The take-up of electric vehicles (EVs) may well be in a growth pattern which could rival that of the price of bitcoin, but is unlikely, like the latter to push sales into bubble territory. As range anxiety and long charging times recede into obscurity with the enormous developments in battery technology, the environmental, and ultimately the cost, benefits of electric drive for automobiles over internal combustion engine (ICE)-driven small vehicles is likely to become paramount.

The potential exponential growth pattern for EV sales will have likely an enormous impact on the sales volume, and price, of the metals utilized in EV production. These are notably lithium, cobalt, manganese, nickel, graphite, and some rare earths in battery manufacture, copper (an electric vehicle utilizes far more copper than a conventional ICE-driven vehicle) and perhaps aluminum to keep body panel weight down - and maybe as a substitute for copper in electrical wiring systems. Conversely, the longer term future for platinum group metals, predominantly utilized in ICE engine exhaust cleaning catalysts may well be bleak, and we see a serious downturn for these commencing in the next decade - and getting worse from there.

We thus see several major keys necessary to stimulate the more general take-up of EVs, rather than plug-in hybrids (PHEVs). The first, and most important, is ever-improving battery technology, perhaps coupled with the expansion of a nationwide fast charging network to handle distance driving demand. Range anxiety will be countered by battery life improvements, while an interim solution could be the inclusion in EVs of small range extending ICEs designed primarily to charge the batteries rather than for driving the vehicles.

Up until the current year, there were few EVs on the market capable of achieving a range of much more than 100 miles, but this is changing now quite rapidly, although the 300-400 miles of range between charges, which is probably necessary to achieve true sales lift-off, is mainly only available at the high end of the price range. But every time a new model is announced, range tends to be one of the aspects which is being expanded. We would anticipate 250-350 mile range to be the norm, rather than the exception, even in many low-end EVs by the end of the current decade.

So, if one looks at the extremely rapid pattern of technological battery improvement in computers and in mobile phones, there has to be the likelihood that battery technology research will continue to raise vehicle range between charges, and reduce costs as a combination of technological advance and scale of production leads to savings here. No doubt rapid charging technology will also develop alongside, as will the installation of more and more charging points across the nation - this being the other main bugbear, along with vehicle cost, affecting EV take-up. Ultimately, we suspect that far greater ranges may become the norm - maybe even 1,000 miles on a single charge before too long, certainly for high end vehicles.

This would likely be a nail in the coffin of the internal combustion engine (ICE) as would likely increasing legislation to ban ICE-driven vehicles from urban areas which we are already seeing in some major cities around the world as urban administrations in particular do battle with air pollution, to which gas and diesel driven vehicles are a major contributor. Indeed some nations are already looking to ban sales of ICE-driven vehicles. Norway, for example, is proposing to ban all fossil-fuelled cars from its roads. As the UK's Guardian newspaper reports, Norway already has the highest per capita number of all-electric [battery only] cars in the world: more than 100,000 in a country of 5.2 million people. In 2016, EVs constituted nearly 40% of the nation's newly registered passenger cars. And the Norwegian experiment shows every sign of accelerating. Earlier this year, Norway opened the world's largest fast-charging station, which can charge up to 28 vehicles in about half an hour. The country, joined by Europe's No. 2 in electromobility, the Netherlands, intends to phase out all fossil fuel-powered automobiles by 2025.

New types of battery technology may also be a factor here. At the moment most, if not all, EVs run on lithium-ion technology, but research is under way into so-called solid-state batteries which offer (in theory at least) lighter weights, longer ranges, shorter charging times, and lower costs than current standard lithium-ion batteries. But so far, the technology has not been able to be transferred from the laboratory to the kind of size necessary to drive a full-size EV efficiently. Even with lithium-ion technology, though, Elon Musk's Tesla (NASDAQ:TSLA) - perhaps the principal driver in the advance of EV design and implementation - is achieving a claimed 600 mile range between charges in some of its latest, currently available high-end vehicles - and is already on the way to achieving this on its 'affordable' Model 3 range.

Tesla has also announced an all-electric semi truck which appears expensive in relation to diesel driven trucks but claims a 2-year cost payback, given how much cheaper it is to run an all-electric vehicle than an ICE-powered one, and performance and range figures are impressive. Tesla also claims driver environment and substantial safety benefits for its semis. PepsiCo (NYSE:PEP) has already ordered 100 of these and expects to start taking delivery by 2019/20.

Other manufacturers are also planning to produce and sell all-electric trucks by the end of the current decade - Reuters reports that Navistar International Corp. (NYSE:NAV) and Volkswagen AG's (OTCPK:VLKAF) Truck and Bus are working together to launch an electric medium duty truck by late 2019, while rival Daimler AG (OTCPK:DDAIF) has delivered the first of a smaller range of electric trucks to customers in New York. These are designed for shorter ranges than the Tesla semi but will likely see expanded ranges as battery technology advances.

Re the solid state battery, in the UK, Sir James Dyson, of vacuum cleaner fame, is working to develop a Dyson EV by 2020 and is reportedly putting £2.5 billion towards its development. Dyson is also reportedly nailing his colors to the solid-state battery mast, although again whether a solid state battery sufficient to power an EV will be available in that timescale remains to be seen!

Japanese mainstream auto manufacturer Toyota (NYSE:TM) also reckons to be working on a solid-state battery-driven EV which it hopes to have on the market in the early 2020s. Undoubtedly, other mainstream manufacturers, virtually all of whom are working on EV design and production, will also be looking at the potential of solid state batteries because if they can be produced commercially will, eventually, offer the range, rapid charging and lower costs required to make EVs the norm rather than the exception.

With the kinds of technology growth patterns we have been seeing, we would anticipate total EV dominance of the automobile market far faster than recent projections might suggest - perhaps within 20 years. Already Volvo (OTCPK:VOLAF) has announced that every new car it launches from 2019 will have an electric motor (this will include hybrids so is not phasing out the ICE totally - yet - but is an indicator of the way the market is trending).

While battery technology/range is perhaps the most important factor for EV manufacture and sales going forward, cost is another hugely important factor. Despite the apparent drive-train simplicity of electric-powered vehicles, those on the market at the moment are much more costly than similar-sized conventional vehicles, and only attractive through the availability of government subsidies. Insurance costs are higher too.

But there are some other key advantages of electrically driven vehicles which will be major sales points assuming battery technology factors can be overcome - which they will be. Rapid torque availability - which means very fast acceleration - the far easier integration with new computer technology, potentially far lower running costs and the convenience of home charging, for those with that possibility, or with easy access to overnight charging points, rather than having to fill up at a gas station are all key points. But most of all the perceived environmental benefits of electric drive over ICE-driven vehicles are becoming paramount.

The capital and maintenance costs for EVs are likely to come down as take-up increases, but it may take time, and the continuation of subsidies until the market has truly taken off is probably key for any serious short-term growth momentum

Model Availability

Suffice it to say that the numbers of EVs available to the market will be increasing exponentially over the next few years with most mainstream manufacturers offering all-electric models already. However, one does have to credit Elon Musk's Tesla company with bringing EVs into mainstream thought with its spectacular high end Model S and Model X EVs, offering a degree of luxury and incredible performance only previously seen in high-end supercars. And now, Musk's company is in the throes of bringing his production vehicles into the 'affordable' category - if $35,000 plus is seen as 'affordable'. Pre-orders for the Tesla Model 3 are such that, provided it can meet its production targets, without going bust first, would make Tesla one of the world's largest automakers.

Musk is a visionary and is not stopping there and has just shown the all-electric-powered truck (mentioned above), and the 'Insane' Tesla Roadster capable of 0-60 mph in 1.9 seconds and with a claimed 620 mile range, but many think Musk's company is hugely overstretched and will crash and burn under its huge debt burden.

But it is probably Musk's amazing vision and drive which has stimulated the EV sector into action. Whether Tesla will survive, or will be overtaken by mostly mainstream auto manufacturers, who now have been dragged into the realization that EVs are almost certainly the future, remains to be seen. The mainstream manufacturers are battling to cut into Tesla's undoubted lead in the sector and are already coming out with possible Tesla killers - like the Chevy Bolt which offers similar pricing and performance to the Tesla Model 3 - but somehow lacks its kerb appeal.

Metals Demand

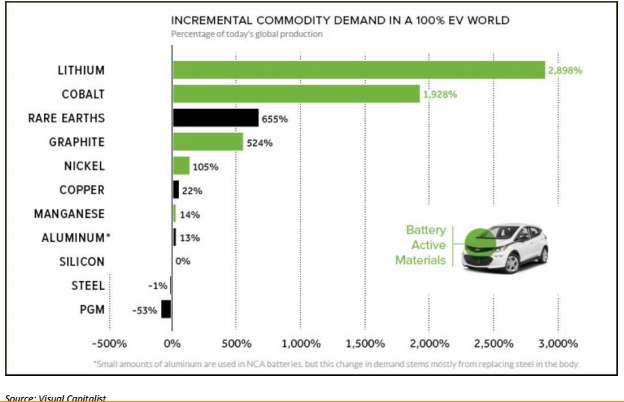

The global automobile market is enormous and a switch to EVs could have a huge impact. Below is a barchart from Visual Capitalist based on the change in metals demand with a 100% take-up of all-electric battery driven cars but only based on the battery technology used in the Chevy Bolt - GM's (NYSE:GM) direct competitor with the Tesla Model 3, which uses a different battery make-up - and would be very different still once solid state batteries have come into use. However, it is valuable in demonstrating some of the likely beneficiary metals in a switch to EVs.

image: https://static.seekingalpha.com/uploads/2017/12/14/16280222-15132618478684318.png

Naturally, lithium tops the bill, but here, there is plenty of future production coming on stream to meet demand so a lithium play may not be as beneficial as it would seem from the chart. It is perhaps some of the other metals where supply may not be able to keep up with demand and prices may rocket, but because these metals are often produced as byproducts, securing an investment that may take off accordingly may be more difficult to do.

Of the primary metals, the biggest beneficiaries could be copper, nickel, and aluminum - the former because the average EV uses around twice as much copper as existing ICE-driven vehicles, nickel, and aluminum are both used in some battery technologies in a big way, while the latter will almost certainly get increasing use in body panels to keep vehicle weights down. Of the byproduct metals cobalt has obviously the most potential as do the rare earths - specifically dysprosium which is utilized in some electric drive technologies.

London quoted Glencore [LSE: GLEN] is comfortably the world's biggest cobalt producer, but cobalt only represents a small part of the company's product mix, but nickel is important too. An ADR is available to U.S. Investors: Glencore ADR (OTCPK:GLNCY). Canada's Sherritt International [TSX: S] which will also benefit as a major nickel producer could be of interest and again is available on the OTC market in the U.S. - Sherritt International (OTCPK:SHERF). Another major cobalt miner with a U.S. ADR quote is Brazil's Vale (NYSE:VALE) but, like Glencore, is one of the world's largest diversified miners, and cobalt represents a fairly small part of its overall revenues - but Vale is also the world's second largest nickel producer after Russia's Norilsk (OTCPK:NILSY).

Dysprosium is the rare earths wild card, but there is little or no significant production outside China, although Australia's Northern Minerals [ASX: NTU] has brought is Browns Range mine into production and reckons to be the world's next significant dysprosium producer outside China. But its mining operation, high in heavy rare earths of which dysprosium is particularly significant, is only at pilot plant construction stage at the moment.

Graphite, which may be the other major beneficiary 'metal', is primarily produced in China, India, Brazil, Turkey, and North Korea. Graphite investment options in North America are largely restricted to the risky junior sector, and none are full board quoted. There have been articles on Seeking Alpha about these, but for the moment, this writer is steering clear. The junior sector seems just too speculative. Rather look to the major stocks which may benefit as the downsides are much more limited.

Of the major metals, copper appears to be the likely major beneficiary of significant growth in the EV sector, while maintaining significant demand in the ICE-driven vehicle sector. The world's biggest producer remains the Chilean state-owned Codelco, but the remaining big producers apart from the U.S. company, Freeport McMoran (NYSE:FCX) are mostly the big diversified miners. Glencore and Vale, both mentioned above as major nickel and cobalt miners, are among these as are BHP Billiton (BHP) and Rio Tinto (RIO), the world's two biggest diversified miners. Both these are headquartered elsewhere - BHP's joint HQ are in the UK and Australia, and Rio Tinto in the UK. Once again, because these are such big diversified mining companies, demand growth in a particular sector like copper may be less significant yet still give a useful boost to earnings.

The same applies to aluminum. Alcoa (NYSE:AA) is the biggest North American producer, but any impact due to growth in the automobile production sector won't have a particularly significant impact overall as it will only represent a tiny portion of overall demand.

While this article primarily looks at the likely growth potential for EVs and some of the likely long term beneficiaries (virtually, none of the anticipated gains in the major sector are likely to eventuate until the next decade), one should also take a look at the eventual losers. The most notable is the market for platinum, palladium, and rhodium, all of which have their primary usage in ICE exhaust emission control catalytic technology. Here again, the problems are likely to appear long term - not short term where global recovery may still lead to some good gains - particularly if precious metals' prices (driven by gold) rise. We would expect the platinum and palladium prices to rebalance in favor of platinum, given the change in the pricing differential is likely to result in a switch to platinum catalysts in at least a part of the gasoline ICE exhaust control market.

The current high palladium price of over $1,000 an ounce does not seem yet to have impacted stocks like Sibanye-Stillwater (SBGL). While the company is also expanding its platinum exposure through the just-announced purchase of Lonmin, it is not really being given the credit for its palladium exposure through Stillwater, and also in South Africa, where the majority of its production is based. Its holdings there are predominantly in mines producing primarily from the platinum richer Merensky reef, but it has the capability to add to its production on the UG2 reef which has a marginally higher palladium and rhodium content. But overall, both Stillwater and the South African producers are at best marginal operations at current pgm prices, although the higher palladium and rhodium prices may be slightly improving the economics.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Editor's Note: This article covers one or more stocks trading at less than $1 per share and/or with less than a $100 million market cap. Please be aware of the risks associated with these stocks.