HEYWOOD -I have a different # in mind.

At the time - I don't think smaller shareholders understood what moves from

2015 to present did to the small shareholder value till,... one disects every move.

Let's play suppose using just common shares.

500 million shares ( common )

- Imbedded former

- Electrum

- Resource Cap

- Drake

- Insiders ( 2016 forward junior )

----------------------

= 50 million remaing ??? ( small shareholders )

x $ ???

This is all about 2015 resource 329 mil tonnes + 846 mil tonnes

It's about no iron credit or factoring other avail minerals

It's about dismissing solid solution nickel +plat group

It's about not separating pgm's from magnetite

It's about recharacterization of, geology / boundary / upper / lower

It's about testing sulphides and gabbs later.

It's about extraction can't handle crystalines ( Clino high grade )

2017 separated all the high grades from resource.

Sulphides, Gabbs, Clino.

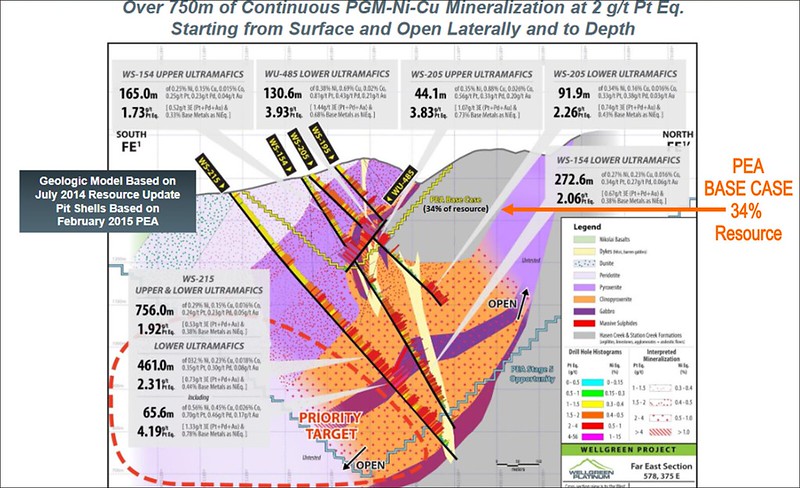

Thank goodness for Johnson's first image. Grades along drill hole reveal the high grade 2.4/g Pt Eq

Tells us what's really below the 1st and 2nd mountains ( high grade ores )

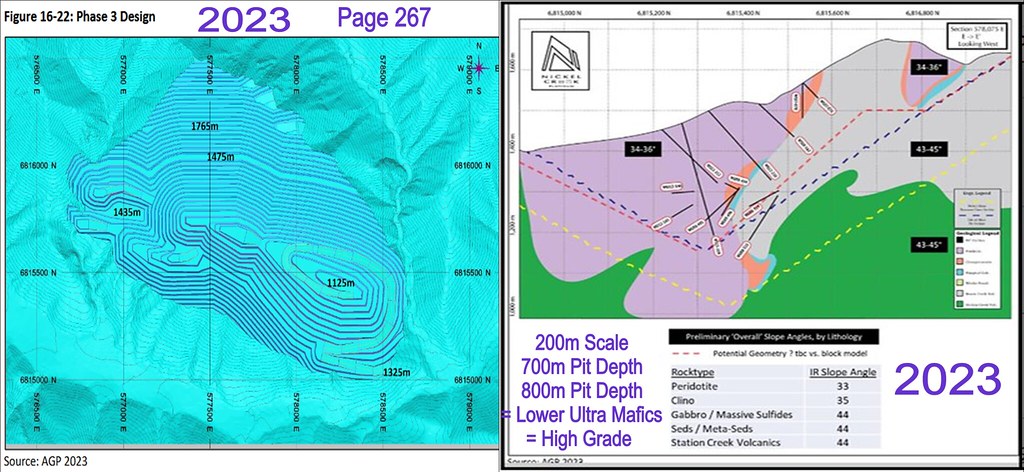

Two 2023 pit image comparison

Two 2023 pit image comparison 1st image = 1125 m pit depth

vs

2nd image 1125 m ( 700 m pit depth ) this depth captures high grades

2nd image shows the pit depths

Yet.... this 2nd image converted all the good ores to peridotite.

High grades ( 3 geologies ) removed.

Yet... what does Johnson's image above show ?

Massive high to 700+m at depth.

Is one mining 594.6 million tonnes of waste lol

https://live.staticflickr.com/65535/53585015681_3aeba8eac5_c.jpg First thought comes to mind - 846 million inferred tonnes

Separate ( junior, large holders ) from ( small holders )

Cheap resolution.... after all... wellgreen resource was founded on

2015's ug mine - main focal - 2013 assays.

Imagine what $125 million could do ? ( my own est )

Not investment advice.

Perform your own DD.

I maybe right, wrong, but then again i might be bang on.

Wango~