RE:RE:RE:RE:RE:RE:RE:RE:injection estimates Market Prices and Uncertainty Report

This is a regular monthly supplement to the EIA Short-Term Energy Outlook.

Contact: James Preciado (James.Preciado@eia.gov)

Full Report

Crude Oil

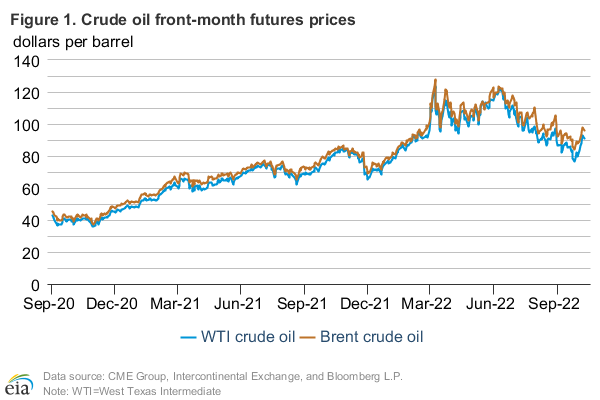

Prices: International crude oil prices, which reached their highest point of the year in June, fell to their lowest levels of the year in early August. The North Sea Brent front month futures price settled at $105.44/barrel on August 7, a decrease of $6.85/barrel from July 1 (Figure 1). The front month West Texas Intermediate (WTI) contract also fell, settling at $97.34/barrel on August 7, $8.00/barrel lower than on July 1.

A further easing of supply concerns and potentially softening demand combined to help loosen crude oil markets over the previous month. An agreement to open some Libyan ports to resume exports of crude made additional barrels available to the global market and applied downward pressure on light sweet crude oil prices. Low refinery runs in Asia and Europe capped demand for crude oil and expectations for global economic growth were revised lower compared to last month, remaining below growth rates projected at the start of 2014.

The front of the Brent and WTI futures curves diverged sharply in July, demonstrating the different set of factors driving these two markets. The 1st-3rd month futures price spread for Brent settled at -$1.09/bbl on August 7, a decline of $1.58/bbl from July 1 (Figure 2). It is the first time since 2011 that the Brent futures curve was in a consistent contango (when near-term price are less than longer-term ones) and shows an easing of tightness in the world waterborne market. It also indicates that global commercial crude oil inventories likely built in July.

In contrast, the U.S. domestic crude oil market tightened in July with backwardation (when near-term prices are greater than longer-term ones) in the front part of the WTI futures curve increasing to its highest level of the year. The 1st-3rd spread settled at $3.19/bbl on July 22, before declining to settle at $1.02/bbl on August 7. Cushing inventories fell for most of July, hitting their lowest point since 2008 for the week ending July 25 as U.S. refinery runs hit their seasonal peak. The recent decline in backwardation in the first week of August coincides with a decline in PADD 2 refinery throughput and a small build in Cushing, Oklahoma, inventories for the week ending August 1.

Crude production in the Permian Basin, the largest crude oil producing region in the United States, increased 0.23 million bbl/d from August 2013 to July 2014 to reach an estimated 1.6 million bbl/d. This has resulted in a growing spread between crude oil priced in West Texas and in Cushing, Oklahoma, as production exceeds pipeline take-away capacity. The average discount of crude oil priced in West Texas to WTI priced at Cushing, Oklahoma, increased by the largest amount from June to July since these benchmarks traded at parity in August 2013. WTI prices in Midland, Texas, averaged $11/barrel below WTI at Cushing in July, the second-largest discount on record (Figure 3). Similarly, West Texas Sour (WTS) crude priced in Midland, Texas, averaged $10/barrel lower than WTI at Cushing, the third-largest average monthly discount. In early summer, it was reported that the completion date of Magellan Midstream Partner's 300,000 bbl/d BridgeTex pipeline running from the Permian Basin to the Houston area was pushed back to September from its original completion date of mid-2014. Additionally, the Phillip 66's Borger refinery, which runs crude oil produced in West Texas, started a planned maintenance outage in mid-July. This combination of factors led to available crude oil further exceeding take-away capacity from West Texas and increased basis differentials.

Global demand for commodities: Two proxies for global demand of commodities declined in July. The Baltic Dry Index (BDI), published daily by the Baltic Exchange, serves as an assessment of the cost of shipping raw materials by sea. The BDI decreased by 14% from July 1 through August 7(Figure 4). The Dow Jones-UBS Commodity Index (DJ-UBSCI) is composed of exchange-traded futures for a diverse group of commodities including agriculture, energy, industrial metals, precious metals, and livestock. The DJ-UBSCI declined 5% from the beginning of July through the first week in August. Downward movements in either of these indexes generally reflect lower demand for raw materials and commodities—products that are closely tied to economic growth.

Some of the 7% drop in the price of Brent in July through the first week of August was a result of supply side risk premiums subsiding; however, the decreases in the BDI and DJ-UBSCI indexes may indicate that demand factors are also influencing international crude oil prices. If expectations for economic growth are lowered, crude oil prices will retreat accordingly to reflect subdued demand growth.

Volatility: Brent and WTI crude oil prices exhibited their largest realized price volatility for the year, measured by monthly trading ranges. The difference between the highest price and lowest price for the Brent front month futures contract in July was $8.44/bbl and the same range for WTI was $8.49/bbl. These were the largest monthly ranges since November and September of 2013, respectively (Figure 5).

Although implied volatility for the Brent and WTI futures contracts increased in July, it still remains less than prior 2014 levels and below levels from last November, in contrast with futures contract monthly trading ranges. Implied volatility for the front month Brent and WTI contracts settled at 15.7% and 17.1% on August 7, 3.0 and 3.9 percentage points higher than on July 1, respectively (Figure 6). Higher trading ranges with a subdued response in implied volatility suggests market participants do not expect recent volatility increases to extend into the future.

Market-Derived Probabilities: The November 2014 WTI futures contract averaged $96.28/barrel for the five trading days ending August 7 and has a probability of exceeding $100/barrel at expiration of 27%. The same contract for the five trading days ending July 1 had a probability of exceeding $100 of 71% (Figure 7). Because Brent prices are higher than WTI prices, the probability of Brent futures contracts expiring above the same dollar thresholds is higher.

Petroleum Products

Gasoline prices: TThe reformulated blendstock for oxygenate blending (RBOB, the petroleum component of gasoline) front month futures price declined by 26 cents per gallon (gal) from July 1 to settle at $2.77/gal on August 7 (Figure 8). The RBOB-Brent crack spread settled at 26 cents/gal on August 7, a decrease of 10 cents/gal since July 1.

TThe decline in crude oil prices in July contributed to the decline in gasoline prices; however, as shown by the decrease in the gasoline crack spread, fundamentals within the gasoline market also likely applied downward pressure on gasoline prices. U.S. refineries ran at record highs in July at 16.7 million bbl/d, an increase of 0.83 million bbl/d from June. This was the largest increase in refinery runs from June to July on record, helping to lower U.S. gasoline prices.

Backwardation in the gasoline futures curve showed a steeper decline than backwardation in the Brent crude oil futures curve over the last five weeks. The 1st-13th spread for gasoline declined by 16 cents/gal ($6.61/bbl) from July 1 to August 7 and reached its lowest point for the year in August(Figure 9). The 1st-13th spread for Brent only declined by $4.42/bbl over the same time. The flattening of the RBOB futures curve indicates a loosening gasoline market.

Heating Oil prices: The front month futures price for heating oil decreased 8 cents/gal from July 1, settling at $2.90/gal on August 7 (Figure 10). The heating oil-Brent crack spread increased 8 cents/gal to settle at 39 cents/gal on August 7.

Like gasoline, the decline in heating oil prices is attributable to the decline in crude oil prices but strength in the heating oil crack spread indicates some near-term tightness in the distillate market. U.S. distillate inventories were 125 million barrels as of August 1, lower by 1.5 million barrels compared to last July, and the eighth straight month of lower year-over-year inventory levels. At the same time, distillate consumption plus exports for the four weeks ending August 1 were 5.0 million bbl/d, an increase of 100,000 bbl/d from July 2013. The tightening in the distillate market and loosening of the gasoline market resulted to heating oil prices rising above gasoline prices on July 23 for the first time since May.

Volatility: Implied volatility for the front month RBOB contract and front month heating oil contract rose slightly by 1.1 percentage points and 0.7 percentage points, respectively, from July 1 to settle at 16.4% and 14.2%, respectively, on August 7 (Figure 11).

Market-Derived Probabilities: The November 2014 RBOB futures contract averaged $2.59/gal for the five trading days ending August 7 and has a 16% probability of exceeding $2.80/gal (typically leading to a retail price of $3.50/gal) at expiration. The same contract for the five trading days ending July 1 had a 49% probability of exceeding $2.80/gal (Figure 12).

Natural Gas

Prices: Natural gas prices reached their lowest point of the year ($3.47/MMBtu) with the expiration of the August futures contract on July 28 and marked the sixth straight week of declines in the front month futures price. The front month contract (September delivery) settled at $3.88/MMBtu on August 7, a decline of 58 cents/MMBtu compared to July 1. Cooling degree days were at or below normal for three consecutive weeks and below last year's levels for five weeks, averaging 13 cooling degree days below last year (Figure 13). Temperatures were particularly cool in areas where power burn can be high in the summer, such as Texas and the Southeast. Continued strong storage injections, averaging 92 billion cubic feet (bcf) per week in July, also weighed on U.S. natural gas prices. .

The recent declines in natural gas prices were not limited to near-term contracts. Prices for delivery of Henry Hub futures contracts in June 2015 and December 2015 declined by 24 cents/MMBtu and 19 cents/MMBtu, respectively, from July 1 to August 7 (Figure 14). The entire natural gas futures curve moving down suggests that some of the recent price declines are attributable to rising expectations for future U.S. natural gas production. In the August STEO, dry natural gas production in the United States is projected to be 69.8 bcf/d and 71.2 bcf/d in 2014 and 2015, respectively, and are 2 bcf/d and 2.6 bcf/d, respectively, higher than expectations at the start of this year. The increased production and lower natural gas prices allow natural gas to compete more with other fuels in uses such as electricity generation.

Volatility: Historical volatility reached its lowest point of the year in late July, settling at 26% on July 25. Implied volatility rose slightly since the beginning of July, increasing 1.3 percentage points to settle at 29% on August 7 (Figure 15). Relatively unchanged volatility during times of falling prices further suggests that an increase in production expectations is one of the drivers of declining natural gas prices, as increased supply would reduce the strain on inventories in the upcoming winter.

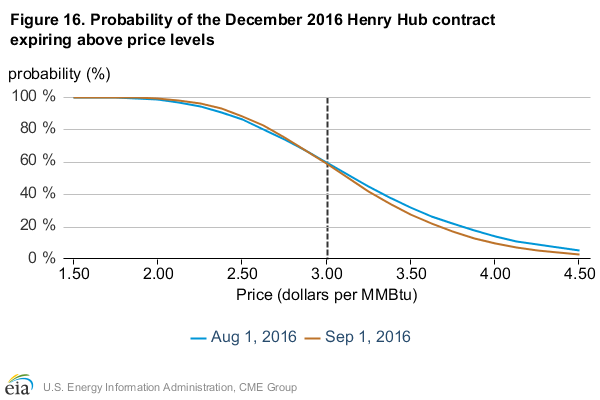

Market-Derived Probabilities: The November 2014 Henry Hub futures contract averaged $3.96/MMBtu for the five trading days ending August 7 and has a 16% probability of exceeding $4.50/MMBtu at expiration. The same contract for the five trading days ending July 1 had a 45% probability of exceeding $4.50/MMBtu (Figure 16).