Photo by coldsnowstorm/E+ via Getty Images

Photo by coldsnowstorm/E+ via Getty Images Investment Thesis

In August 2020 when I last posted a note on Liminal Biosciences (LMNL), the company's shares were riding high on the promise of its convalescent plasma collection program, following the FDA's decision to hand an Emergency Use Authorisation ("EUA") to the use of convalescent plasma from patients recovered from COVID-19 to treat hospitalized patients with the virus.

Liminal's shares - which had been trading at ~$8.5, spiked to $23 on the news, as the company, through its subsidiary Prometic Plasma Resources joined the Plasma Alliance, collecting convalescent plasma via its FDA and Health Canada approved collection centre in Manitoba, Canada, and a second center, in Amherst New York, which received full FDA approval in January this year.

As we now know, however, the thesis that convalescent plasma - theoretically teeming with neutralizing antibodies against COVID-19 - could be administered to hospitalized patients to aid recovery has now been widely discredited, with studies showing that the technique had no effect in 28-day mortality rates.

By the end of 2020, Liminal shares had sunk to a price of $4.2, and in late January Liminal announced that it would look at strategic alternatives for its plasma collection business - i.e. a sale, to try to reduce its net losses - which had been $143m, $158m and $92.7 in 2018, 2019, and 2020 respectively.

As part of its convalescent plasma business, Liminal is still developing Ryplazim - a purified glu-plasminogen derived from human plasma that can be used as a plasminogen replacement therapy, to treat patients with congenital plasminogen deficiency ("C-PLGD").

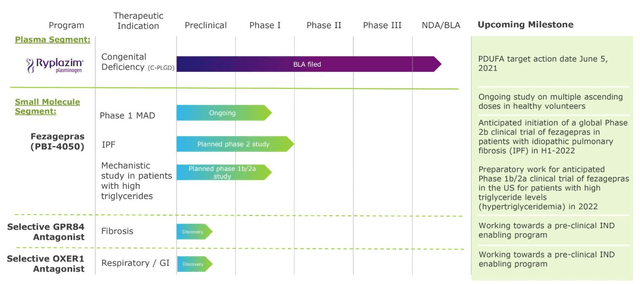

Liminal completed a Phase 2/3 trial of Ryplazim in 2018, which achieved the targeted increase from baseline in patients individual trough plasminogen activity levels through 12 weeks of therapy, and complete healing of their measurable lesions within 48 weeks of initiating therapy. After resubmitting its Biologics License Application ("BLA") to the FDA in September, Ryplazim now has a PDUFA date - when the FDA will rule on whether to approve the drug - on June 5 this year.

A few days ago, Liminal announced that it had agreed a deal with Italy-based plasma specialist Kedrion for the sale of its two plasma collection centers in a deal worth $17m upon completion, with Kedrion retaining an option to acquire the rest of the plasma business - i.e. Ryplazim and Liminal subsidiaries Prometic Biotherapeutics and Prometic Bioproduction - for an additional $5m, by June 15. Liminal, however, would retain a 70% claim on the net proceeds from an FDA Pediatric Rare Disease Priority Review Voucher, which would be issued if Ryplazim is approved, and could be worth ~$100m if sold.

As such, Liminal will shortly exit the plasma business altogether, and the company's focus is now solely on developing its pipeline of small molecule assets, which includes Fezagepras ("Feza") - an anti-inflammatory and anti-fibrotic therapy designed to modulate the activity of receptors including GPR40 and PPAR alpha, amongst others.

Feza is currently progressing through a Phase 1 dose escalation trial in the United Kingdom, with a global Phase 2 expected to initiate in H122, subject to results from the Phase 1 study, and a Phase 1b/2a in patients with high triglyceride levels in the US, also in 2022. Feza has been granted an Orphan Drug Designation by the FDA, and the European Medicines Agency ("EMA") for treatment of both Idiopathic Pulmonary Fibrosis ("IPF"), and Alstrm syndrome.

Finally, Liminal has a preclinical GPR84 antagonist drug candidate, and selective OXER1 antagonist candidate, for which the company hopes to submit Investigational New Drug Application ("IND") enabling programs pending the outcome of successful studies.

To summarize the investment thesis for Liminal then, this is a company that's undergoing a second major transformation in the past two years. Formerly known as Prometic Life Sciences, the biotech changed its name and sold off its bio-separation business in 2019, issuing billions of new shares to stave off bankruptcy, before completing a 1000-1 stock split, reducing its share count back down to 23.13m.

Now that the convalescent business is being sold for a fraction of the price that Liminal may have hoped for, and another new management team overhauled and replaced, and with losses of $20.4m in Q121 announced this week, and a cash position of just $17.9m, the outlook for Liminal as an investment opportunity does not look promising.

Hope now rests entirely on the promise of the company's small molecule pipeline - which is early stage but targets areas of high unmet need in fibrosis and possibly diabetes - whilst a $70m windfall through the Priority Review Voucher sale - should Ryplazim be approved - would help to ease the company's financial concerns.

With a current market cap of just $99m, risk-on investors may feel that the stock price could rise on positive Phase 1 Feza data or Ryplazim approval, but against that, the failure of one or both of these potential price catalysts would be very damaging for Liminal and may even spell the end of the company.

As such, I would take a neutral stance on Liminal at this time. My optimism around the COVID opportunity and blood plasma business in my last note was misplaced, and although the upcoming data and voucher sale catalysts could provide some short-term share price accretion, even if Feza was to return compelling data from its dose escalation study, Liminal would still be years away from a pivotal trial initiation, short of cash, and having exhausted the appetite of investors for further fundraising.

Nevertheless, in the rest of this article, I will discuss recent changes at the company, the Feza opportunity, and the likelihood of a Ryplazim approval.

Liminal - Company Overview

As discussed in detail in my last note, Liminal is headquartered in Quebec, Canada, with offices in Cambridge, United Kingdom, and Rockville, Maryland.

The Canadian investment firm Thomvest Asset Management holds a majority and controlling 71.6% stake in the company via its Structured Alpha investment fund after helping Liminal complete a debt restructuring in 2019.

As a result, Stefan Clulow, then MD of Thomvest, became chair of Liminal's Board of Directors, while Dr. Benny Soffer - an executive at Consonance Capital - another investment firm which helped Liminal complete a $75m fundraising at the same time as the restructuring - designated Liminal's board observer.

Both appear to have now left the company, with two new board members - Alek Krstajic, a communication entrepreneur - and Eugene Siklos - President of ThomVest Asset Management - appointed in September last year.

Kenneth Galbraith - a biotech and finance veteran who became Liminal's CEO in April 2019 - also announced his resignation in November last year, citing personal reasons, with Liminal's Chief Operating Officer of its Small Molecule Therapeutics division Bruce Pritchard - an accountant by trade, who has been with Liminal since 2008, taking his place.

Alongside Pritchard, Patrick Sartore - formerly COO of the plasma therapeutics business - is now Liminal's President, and Murielle Lortie - who has been with the company since 2018 - has been appointed Chief Financial Officer.

With management having limited drug-development experience, the responsibility for development of Feza apparently rests with Dr. Jeffrey Smith, the company's Strategic Medical Advisor - a former founder of Alder Biopharmaceuticals Inc (NASDAQ:ALDR) who worked on an anti-CGRP antibody for migraine treatment and anti -IL-6 antibody for rheumatoid arthritis - and Dr Gary Bridger - a Board member and former Executive Vice President of Research and Development at Xenon Pharmaceuticals Inc (NASDAQ:XENE), who also co-founded AnorMED - sold to Genzyme in a $580m deal in 2006.

Recent Progress

I have covered Liminal's recent progress in my intro, with management confirming most of the detail in its Q121 earnings presentation released this week.

Liminal Biosciences - pipeline status as of Q121. Source: Q121 earnings presentation.

As discussed, the Ryplazim PDUFA date of June 5 is the most important date on the company's calendar, with the possibility of a lucrative Priority Review Voucher in play, potentially worth ~$70m to the company - money that may be critical to the survival of the business.

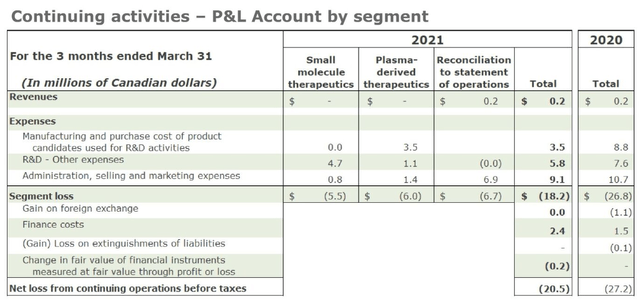

In Q121, total net loss was $20.5m, with the plasma business accounting for ~$6m of that figure, and contributing a meager $200k of revenue via sales of convalescent plasma. Going forward then, Liminal will at least reduce its cash burn to more manageable levels.

Liminal P&L accounts as at Q121. Source: Q121 earnings presentation.

Liminal has indicated that it's likely to attempt to raise funds via the capital markets, creating further dilution for investors, although it will operate a scaled-down operation with a narrow small molecule focus for the foreseeable future.

The Fezagepras Opportunity and Early Pipeline

According to estimates, the Idiopathic Pulmonary Fibrosis Market could be worth as much as $8.8bn by 2027, Around 100k people in the US suffer from the disease, with 30-40k new cases diagnosed each year.

Current treatments for the disease include Corticosteroids and Proton Pump Inhibitors, while two drugs - Boehringer Ingelheim's Ofev and Roche's (OTCQX:RHHBY) Esbriet - which made respective sales of $1.1bn and $2.5bn have been approved to treat the disease. There's currently no cure for IPF.

Sales of Esbriet and Ofev appear to be substantially below the forecast market size for IPF, so theoretically Liminal could have a valuable asset on its hands with Feza. There's also some encouragement in the fact that in 2019, Roche paid $390m upfront and committed to milestone payments of up to $1bn to acquire the private biotech Promedior, in order to acquire its early stage IPF drug PRM-151.

There's no question that Liminal would be desperate to find a development partner for Feza, but aside from an exploratory Phase 2 trial of Feza as a monotherapy conducted in 2017 in 41 patients, which showed the drug to be well-tolerated at an 800mg dose, there's very little data available to tempt potential collaborators.

A second Phase 2 trial in patients with Alstrm syndrome - a rare fibrosis disease involving the heart, liver, and kidney was abandoned in May 2020 due to COVID restraints.

Liminal management states in its Q121 10Q submission:

We have observed that Fezagepras regulated fibrotic and inflammatory markers in rodent and normal human fibroblasts, idiopathic pulmonary fibrosis patient fibroblasts, human epithelial cells and in rodent macrophages.

Based on my layman's knowledge of fibrosis treatment, the targeting of PPAR-alpha and GPR40 - involved in the regulation of fatty acids and insulin - is a well-established route to fibrosis treatment and even diabetes treatment - but, due to their enormous and growing size, and the absence of any cure, both of these markets are fiercely contested via existing and new therapies developed by the big Pharma companies, as well as by hundreds of biotechs.

As such, it may be a small miracle if Fezagepras were to one day challenge current standards of care or generate best-in-class data. While I have said before that many small biotechs look like they are searching for the proverbial needle-in-a-haystack - right up until the moment they produce stellar data and the share price sky-rockets - it really would be a stretch to suggest that this may be about to occur with Feza and Liminal. Stranger things have happened in biotech, however.

Similarly to Feza, Liminal's preclinical assets - the GPR84 and OXER1 antagonists - appear to target promising areas of development - OXER, for example, is a G-protein-coupled receptor that is selective for 5-oxo-ETE - believed to be one of the most potent human eosinophil chemo-attractants and potentially a valuable target for lung or gastrointestinal disease.

The trouble is that Liminal is still unable to advise which diseases its candidate might target, with CEO Pritchard stressing that tackling the pre-IND process alone is occupying most of the company's time on the Q121 earnings call.

Conclusion - Good Financial Stewardship in recent months doesn't disguise speculative at best pipeline.

In some ways, it's hard not to feel sympathetic towards Liminal after its convalescent plasma bubble burst so quickly after the company looked to be finally turning a corner.

Instead, the fire sale of all assets related to its plasma therapeutics division for just $17m may just about solve Liminal's financial problems in the short term, while the company desperately clings to the potential approval of Ryplazim in June and the $50-$70m I estimate the sale of its Priority Review Voucher could earn.

It's hardly surprising therefore that the development of the small molecule pipeline has been somewhat slow, whilst other compounds remain at the preclinical stage. For one thing, management is very short on direct drug-development experience.

It's interesting to compare Liminal - with its market cap of $99m, 1 Phase, 1 asset, and 2 preclinical, to precision medicine drug developers such as e.g. Relay Therapeutics (RLAY) or Black Diamond Therapeutics (BDTX) - who currently have 1 clinical asset between them, and yet have market caps of $2.7bn and $811m, respectively.

It may be possible to make the case that a form of snobbery exists in biotech, where companies with more glamorous drug targets and technology, or deep-pocketed backers, garner valuations that run far ahead of their potential value, while biotech's like Liminal carry out similar development work without the benefits of a strong reputation fuelled by rumours of its super-powerful drug discovery technology.

In that scenario, it might be tempting to look at Liminal as an undervalued, albeit risk-on opportunity that has been overlooked and may just deliver something out of the ordinary data wise.

In the cold light of day, however, with the failure rate of drug-development candidates in the clinic as high as 4/5 or even 9/10, unless you have some inside knowledge concerning the efficacy of Fezagepras or are actively involved in the business, Liminal does not look to be attractive long-term hold.

Some investors may consider investing in Liminal ahead of the Ryplazim PDUFA date in June, which would surely deliver upside if approved, but the risk/reward profile - with Liminal's future as a going concern potentially under threat if Ryplazim is not approved - is not for the faint hearted.

Given Liminal's lengthy history of stalled development projects and the lack of drug development know-how, the company feels like a biotech to avoid investing a lot of money or faith into. I'm 50/50 on Ryplazim approval and the upside that may bring, but I can see any gains being eroded quite quickly after the event, leaving the Phase 1 Feza readouts as the only near-term catalyst.

I, therefore, do not foresee long-term upside for Liminal at this time, although I'm remaining neutral based on the prospect of a June Ryplazim approval.