A Closer Look at Kirkland Lake Gold's Insane Valuation

(This article was first released to subscribers on March 3, 2021.)

Kirkland Lake Gold (KL) shares have fallen so low that its valuation is now approaching absurd levels. The purpose of this article is to make the argument that Kirkland Lake Gold's stock is very undervalued, and may not have much room to drop further. At the time of writing, its shares trade at US$33.

Kirkland Lake Gold's valuation is one of the most compelling in the gold mining sector, and I believe investors might be wise here to dollar-cost averaging positions, while also setting dividends to be re-invested in the stock.

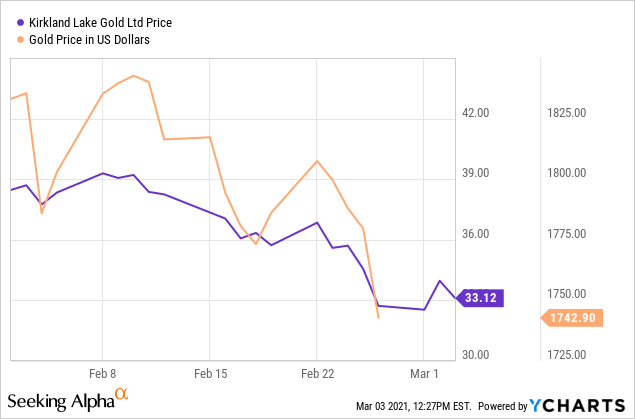

KL Stock Price Underperforming Gold

There is a growing gap between its stock price and gold prices (see above chart), but this week the gap seems to be reversing.

The stock is trading at $33.00 here with gold at $1,720/oz, as of writing on March 3. The last time its stock traded at $33 per share, it was April 2020 and the price of gold was $100 lower at $1,600/oz..

When gold had a hard sell-off in March of 2020, it dipped below $1,500/oz., and at that point in time, Kirkland Lake's stock price actually fell under $20 for a brief moment in time, creating one of the best buying opportunities in years.

If gold were to fall below $1,500/oz. again - which is possible, but seems very unlikely at this point in time - then shares could plunge even lower, if history is any indication.

However, the underperformance against gold has started to reverse a bit. In the past 5 days, the price of gold and KL shares are about the same - gold has fallen from $1,800 to $1,720 while KL shares fell from $38 to $33. KL is outperforming gold this week.

Data by YCharts

This might be a sign that we're nearing a bottom in mining stocks, as gold miners like Kirkland Lake Gold typically lead the metal higher on rallies.

Free Cash Flow Forecasts at $1,500/oz.. Gold

Kirkland Lake Gold is a profitable gold miner at nearly any gold price - the company would make money with gold at $1,100 (not much, but enough to make money and run its business). There is virtually no risk of bankruptcy as it has $850 million in cash and no debt.

*For the full-year 2020, it produced 1.369 million ounces of gold at an average all-in sustaining cost [AISC] of just $800/oz.. This cost metric includes everything it costs to produce an ounce of gold (All-In Sustaining Costs = Cash costs (including by-product credits), sustaining capital, exploration expenses, and G&A expenses.

*For 2021, the miner has forecasted 1.3 - 1.4 million ounces of gold at similar AISC - $900/oz. for the first half of the year, falling to $700/oz. for H2 2021.

If gold fell to $1,500/oz., and stayed there for several years (which, again, is a very unlikely scenario), the miner is estimated to produce upwards of $3.2+ billion in free cash flow (from 2021 - 24).

Free cash flow is the ultimate measure of profitability; it is defined at the cash a company generates after accounting for cash spent on growth (Ex: equipment, capex, mine expansion, etc.) It represents the money left over after all capital expenditures are paid, and the money free to pay dividends, buy back shares, or purchase new assets.

(Gold mining free cash flow forecasts. Credit: BMO Capital Markets.)

(Gold mining free cash flow forecasts. Credit: BMO Capital Markets.)

What's also pretty amazing to consider is the fact that Kirkland Lake Gold's enterprise value is now $8 billion after you subtract $850 million in net cash from its market cap. Assuming the forecasts above hold true, it would earn 40% of its enterprise value in free cash flow from 2021-24 using a super-bearish $1,500/oz. gold price.

Should gold average $1,850/oz. for the next 4 years, its free cash flow forecast comes in higher at $5.66 billion, which equals 70% of its current enterprise value.

Financially strong, low valuation

Kirkland Lake Gold ended 2020 in the best financial shape of its existence. The miner's cash balance totaled $847.6 million to end the year, a 20% increase from last year despite massive spending on share buybacks, dividends and capex.

The company used $732.4 million to repurchase 18.925 million shares through its normal course issuer bid. It also spent $115.9 million for dividend payments, and $98.6 million to repay Detour Gold's outstanding debt (the company has zero debt).

The stock now yields 2.30% based on an annual payout of $.75. Analysts have estimated earnings per share of $3.73 for 2021, which results in a payout ratio of 20%, indicating it has much more room to raise the dividend further.

Shares have a forward P/E ratio of 8.76X, and an EV/EBITDA of 5.19X, among the lowest multiples it has traded at in years.

Opportunity to purchase gold miners at a discount

It's arguably a great time to be a buyer of a gold mine. With $847 million in cash, no debt and access to at least $1 billion in available credit facilities, I think this is an opportune time for the company to consider making another acquisition or two, which would increase its gold reserves, production profile and cash flow.

Its $3.7 billion purchase of Detour Gold came in Nov. 2019, when gold traded at $1,450/oz., and it has been an incredible acquisition for the company.

Kirkland Lake Gold certainly doesn't need to make that big of a splash this time around and I think there are plenty of gold mines, and gold development projects in the U.S., Canada and Australia worth pursuing for less than $1-2 billion.

Expect a weaker Q1, but a much stronger finish to 2021

Kirkland Lake Gold's earnings will be strongest in the second half of the year and its first quarter will likely be the worst in terms of production and cash costs.

It'll produce upwards of 650,000 oz. Au in H1 2021, rising to 750,000 oz. Au in H2 2021. AISC per ounce sold are expected to average over $900 in the first six months of the year, and be highest in Q1 2020, improving to approximately $700 during H2 2021.

Any further weakness in its stock price should be bought in my opinion. I know it's hard to buy a stock that seems to keep falling, and it may seem like the stock has been falling for years by now! But the fundamentals for KL are very, very strong. At some point in time the stock is going to turn a corner, with the stock holding impressive upside potential.