the decision is pretty easy, even as it is pretty graphic: the Dragon is coming to lunch on Tuesday. The only decision you have to make is whether you and your money are going to be at the table or on the menu.

The same could be said about volatility. I think it's here to stay, particularly as our own demographic shift results in further currency debasement and inflationary pressure. You can't just wish away $202 trillion in unfunded liabilities, despite what those in our capital might think.

No matter which way you cut it, it's very simple, as I see it: the West (including Japan) faces severe structural imbalances that, when combined with limited willingness to deal with meaningful austerity, will hold it back for many years - which is why I'd rather go with growth any day.

In closing, I want to leave you with one more thought.

Even though we have talked extensively about why the case for emerging markets is stronger than ever, I am not a big fan of abandoning the U.S., which is what some of my colleagues advocate.

The United States is a nation filled with resilient, clever people; and despite the fact that the chips are down, I wouldn't bet against it.

We will find our way through this mess, even though the path we must take isn't clearly defined nor brightly lit ... yet.

Best regards for great investing,

Keith Fitz-Gerald