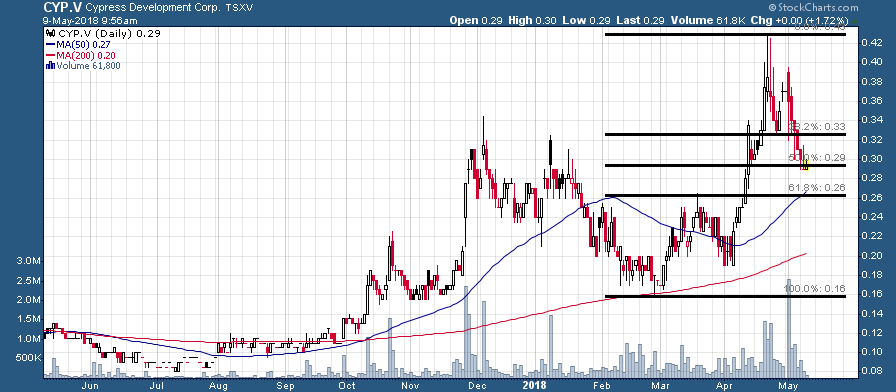

So under valued compared to bacanora At its recent share price of C$.30 Cypress has a C$17.5 million market cap – CYP’s current market cap is 1/10th of lithium development peer Bacanora Minerals (TSX-V:BCN), which has a C$187 million market cap. Bacanora’s clay-held lithium project is at the BFS stage (bankable feasibility study) and it is slightly larger than CYP’s project, however, the valuation gap is simply enormous. Cypress is in a superior location/jurisdiction (Nevada) compared to Bacanora’s project (Mexico) and CYP shareholders can look forward to CYP shares bridging the current valuation gap as the company advances towards the BFS stage over the next year (it’s quite possible that Cypress could be in the bankable feasibility stage by the 2nd half of 2019). Proving the value of the project’s mineralogy will be a huge step towards producing a positive PEA with compelling project economics. Buying near C$.30 (previous resistance and 50% retracement of February-April rally) following the “selling on the news” after the resource estimate announcement might be an attractive entry point as Cypress embarks upon what could be the most critical year and a half in the company’s history:

CYP.V (1 Year)