Jeepers - not good reviews for Tilray

You’re reading this week’s edition of the New Cannabis Ventures weekly newsletter, which we have been publishing since October 2015. The newsletter includes unique insight to help our readers stay ahead of the curve as well as links to the week’s most important news. We post this and all of the newsletters on our website here.

Friends,

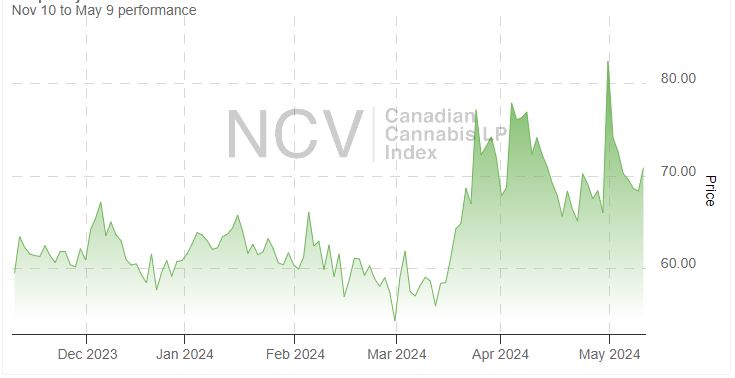

Near the end of Q1, we shared a warning about the Canadian LP market, which had soared after the Legislative Review of the Cannabis Act. The New Cannabis Ventures Canadian Cannabis LP Index rallied the day we ran the newsletter, dropped and then rallied back in early April. Then, it sold off a lot, and we suggested that cannabis investors should not ignore Canada. Here is teh action over the past six months:

The index has lifted substantially from its all-time low set at the end of February, and it is up 16.4% in 2024. There are six Canadian LPs in the NCV Global Cannabis Stock Index, which has rallied 29.1% so far in 2024. Those six stocks in the index are up an average of 40.4%:

All are up more than the Global Cannabis Stock Index except for Tilray Brands, which has dropped 14.2%. I continue to think that the stock could move a lot lower, as it seems to be overvalued relative to peers. It trades at 3.9X tangible book value. My favorite LP, Organigram, has pulled back and is up less than the average. One that I like a lot, Village Farms, is not in the index, and it has rallied 72.1%. I include a large position in Organigram and a small one in Village Farms my model portfolio at 420 Investor. Both of these stocks trade below tangible book value.

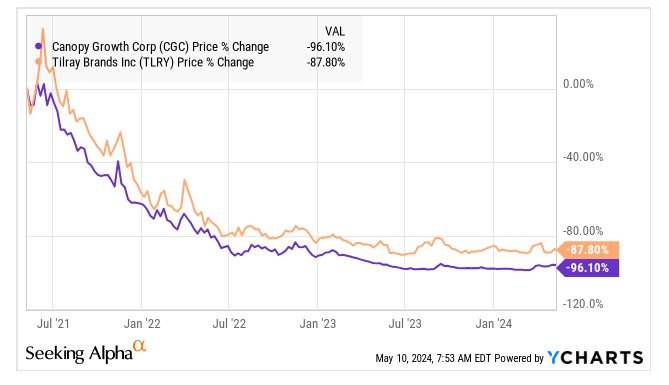

The best stock in 2024 of the six LPs that are in the Global Cannabis Stock Index has been Canopy Growth. Its fiscal year ended at the end of March, and it will report its Q4 results this quarter. It still hasn’t scheduled a date. The market cap is currently over $1.3 billion and more than 3.4X tangible book value. The NASDAQ still has not ruled on the move that Canopy Growth is making to acquire American cannabis companies and maintain its NASDAQ listing. The company isn’t doing well in Canada, and it has a negative projected adjusted EBITDA for FY25.

Canopy Growth and Tilray Brands, which both have market caps above $1 billion, are very popular with investors despite their terrible performance over the past five years:

Some investors like to buy stocks that are down a lot, and both of these are down more than the Global Cannabis Stock Index, which has lost 81.8% over the past three years. We suggest that investors look at the valuations! There are much better deals in the market than Canopy Growth and Tilray Brands in our view.

The Canadian cannabis market is maturing, and we are not sure why investors would chase these two stocks. Several other Canadian LP stocks trade below tangible book value and aren’t carrying large debt loads. There had been some speculation that Canada would address the tax challenges, but it failed to do so recently.

The Canadian LPs are having a good year so far, but we suggest that investors be cautious, especially regarding Canopy Growth and Tilray Brands. The excitement about cannabis stocks this year has been mainly due to the potential rescheduling, which would have no impact on either of these companies.