Following up on my article “When will Cenovus or CNQ buy out MEG Energy?”

Things have evolved since Husky Energy tried to take out MEG Energy at $11/share back in October 2018:

At the time of the Husky offer, WTI oil was at US$75/barrel, MEG had 297 million shares outstanding (today they are at 307 million), and they had $3.2 billion net debt (today they are sitting at under $2.6 billion). Annual production in 2018 was 87.7 kboe/d, while in 2022 it will be around 95-96 kboe/d.

By all accounts MEG is in better shape today than it was 3 years ago. Will it be CVE or CNQ to first offer a stock swap for a 30-40% premium over the current price?

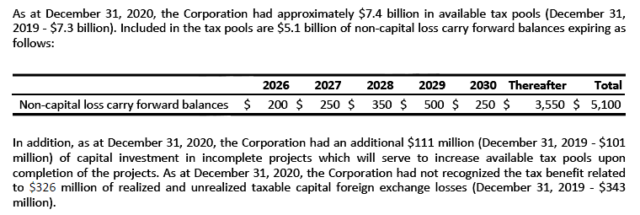

The big hidden asset not readily visible comes from the following two paragraphs on MEG’s financial statements:

With WTI at US$70/barrel, it will take a very, very long time to dig through these tax pools. Simply put, $5.1 billion in non-capital losses represents an additional $1.2 billion of taxes that can be bought off in an acquisition. With the way things are going, Cenovus will be able to eat through their tax shield mid-decade (they also inherited a tax shield from the Husky acquisition), and CNQ’s tax shield is virtually exhausted at this point (they did acquire some with their announced acquisition of Storm Resources on November 9th, but this will go quickly as Storm had about half a billion in operating loss and exploration credits).

Either way, this tax pool is a ‘hidden’ asset and will bridge the differential between the current market value and a takeover premium. Since valuations in the oil patch are still incredibly depressed (enterprise value to projected free cash flows are still in the upper single digits across the board), a stock swap makes the most sense.

Operationally this is the most likely course of action – without a major capital influx, MEG is constrained to around 100kboe/d of production and things will be pretty much static for them after this point. The only difference at this point is whether Western Canadian Select valuations rise (having Trans-Mountain knocked out for two weeks did not help matters any) and what the final negotiated value will be. The acquiring entity will be able to integrate MEG’s operations to theirs quite readily and shed a bunch of G&A after they pay out the golden parachutes.

Needless to say, I’ve had shares of this at earlier prices.