Nevsun Resources (NSU) has released its Q2 financial results. However, much more interesting than the financial results was the related conference call and some hints regarding the future of the company. The most important information is that management still believes that Lundin Mining's (OTCPK:LUNMF) takeover offer of C$4.75 per share heavily undervalues Nevsun's assets. This claim is supported also by last week's transaction, when Newmont Mining (NEM) announced the acquisition of 50% of NovaGold's (NG) Galore Creek project.

There were 51.3 million lb zinc and 8.6 million lb copper produced at Nevsun's 60%-owned Eritrean Bisha mine in Q2 2018. That means zinc production was 28% lower and copper production 3% lower than in Q1. The production decline was caused by lower zinc feed grades (6.1% in Q2 vs. 7.1% in Q1) and a lower throughput rate. The throughput rate was negatively affected by maintenance activities and as a result, only 491,000 tonnes of ore were milled, which is almost 13% less than in Q1. However, the company expects that the ore grades will rebound in the second half of 2018. Therefore, it reiterated 2018 cost and production guidance. The Bisha mine should be able to produce 210-240 million lb zinc and 20-30 million lb copper, at a C1 cash cost on a by-product basis of $0.6-0.8/lb zinc.

What is positive is that zinc recoveries remained close to the 80% level and zinc concentrate grade remained unchanged at 47.8%, while copper recoveries improved to 69.4% and copper concentrate grade improved to 21.5%. As a result, Nevsun recorded revenues of $76.4 million, earnings from operations of $2.4 million and a net loss of $9.3 million. The company was debt-free and it held cash of $125.1 million as of the end of Q2.

However, as I mentioned above, the conference call was more interesting than the financial results. Nevsun still believes that Lundin's offer is not good enough. According to Peter Kukielski, Nevsun's CEO:

We were surprised by the value they have presented with their formal offer of CAD 4.75 in cash for all shares of Nevsun. This offer is lower than a proposed – proposal delivered to me and the Board of Directors on July 3, which indicated Lundin was prepared to offer $5 per share for the company in the combination of cash and Lundin shares with an established miner as a new partner for Bisha.

We engaged with the new partner, signing a confidentiality agreement and granted access to our data room, only to be surprised by Lundin’s sudden announcement on July 16 to launch a bid on their own.

Especially the second part of the statement is interesting. It seems like Lundin Mining found a potential acquirer more experienced (than Euro Sun Mining (OTCPK:CPNFF)) for the Eritrean assets. But just days after the new potential acquirer was granted access to the data, Lundin started the hostile takeover attempt. There are only two logical explanations:

- The potential acquirer didn't like the data it was provided and lost interest in Bisha. However, it is reasonable to expect that the data evaluation would take a little more time. Moreover, the potential acquirer would probably announce to Nevsun's management that it isn't interested anymore.

- Lundin Mining got scared by the developments at Nevsun and decided to act quickly in order to acquire Timok as quickly and as cheaply as possible.

I believe that the second explanation is more probable. Lundin knows that if Nevsun proves its ability to finance Timok Upper Zone without an excessive share dilution, it will be much harder to persuade Nevsun's shareholders to sell their shares cheaply. According to the conference call, it seems like there are several potential strategic investors in Nevsun willing to acquire less than 20% of the company. It means the potential share dilution would be only up to 20%, which definitely isn't a tragedy. According to Ryan McWilliam, Nevsun's CFO:

We received strong expressions of interest from strategic partners looking to invest in Nevsun this quarter.

Several of these potential strategic partners are now in the final stages of due diligence. Partner will provide both cash and potential complementary technical, marketing or off-tech capabilities that will further aid the development of Timok.

A 20% share dilution simply isn't scary enough to persuade Nevsun's investors that they won't be able to benefit from the Timok project. Moreover, a strong partner owning up to 20% of outstanding shares may mean a complication for Lundin's hostile takeover attempt. It is possible that Lundin was somehow informed that a strategic partner may show up soon which prompted Lundin to act quickly.

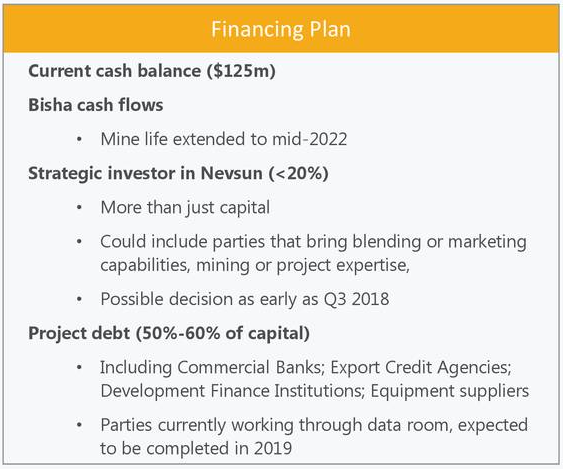

The financing plan presented by Nevsun seems reasonable (picture below). Nevsun wants to use its cash on hand ($125 million) and cash-flows generated by Bisha. Over the last three quarters, Nevsun recorded earnings from operations of $13.6 million on average. Conservatively assuming that this value will decline to $7 million per quarter on average over the next 18 quarters, Bisha should be able to generate $126 million by the end of 2022. A strategic investor should provide approximately $220 million (assuming it will acquire 20% of Nevsun at the current market price). About 50-60% of the Upper Zone initial CAPEX should be covered by some form of debt. According to the PFS, the initial CAPEX is estimated at $574 million and another $114 million should be spent before the construction decision is reached. It means that the debt financing should provide $290-350 million.

Source: Nevsun Resources

Source: Nevsun Resources

The above financing package should be able to secure $760-820 million. It should be more than enough to cover the combined pre-production and pre-construction CAPEX estimated at $688 million. Moreover, Nevsun is working on a study that evaluates the possibility to start with a 1.6 million tpa operation that would be expanded to 3.2 million tpa after the initial 2 years of production. This approach is believed to reduce the pre-construction CAPEX needs by approximately $100 million. The study should be completed this quarter.

The process of debt financing seems to be well underway as well. According to the CFO:

A traditional project finance facility is expected to fund 50% to 60% of the project’s capital. We continue discussions with commercial banks, export credit agencies and development banks, who have expressed the strong interest in participating in this facility. Several of these parties are now under confidentiality agreement, received management presentations and are reviewing a data room, which has been set up for potential lenders. We’re on track to deliver this facility in 2019.

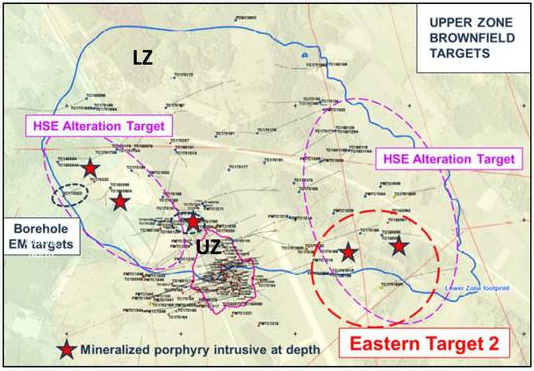

Moreover, there are other catalysts on the horizon. A 12,500 m drill campaign is underway. Its aim is to identify more Upper Zone-like deposits. A hot candidate has been identified only 500 meters to the east of the Upper Zone, in the Eastern Target 2 area (map below), where previous drilling intersected 2.93% copper and 2.54 g/t gold over 27 meters.

The great exploration potential is confirmed also by the historical experiences with copper-gold mineralization in the region. According to the CEO:

The great exploration potential is confirmed also by the historical experiences with copper-gold mineralization in the region. According to the CEO:

From a broader perspective, I should note that over its long history, 27 Upper Zone style deposits have been discovered and mined in Bor. And much of the land around the Bor complex has not yet been explored. In fact, Nevsun’s total land package in the Bor region provides us with significant Brownfield and Greenfield exploration opportunities and what is considered to be one of the most perspective camps in Europe, if not the entire world.

The initial results from the current drill campaign are expected this quarter.

For Nevsun's shareholders, Newmont's acquisition of 50% of the Galore Creek project from NovaGold could also be interesting. At current metals prices, the Galore Creek deposit contains measured, indicated and inferred resources of 17.78 billion lb of copper equivalent, including reserves of 9.72 billion lb of copper equivalent. The transaction values 1 lb of copper equivalent resources at $0.03 and 1 lb of copper equivalent reserves at $0.057. Using the same valuation on 16.366 billion lb of copper equivalent of the Lower Zone resources attributable to Nevsun, we can come to a value of $491 million. It is in line with my previous estimate that Nevsun should demand at least $500 million for its stake in Timok Lower Zone alone.

It is possible to argue that Galore Creek is a more advanced project and it contains higher categories of resources as well as reserves. It is true, on the other hand, that Galore Creek's PFS is 7 years old. Galore Creek won't reach production anytime soon, new economic studies need to be prepared first and the estimated CAPEX to build the mine is $5.16 billion. Moreover, as I stated in my article about this transaction, I believe that it was more favorable for the buyer than for the seller, i.e. NovaGold sold its stake in Galore Creek cheaply, as it wanted the cash to focus on its flagship Donlin project.

Conclusion

Nevsun's Q2 results were worse than the Q1 results, however, this development was expected given the negative zinc price development. For Nevsun's shareholders, the conference call was more interesting than the financial results themselves. The management has outlined the Timok Upper Zone financial package that envisages a share dilution of only up to 20%. The financing plan seems to be reasonable. According to management, several parties have serious interest in making the strategic investment in Nevsun's equities and several European banks are interested in providing the debt financing. A drilling campaign focused on discovering new Upper Zone-like deposits is underway with initial results expected this quarter. Also a study evaluating alternative Upper Zone development options with reduced pre-production CAPEX should be completed this quarter.

Given the positive developments, Lundin Mining decided to start a hostile takeover attempt in order to acquire Nevsun, and especially Timok, as soon and as cheaply as possible. However, the offered price of C$4.75 per share ($3.64) per share is too low. I believe that a serious offer should be closer to $2 billion ($6.5 per share). Recent developments appear to confirm this.