sframephoto/iStock via Getty Images

While it was a difficult year for the Gold Juniors Index (GDXJ), with a second consecutive negative return in 2022, it was an especially tough year for Calibre Mining (OTCQX:CXBMF) investors. This was incredibly frustrating for shareholders, given that the company continues to fire on all cylinders. Unfortunately, its 2200 basis point underperformance was mostly related to a degradation in sentiment regarding Nicaraguan mining operations, which impacts Calibre Mining ("Calibre"), given that ~80% of its production comes from within the country.

The good news is that despite the October news related to sanctions imposed on the Nicaraguan General Directorate of Mines by the United States Treasury Department, Calibre has no material impact on operations and finished 2022 with a record year of production. Additionally, the company expects ~24% growth in output from 2022 levels based on its two-year average forward guidance mid-point, giving it one of the best growth profiles within its peer group. Finally, this negative publicity surrounding Nicaragua has overshadowed exceptional exploration results, which could translate to meaningful reserve growth at its Limon Complex. Let's take a closer look below:

Calibre Operations (Company Presentation)

FY2022 Results & Forward Outlook

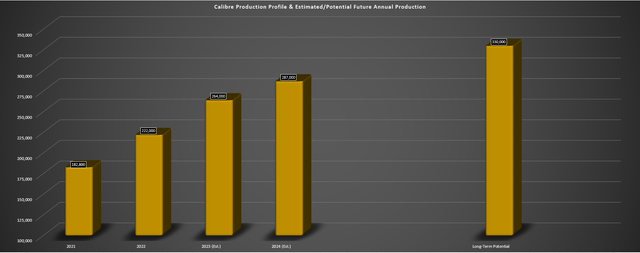

Calibre Mining released its preliminary Q4 and FY2022 results this week, reporting quarterly and full-year gold production of ~61,300 ounces and ~222,000 ounces, respectively. These results met the company's guidance of 180,000 to 190,000 ounces from its Nicaraguan Operations (~180,500 ounces produced) and its annual production guidance of 220,000 to 235,000 ounces despite an unplanned outage in the carbon plant that impacted Q3 results. Given the higher grades at its Nicaraguan assets and the additional contribution from its Fiore acquisition (Pan Mine), Calibre grew consolidated production by 21% year-over-year during a year when many miners struggle to achieve growth.

Calibre - Annual Gold Production & Forward Estimates (Company Filings, Author's Chart)

Looking ahead to FY2023, Calibre expects another strong year for gold production, benefiting from increased throughput at Libertad as additional high-grade mines come online. These include Eastern Borosi and Pavon Central, which should both be contributing by 2023 at the latest. The most exciting opportunity here is Eastern Borosi, with an average open-pit reserve grade of 6.8 grams per tonne of gold, nearly double the grades that Calibre has been feeding to the Libertad Plant (~3.70 grams per tonne of gold). This is expected to result in a significant increase in annual gold production to 262,500 ounces at the mid-point, but I would not be surprised to see a beat on this guidance mid-point for the year, translating to $140+ million in operating cash flow even at gold prices well below spot levels.

From a cost standpoint, Calibre has guided for all-in sustaining costs [AISC] of $1,225/oz at the mid-point in FY2023, with its margin performance dragged down by its higher-cost Pan Mine Nevada ($1,350/oz to $1,450/oz AISC). However, as production increases further in 2024 from its Nicaraguan operations, I expect AISC to dip back below $1,175/oz (consolidated basis), assuming we don't see further headwinds from a fuel cost standpoint with elevated oil prices. Finally, growth capital is budgeted at ~$60 million, with exploration capital at $25 to $30 million. The latter is very encouraging, with the company's aggressive exploration spending to date certainly paying off nicely. Let's take a closer look below:

Recent Developments

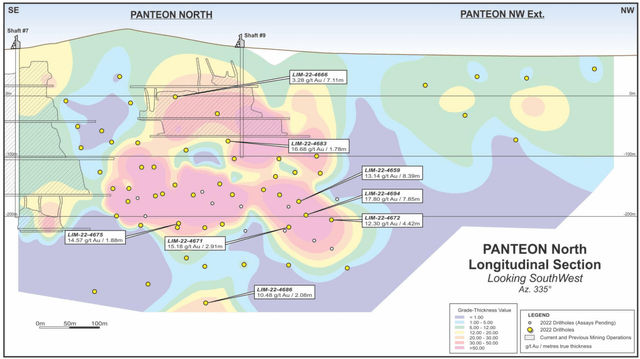

Moving over to recent developments, the major news for Calibre has been its continued exploration success, with the highlight of 2022 drilling being the discovery of the Panteon North zone. For those unfamiliar, this discovery lies just 1 kilometer north of existing operations at its smaller Limon Complex, and the grades intersected to date have been phenomenal. As shown below, Calibre has hit multiple 100+ gram-meter intercepts at Panteon North over very mineable widths, with some highlights including the following:

- 5.6 meters at 66.03 grams per tonne of gold

- 5.0 meters at 30.33 grams per tonne of gold

- 4.9 meters at 22.55 grams per tonne of gold

- 7.3 meters at 17.80 grams per tonne of gold

- 8.4 meters at 13.14 grams per tonne of gold

- 2.9 meters at 15.18 grams per tonne of gold

- 10.6 meters at 12.85 grams per tonne of gold

- 3.8 meters at 52.09 grams per tonne of gold

- 3.3 meters at 43.09 grams per tonne of gold

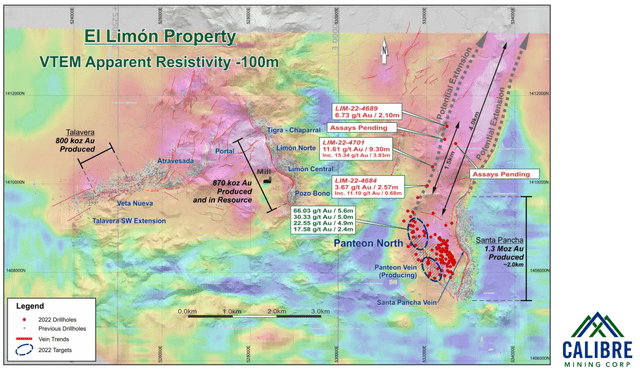

As of the most recent update, the company has defined a gold shoot that spans 400 meters along strike and 200+ meters down-dip, and the results appear to be consistently coming in above 7.0 grams per tonne of gold with multiple intercepts hitting half an ounce per tonne or better gold grades. This is very encouraging from a resource growth standpoint, but the company's new discovery a further 2.5 kilometers north of the Panteon North zone is just as exciting. The grades at this zone are also quite impressive, with highlight holes of 9.3 meters at 11.61 grams per tonne of gold, 3.9 meters at 15.34 grams per tonne of gold, and 2.1 meters at 6.73 grams per tonne of gold, suggesting the potential for material resource growth at its El Limon Property.

Panteon North Drilling (Company Presentation)

It's also worth putting these two new discoveries in context, and we can see below these two discoveries occur along just half of the interpreted potential extensions to the north, suggesting that Calibre could easily add 1.0+ million ounces of gold between Panteon North and additional deposits along strike to the north. This is especially important because these discoveries were not part of the company's multi-year growth plan that aims to increase production toward 300,000 ounces per annum (high end of 2024 guidance), and the grades at Panteon North appear to be as good (if not better) than the grades expected to be mined north at Eastern Borosi.

El Limon Property Map - VTEM Apparent Resistivity (Company Presentation)

So, why is this important?

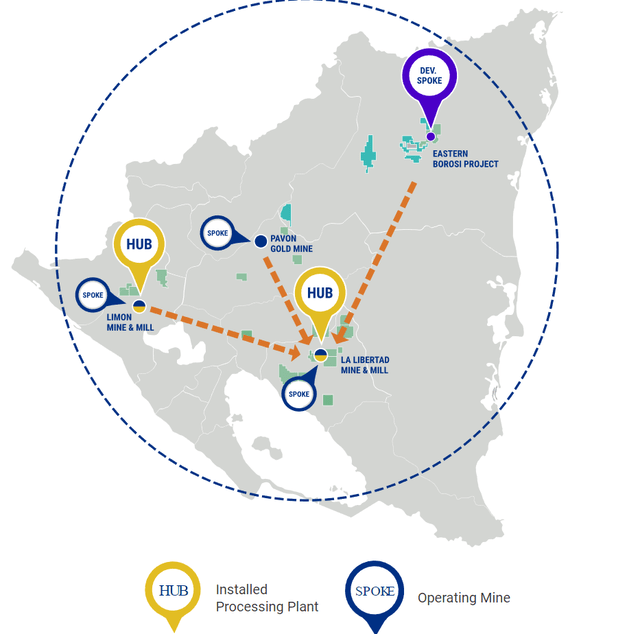

For those following the Calibre story, the company's Libertad Mill has a total capacity of ~2.2 million tonnes per annum, and the company is currently processing less than 1.2 million tonnes per annum at the facility. While the total tonnes processed at Libertad will see a boost from the additional high-grade feed from Eastern Borosi, it's possible that Panteon North and additional deposits could represent a new mining center and future spoke with similar grades to Eastern Borosi. The kicker is that this new discovery at the Limon Complex looks to have similar grades to its highest-grade spoke (Eastern Borosi) but is a much shorter distance, suggesting a savings of at least $15/tonne but with the benefit of similar grades coming to the mill.

Calibre Mining - Hub & Spoke Model Nicaragua (Company Presentation)

While it's still early days, the attractiveness of the Calibre Mining model is that it has considerably sunk costs at Libertad and that new high-grade discoveries can lead to a significant lift in production and much lower costs as it leverages existing capacity. So, with the potential for a second 6.0+ gram per tonne mine to feed Libertad, this is a significant upgrade to the investment thesis. Even assuming an average feed grade of 4.8 grams per tonne of gold and ~1.7 million tonnes processed per annum (77% of capacity) at a 92% recovery rate, this could push Libertad's annual production from ~100,000 ounces to 240,000 ounces per annum, and boost the company's total production to 350,000+ ounces even without its Gold Rock development project in Nevada.

So, while I previously saw the ability for Calibre to produce 330,000 ounces long-term (post-2025) with the addition of Gold Rock (a development asset in Nevada that requires state permits but is federally permitted), it looks like the actual opportunity could be 400,000+ ounces once Gold Rock is online. This is because the Nicaraguan operations alone could support 300,000 to 320,000 ounces per annum on the back of these new discoveries (~240,000 ounces per annum from Libertad and ~80,000 ounces from Limon), with an additional ~85,000 ounces from its Nevada operations depending on how it chooses to size Gold Rock from a throughput standpoint. With investors getting this impressive growth story for a sub $400 million market cap, this is undoubtedly one of the sector's better buy-the-dip candidates.

Valuation & Technical Picture

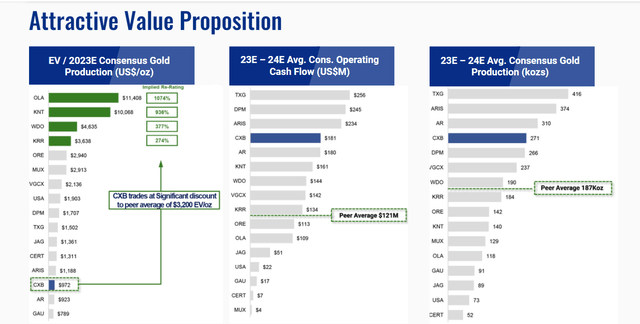

Based on ~497 million fully diluted shares and a share price of US$0.78, Calibre Mining trades at a market cap of ~$388 million. This is a dirt-cheap valuation for a ~270,000-ounce gold producer whose costs are expected to come in just below the industry average this year ($1,225/oz vs. ~$1,260/oz estimated industry average costs). Obviously, some discount should be applied given that more than 70% of the company's forward 2-year production is expected to come from a Tier-3 ranked jurisdiction (Nicaragua). Still, even if the company generates only $144 million in cash flow this year ($0.29), it would be trading at ~2.7x forward cash flow estimates if it stays at these levels, one of the cheapest valuations sector-wide.

Typically, a valuation this low is reserved for a company that has one or more of the following issues:

- it has a poor track record of delivering on promises

- it operates out of one of the worst jurisdictions globally

- it has extremely high costs, meaning it's very sensitive to the gold price

- a fragile balance sheet

In Calibre's case, its margins are quite respectable, with ~33% AISC margins at a $1,825/oz gold price. Meanwhile, it has a solid track record of delivering on promises and continues to exceed expectations from an exploration standpoint at its Limon Complex in Nicaragua. However, the one thing that is out of its control is that it operates in a jurisdiction that has received negative publicity, and a single headline related to expanded US-Nicaragua sanctions sent the stock down more than 40% last year despite no change to operations, with a similar blow delivered to Hochschild (OTCQX:HCHDF) in 2021 regarding its Peruvian Operations.

Calibre - Value Proposition (Company Presentation)

Unfortunately, Hochschild's stock has made new lows since due to poor reserve replacement, but Calibre continues to fire on all cylinders, and its stock has recovered most of its losses. So, with Calibre checking several boxes (reserve replacement, meeting/beating guidance, steady production growth) and working to improve its one weakness from an investment standpoint, I don't believe that the stock's deep discount to its peer group is sustainable long-term. That said, the market can remain irrational for a long period. As I pointed out in my previous update, although there hasn't been any change to operations, the perceived risk could weigh on the stock and result in underperformance vs. some of its peers.

Based on what I believe to be an ultra-conservative multiple of 3.7x cash flow to reflect the company's strong organic growth profile and high likelihood of resource/reserve growth offset by its less favorable jurisdictional profile, I see a fair value for the stock of US$1.07 [C$1.42]. This represents a 37% upside from current levels, suggesting there's still some upside from a valuation standpoint after this rally. However, I prefer a minimum 45% discount to fair value when sub $500 million market cap names, meaning that while I see the stock as cheap, it is not currently in a low-risk buy zone. For the stock to head into a low-risk buy zone, it would need to dip below US$0.58.

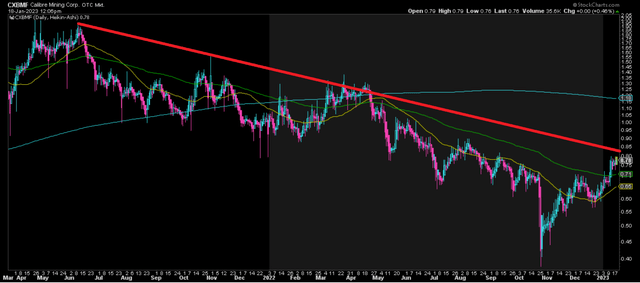

CXBM2-Year Chart (StockCharts.com)

Moving to the technical picture, Calibre has put together a ~105% rally within a long-term downtrend, and probabilities would suggest that the stock is likely to run out of gas soon as it approaches its downtrend line. Meanwhile, because the stock has wedged up the right side of its larger base with only very brief pauses, the next support level doesn't come in until US$0.57. So, with Calibre now sitting just a nickel away from potential resistance at US$0.81 to US$0.84 and having no strong support until US$0.57, the reward/risk is not remotely favorable, with a reward/risk ratio of 0.25 to 1.0 (the potential upside to resistance vs. potential downside to support). Hence, I don't see any way to justify chasing the stock here above US$0.77.

Summary

Calibre Mining had a solid year operationally amid several misses sector-wide. The bonus to the story is that the company continues to enjoy exploration success across its portfolio, with the stand-out success being the Panteon North discovery and multiple further high-grade hits north of this new discovery. Looking ahead to its production outlook this year, Calibre should easily produce 265,000 ounces of gold, and its operations will benefit from an additional spoke at Eastern Borosi and the start of mining at Pavon Central.

Having said that, while Calibre has a very attractive organic growth story and could be a top-10 growth story sector-wide if it continues to enjoy exploration success, I don't believe in chasing stocks. The issue today is that Calibre has found itself overbought short-term, even if there's further upside to what I believe to be a very conservative fair value of US$1.07. So, while I see Calibre Mining as a solid buy-the-dip candidate, I would need to see much lower prices to become interested in starting a new position.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.