Why am I now looking at a penny stock?

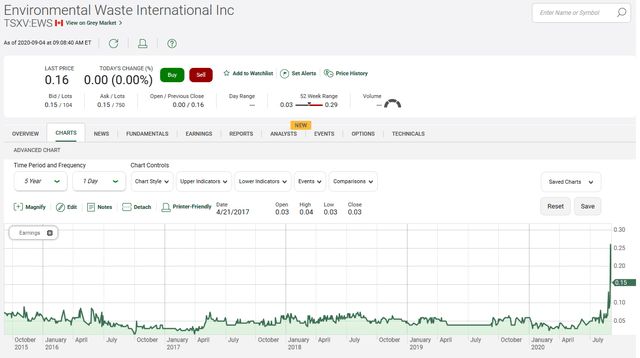

After I sold my previous company, SyncBASE/OPTRACK about five years ago, I was released from the restriction of trading shares of my public clients. Environmental Waste International Inc. (TSXV: EWS) (OTC:YEWTF) was one of those companies. The price of the stock was less than CAD 10 cents a share at that time, and I invested a good chunk of money in it.

One of the reasons for my investment was my relationship with EWI's CEO, Bob MacBean: Bob was the first client of OPTRACK when he was CFO of another public company. Bob also sat on the Board of my company. When he took the position as CEO of EWI, he began using my product, OPTRACK, again for EWI.

Last month, EWI had a breakthrough through a deal with a Danish company called WindSpace to develop waste tire recycling plants across Europe. That announcement, combined with the receipt of the Environmental Compliance Approvals (a few days later) to operate its tire recycling plant in Sault Ste. Marie, Ontario as a commercial facility, resulted in a significant jump in the stock price.

Source: TD Waterhouse Charts

Holding a significant number of shares of EWI, I performed some basic financial projections on the company which indicated to me that it is grossly undervalued. I decided to do a more thorough analysis, and to share my findings by publishing this article. I hold less than half a dozen penny stocks; most of my investments are in large caps. Historically, I have done terribly bad with penny stocks and did remarkably well with large cap stocks. Having said that, EWI is a penny stock that I am fairly comfortable with; I will explain the reasons for my comfort level below.

The article starts by explaining the different alternatives for recycling tires, and how I believe that EWI's Reverse Polymerization is superior to other technologies. EWI's patents, the overall tire recycling business, and competitors to EWI are also discussed. The article concludes with the discounted cash flow valuation and the risks of investing in EWI.

How do we normally recycle tires?

There are many technologies for recycling tires:

Tire-derived Products:

The most economical recycling of tires is reusing them without processing for other purposes. For centuries, we have all seen tire swings and marina bumpers. There are many other creative uses of tires as shown in the following collection of pictures, but the markets are quite small.

Source: Compiled by author from various sources through Google Images

There are many uses of tires as construction material (source, Wikipedia). Entire homes can be built with whole tires. Tires are used in civil engineering applications such as sub-grade fill and embankments, back-fill for walls and bridge abutments, sub-grade insulation for roads, and septic system drain fields. Tires are also bound together and used as different types of barriers such as: collision reduction, erosion control, rainwater runoff, blasting mats, wave action that protects piers and marshes, and sound barriers between roadways and residences. While controversial because of environmental issues, tires are also used in building artificial reefs. Some companies use tires in constructing the grounds for gyms, basketball and tennis courts, although there are also health concerns with these uses.

Stockpiling, Legal Dumping and Landfill Disposal

Tires need to be shredded to be used in landfills, which is an expensive process; if tires are placed as is, they would have about 75% void space, which would trap methane gas causing them to become buoyant, or bubble to the surface, effectively destroying the landfill.

Source: Charismatic Planet, World's Biggest Tyre Graveyard

Stockpiles and legal dumping of tires create very serious health and safety risks. These stockpiles turn to a breeding ground for vermin and insects, especially mosquitoes. In addition, tire fires can occur easily and can burn for months.

Simply said, stockpiling, legal dumping and landfill disposal of end-of-life tires have very serious environmental, health and safety issues.

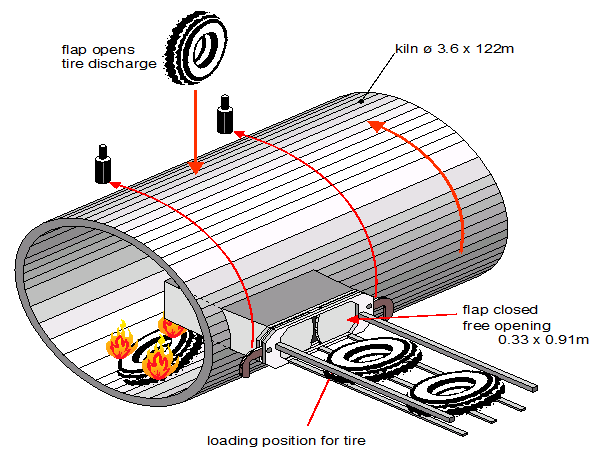

Cement Manufacturing

Burning tires as an alternative fuel is the largest use of waste tires. Manufacturers of Portland cement are large users of tires as fuel. As tires are dropping in the cement kilns (mostly the rotary ones, as shown in the next diagram), the high temperature (usually over 1,000 °C) causes almost immediate decomposition of the tire into its individual components (carbon black, oil and steel), which are all ingredients of Portland cement. Some plants feed shredded tires into the kilns instead of dropping whole tires. The gas emissions associated with alternative fuel (like tires) for Portland Cement production is one of the biggest environmental concerns that are yet to be addressed.

Source: Infinity for Cement Equipment, Use of Alternative Fuels

Steel Mills

Scrap iron and Carbon are two main ingredients in steel manufacturing. Given that tires contain both steel and Carbon, they can be used as scrap iron and a carbon source in steel mills, replacing coal or coke. The oil and gases produced by introducing tires into the mix for steel mills result in environmental issues that are yet to be resolved.

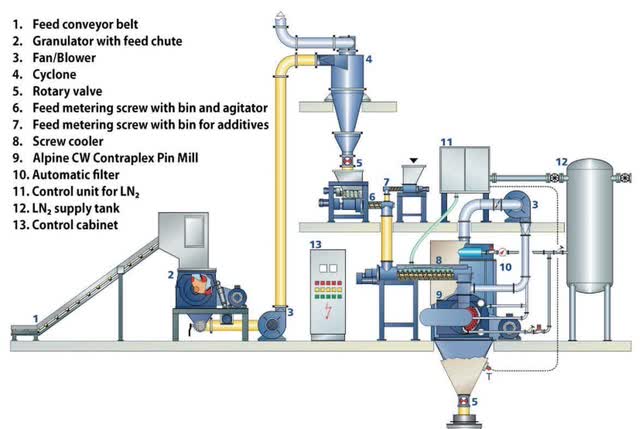

Cryogenic Recycling

Tires can be frozen using cryogens, or super-cold fluids like liquid Nitrogen. This would break the tires down and render them into a material called "crumb". This material can then be used in asphalt roadbeds, agricultural hoses, truck bed liners and various other uses. In other words, this method can be construed as a "chemical grinding" of tires but it is a rather expensive technology.

Source: Hosokawa Polymer Systems, Cryogenic Grinding of Rubber

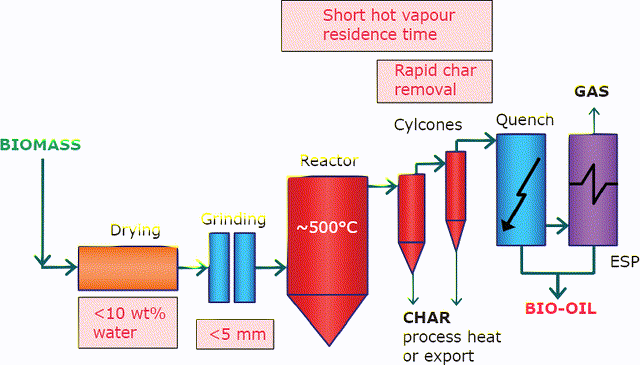

Pyrolysis

Pyrolysis heats whole or shredded tires (mostly shredded) in an oxygen-depleted environment at about 700 to 900 °C while agitating them to ensure even heating. Polymers are then used to soften the rubber and the smaller molecules eventually vaporize. These vapors are then normally burned to produce the self-sustaining reaction. The operation is conducted in a pressurized system, which is expensive and creates serious safety issues.

When performed properly, the tire pyrolysis process is a clean operation and produces little emissions or waste; however, there are concerns about air pollution due to incomplete combustion as is the case with tire fires, which has been well documented.

Source: Johnson Matthey Technology Review, Challenges and Opportunities in Fast Pyrolysis of Biomass: Part I

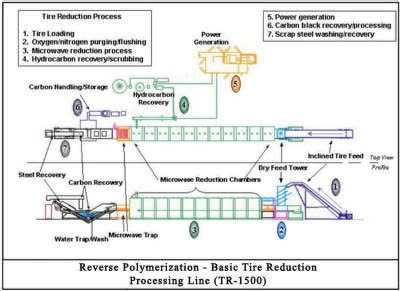

Reverse Polymerization

While fundamentally different, this process is similar to Pyrolysis. It is the patented process developed by EWI for the controlled breakdown of organic waste. EWI published a video that shows how Reverse Polymerization works.

Source: Environmental Waste International

In very simple terms, microwave technology is used to heat the tires in an oxygen-depleted environment and reduce the tires to their basic components of steel, oil, carbon black and hydrocarbon gases.

The hydrocarbon gases are used to pre-heat the tires before the microwave processing and to supplement the heating requirements; this reduces the environmental impact of the tire processing while reducing the external energy (electricity) requirements; this technology is called Hybrid Reverse Polymerization.

As a summary, here is the process for Reverse Polymerization:

- Scrap tires or tire shred is fed into the system, where the air is removed and replaced with nitrogen and preheated.

- The tires then pass through a series of shutters before entering the microwave reduction chambers.

- As the tires move through the tunnel of microwave reduction chambers. The microwave field causes reverse polymerization to occur. The tires break down.

- Gases produced by this process are drawn off, collected, and passed through a condenser to form the hydrocarbon oil.

- Remaining gaseous hydrocarbons continue to a scrubber, where sulphur is removed. The gas and oil can then be used either to (a) generate electricity for the RP process, or (b) be sold as feedstock in other industrial processes.

- Carbon and steel remain on the feed belt and exit the microwave reduction tunnel. The materials are separated, the carbon and steel are collected and sent to storage containers for sale.

Source: EWI Website

How is Hybrid Reverse Polymerization superior to Pyrolysis?

The following summarizes the differences between Pyrolysis and Hybrid Reverse Polymerization (EWI's technology). Reviewing this comparison demonstrates the superior technology developed by EWI and why it is bound to take over the tire recycling industry.

- Superior Processing Method: Pyrolysis processes are typically batch, under pressure and require agitation to produce an even heating. EWI is a continuous feed system, operating at slightly positive pressure with no agitation. These differences give EWI an advantage creating a superior oil (less carbon in the oil), greater recovery of carbon, increased safety and a more efficient overall process. This allows EWI to produce a quality carbon with less than 0.1% PAH.

- Lower Operating Temperature: Pyrolysis systems require an overall operating temperature between 700o-900oC. EWI's system operates at temperatures below 550oC. Pyrolysis systems require the increased temperatures to ensure even heating throughout the tire material, whereas EWI's use of microwave energy allows for even heating at lower overall temperature. The higher temperature creates scorching in the carbon and more light hydrocarbons. Lower temperatures produce a higher quality carbon and more oil in addition to lower energy consumption.

- Pollution: Due to the operating parameters of a pyrolysis system there is more air pollution created. To achieve the higher temperatures pyrolysis systems can introduce air to the process, the increased oxygen content creates unwanted oxygenated hydrocarbons in the vapor stream, while the increased temperatures create more light hydrocarbons.

- Process Control: There is very little control on a pyrolysis system, whereas an EWI system has complete control with the addition of microwave energy. This causes some safety concerns that do not exist with reverse polymerization. For example, stopping the operation in an EWI plant is almost immediate compared with stopping the operation of a pyrolysis plant.

How is EWI protecting its technology?

EWI is active in patenting its unique technology. The company has patents or patents pending in Brazil, Canada, China, India, Japan, the European Union (including the UK) and the US. These patents do not only apply to tires, but can also apply to any other material that requires controlled reduction via microwave technology (like organic waste processing, for example).

EWI also has an interesting patent for treatment and sterilization of medical waste using Reverse Polymerization.

Upon reviewing these patents, I came to the conclusion that EWI's potential is just starting with the tires, and that its technology has a plethora of other applications; this may be the topic of another article.

Who are EWI's competitors?

EWI's main competitors are operating in the traditional pyrolysis systems. Following are the main companies that may be considered competition for EWI (in alphabetical order):

- Beston (Henan) Machinery Co., China

- Careddi Technology Co., China

- Enrestec Inc., Taiwan

- Granunband Macon, US

- Henan Barui Environmental Protection Equipment CO., China

- Henan Doing Mechanical Equipment Co., China

- Henan Rotecho Industrial Co., China

- Hoi hing loong sdn bhd, Malaysia

- Huayin Renewable Energy Equipment Co., China

- Klean Industries, Canada

- Linyi Meicheng Machinery and Equipment Co., China:

- MoreGreen Environmental Protection Equipment Co., China

- Pyrocrat Systems LLP, India

- Pyrolyx, Germany/US

- Scandinavian Enviro Systems, Sweden:

- Unka Engineering, Turkey

- Xinxiang Huayin Renewable Energy Equipment Co., China

This list is by no means exhaustive; there are other companies that produce pyrolysis systems. In addition, there are other competitors that recycle tires using other technologies without breaking them down into their key components (e.g. cryogenic tire shredding). Upon reviewing these companies briefly, I was able to confirm that none of them is using or contemplating using the EWI patented microwave technology in their tire recycling process.

The Tire Recycling Business

The tire recycling business is a huge business. Used tires are a huge disposal problem throughout the world with 1.5 billion of them coming on the market annually or about 4.1 million a day. In most parts of the world end-of-life tires are used:

- As tire derived fuel for cement kilns, paper plants, steel mills and power plants, which is very bad for the environment because of the gases produced.

- Sent to waste disposal sites which is a poor long-term solution as spontaneous fires break out or they become a breeding ground for disease carrying rodents and insects, or

- Turned into shred or crumb rubber, producing a material that can then be reused to create various products; this just delays the problem and does not solve it.

Source: Chaleur Regional Service Commission

To calculate the overall cost of tire recycling, we can check the "eco fees" paid for every newly purchased tire. In Ontario, this fee is CDN$4.25 (approximately US$3.25). With 1.5 billion tires annually, we are talking about a Total Addressable Market of US$4.9 billion. This is almost the same as the current total addressable market for e-commerce software, with its high flying stocks like BigCommerce (BIGC) and Shopify (SHOP).

With the growth of electric vehicles, which increases tire wear compared to conventional vehicles, the tire recycling business is expected to grow at an accelerated rate.

Because of its unique superior proprietary technology, EWI is poised to play a major role in this industry. The current capitalization of EWI is less than $50 million. Since it has the most superior technology in the market associated with the tire recycling industry, $50M can be construed as a very low capitalization for such a growth company.

Valuation and Price Target

EWI does not provide guidance on projections as a matter of corporate policy and this valuation was strictly done by the author without feedback from EWI.

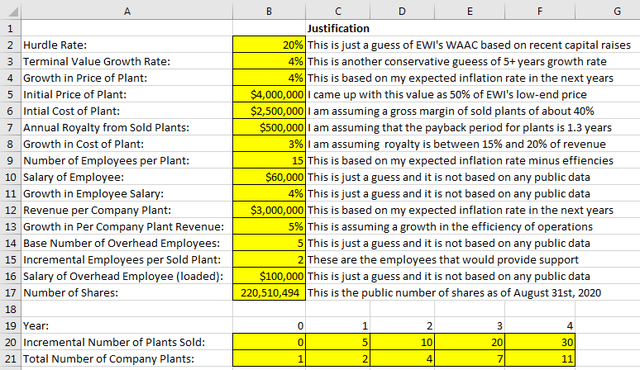

To come up with a price target and a valuation, I developed a discounted cash flow model. The challenge with this model is determining the parameters associated with it, including the number of plants that are expected to be sold, the number of plants that EWI will be operating, the price it will be charging per plant and the cost of developing each plant. Such information is not readily available for the public, and I proceeded with coming up with my best guess for them.

According to EWI's website, the price of a plant ranges between $8 million and $20 million depending on the capacity of the plant.

According to the press release associated with the expansion in Europe with WindSpace, the next five years will bring in $100M in revenue. Because EWI did not disclose the number of plants that would constitute $100M, we can come to the conclusion that it is significantly lower than the low-end $8M published on the website. Based on some educated guesses I came up with assumptions for the number of plants (sold and operated), and how much a plant would cost to build.

I created a spreadsheet that contains the assumptions and the discounted cash flow. It can be downloaded and the reader can vary the parameters and the model to derive a new price target. The following chart shows the valuation model assumptions, which I believe are relatively conservative.

Source: Assumptions and analysis developed by Author

The result of my analysis indicates that the company should have a capitalization of $333 million compared to its existing $32 million as of September 9th, indicating that the EWS stock is a potential 10 bagger and would render a stock price of $1.51 compared to the existing $0.15.

What are the risks of investing in EWI?

There is no investment without risk, and there is no solid analysis that does not take the negative risks into consideration. The risks of investment in EWS include:

Discovery/Invention of new technologies that are superior to Reverse Polymerization: We don't know what new technologies may come up for processing end-of-life tires; if a new technology, superior to Reverse Polymerization comes up, it would put a serious dent in EWI's prospects.

Poor execution from EWI's management resulting from fast expansion: Many companies fail because of their success leading to fast growth and because they would not manage the growth properly. I am personally confident in the management team capabilities, and while the risk exists, I would not consider it high.

Introduction of new environmental concerns: Reusing the tires without processing them is certainly the most environmentally friendly method of tire recycling. There is a remote possibility that tire processing would be banned because of environmental concerns. This would be a disaster for EWI. I don't expect this to happen during my lifetime, and that it is more of a black-swan event.

Failure to acquire the cash needed for expansion: For EWI to expand its existing plants, it needs to raise about $5 million of capital. EWI never had a problem in raising capital in the past, and I expect them to have no problem in raising capital this time, especially with the new August announcements.

Discovery of new types of tires that do not require recycling: We don't know what new technologies will be developed. For example, there is a possibility of having new sources of energy that would allow cars hover over the street instead of rolling the tires, which would increase the life of tires by orders of magnitude. This would also be a black swan event.

Creation of competing patents in other parts of the world that are not covered by existing EWI patents: I would consider this as one of the biggest risks for EWI. However, this risk can be easily mitigated by EWI expanding its patent reach to patent its technology in all countries where it has not yet been patented.

Conclusion

Environmental Waste International Inc. is a company on the verge of becoming a major global player in the $4.9 billion tire recycling industry. EWI's technology is superior to anything else in the market from both the productivity and environmental perspectives.

If my predictions are correct, the stock price of EWI would increase a minimum of 10-fold within a very short period of time. The assumptions presented in the analysis are relatively conservative, and the price target is based on a conservative fundamental discounted cash flow model.

Final word of caution: While I am confident about my analysis and have put my money where my mouth is, EWI is still a penny stock, and as such, the investment risk is very high. Investors need to be extra cautious and conduct their own analysis to come up with their own conclusion; that can be done via downloading the analysis spreadsheet and adjusting the model and the parameters.

If you liked this article, you might want to follow me from the top of the page so that you can get an e-mail notification of the articles that I write.

Disclosure: I am/we are long YEWTF. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: The technology presented here has been reviewed by EWI management. The financials presented here are strictly my own and EWI does not comment on financial projections.