Cushing Running Dry: JPM PM: "We Could Be Just Weeks Away From Cushing Effectively Running Out Of Crude"

Back in April 2020, the landlocked West Texas Intermediate crude oil price briefly crashed into negative territory - a stunning turn of events that cost traders massive losses - when the spot oil market found itself with an unprecedented glut as there was literally too much oil to be stored, and as such those traders who were assigned delivery would pay others just to take the physical oil off their hands. Well, in just a few weeks we may see the opposite scenario: no physical oil at all in the largest US commercial storage facility, leading to what may be a superspike in the price of oil.

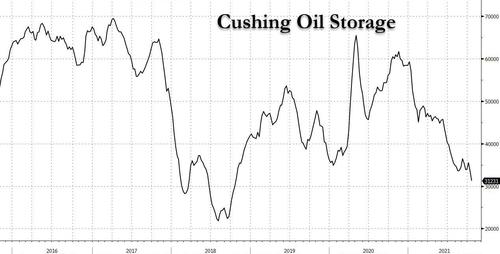

In a note predicting the near-term dynamics of the oil market, JPMorgan's commodity Natasha Kaneva writes that in a world of pervasive nat gas and coal shortages which are forcing the power sector to increasingly turn to oil (boosting demand by 750bkd during winter and drawing inventory by 2.1mmb/d in Nov and Dec), Cushing oil storage - which just dropped to 31.2mm barrels, the lowest since 2018...

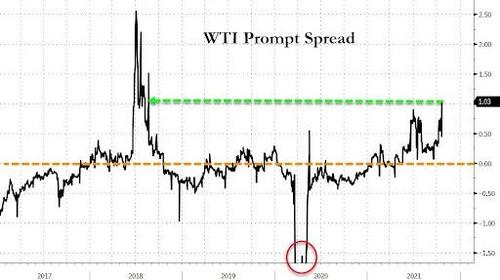

... may be just weeks from being "effectively out of crude." The bank's conclusion: "if nothing were to change in the Cushing balance over the next two months, we might expect front WTI spreads to spike to record highs—a “super backwardation” scenario."

Before we get into the meat of the note, first some background which as usual these days, begins with Europe's catastrophic handling of its energy needs.

As JPM notes, the heating season of 2021/2022 is opening with record high global gas prices even as cold winter weather has yet to arrive. Such are the quirks of the natural gas market that, when/if cold winter arrives, demand for gas tends to outpace any source of supply. In the US alone, in a given week in winter, natural gas demand can surge by 50-70 bcf, if not more, with limited response from supply. The situation is so dire at the moment that - JPMorgan observes - "finding even 1 bcf of spare capacity is becoming increasingly difficult."

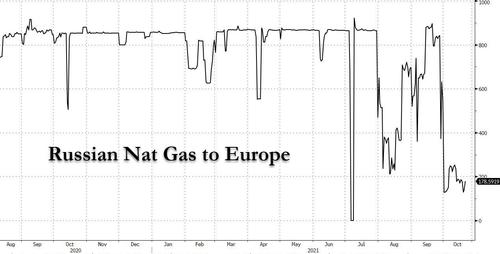

The good news is that with Russian domestic gas storage sites 97% full, stockpiling should be finalized by November 1, potentially freeing 4-10 bcm of additional shipments to Europe. However, on Monday we reported that Gazprom had booked only 35% of Yamal-Europe exit pipeline capacity for November (same as in October) and chose not to book additional transit volumes via Ukraine, implying that Russia is not currently planning to ship additional gas to Europe at least until Nord Stream 2 is fully authorized.

And as JPM notes, echoing what Goldman said earlier this week, "without additional Russian volumes, the winter weather premium currently embedded in the European natural gas price cannot significantly diminish until outlook for January weather becomes more certain."

In short, even higher nat gas prices are on deck, especially if the winter is cold.

So with record coal and gas prices, the power sector and energy intensive industries are turning to oil, potentially boosting demand by 750 kbd during winter and drawing oil inventory by 2.1 mbd over November and December. Earlier today, Reuters quoted Saudi Arabia's Minister of Energy Prince Abdulaziz bin Salman who confirmed that users switching from gas to oil could account for demand of 500,000-600,000 barrels per day (bpd), adding that the world was now waking up to shortages in the energy sector.

Abdulaziz said the potential switch depended on how severe winter weather would be and how expensive alternative energy prices would be. He outlined a wide range of factors that have led to a recent spike in energy prices, including limited investment in hydrocarbons and infrastructure, low inventories, the lifting of pandemic lockdowns and COVID-19 vaccine uptake rates.

"People all of a sudden woke up to the reality that they are running out of everything: they are ran out of investments, they ran out of stocks and they ran out of … creativity in trying to be attending to real solution that address real issues," Prince Abdulaziz told the CERA Week India Energy Forum.

In any case, in the clearest example yet of market tightness, Cushing crude storage fell to 31.2 mb last week as noted in the chart above. And because operational tank bottoms are likely 20-25% of capacity- or about 20 mb - JPM predicts that "we could be just weeks away from Cushing being effectively out of crude" and adds that "if nothing were to change in the Cushing balance over the next two months, we might expect front WTI spreads to spike to record highs—a “super backwardation” scenario."

If JPM's prediction is correct - and recall just yesterday we published a similar take from Morgan Stanley which now expects a similar "peak supply" scenario playing out, if over the longer term prompting the bank to hike its Q1 2022 price target to $95 from $77.5/bbl - it would have a catastrophic (read higher) impact on the price of oil.

Of course, there are potential mitigating factors: as Kaneva notes, though the dynamics of the US crude balance are different than they were in 2018 and much different than they were in 2014—the last two times Cushing drew down toward operational limits—the market still has a few levers to pull before we worry about such a scenario.

Today, the oil market is already reacting to the possibility that Cushing inventories bottom out and the export arb from the US Gulf Coast to Northwest Europe has been closed since 14 Oct. Consequently, the bank expects US crude exports to fall to an average 2.0-2.2 mbd by mid-November, with most of that ~500 kbd cut coming from flows to Europe.

But while this may be good news for the US, it's even more bad news for Europe - this reduction in flows to Europe would come at a time when European crude markets are already quite tight. According to data from Kpler, Europe crude oil stocks are already at their lowest since late 2018. Since 15 July, Europe crude stocks have fallen 35 mb, a rate of 362 kbd.

European exports aside, and focusing on Cushing inbound flows, JPM notes that last week the Steele City to Cushing section of the Keystone pipeline halted for three days as Keystone shifted flows to Patoka and the pipeline was still flowing at a much lower than normal rate early this week, though flows appear to be back above 400 kbd this morning.

Total Keystone flows fell on Tuesday as flows to Patoka slowed as well. If Keystone flows to Cushing—normally 350-625 kbd—return consistently to normal soon, Cushing would be much closer to balance. However, if the shift in flows is intended to serve as line fill for Capline, Keystone may not be a short-term solution to the Cushing tank bottoms issue.

Capline should require about 5.2 mb of line fill in total. With start-up not planned until 1 Jan, the rate of line fill should not be more than about 100 kbd. While this additional tightness in the PADD 2 crude balance certainly does not help matters at Cushing, it should be more than offset by the continued ramp up of the 760 kbd Line 3 Replacement, JPM suggests.

Finally, flows on the Enbridge Mainline group of pipelines, which includes the Line 3 Replacement, have only increased about 200 kbd since the start of Line 3, which means the potential for much more crude volume flowing into PADD 2 could be just across the horizon, assuming Canadian producers are willing and able to supply them.