Tangible Book Value "Intangible assets are excluded from the tangible book value calculation because such assets cannot be liquidated and sold off. For instance, an intangible asset like goodwill is recognized on a company’s balance sheet for accounting purposes to capture the excess purchase price paid over the fair market value (FMV) of an asset."

Read the below as many times as you like quinlash - accurate book value is 'tangible book value'.

Book value is what is left if a company shuts down - the assets minus the liabilities if the CASH left over and distribuetd to shareholders.

Intangibles DO have value - but goodwill has no cash value at liquiditation. Things like IP would have to be sold - if they could be sold, but the value is determiend by the potential buyer - not what the company estimated it's value at.

THis book value thing is probably one of the dumbest arguments I've seen on the board - are yous aying that TKRY is shutting down and you're trying to determine how much shareholders will receive? Because THAT is what book value is.

Yes - low share price CAN be an indication of an under valued stock, but it doesnt mean the shares ARE actually undervalued. There are reasons why the share price would be lower - and TKRY has lots of reasons, you shoudl actually read the q1 financials yourself

You keep posting about BV - what BV do you show for Tikray?

What is Tangible Book Value?

The Tangible Book Value (TBV) represents the value of a company’s tangible assets, net of any intangible assets such as goodwill.

How to Calculate Tangible Book Value (TBV)?

The tangible book value (TBV) measures how much a company’s tangible assets are worth, excluding its intangible assets.

- Tangible Assets: Physical Assets (e.g. Cash, Inventory, PP&E)

- Intangible Assets: Non-Physical Assets (e.g. Intellectual Property, Copyright, Patents, Trademarks, Goodwill)

Conceptually, the tangible book value (TBV) is the residual net value of a company that belongs to common shareholders post-liquidation, i.e. the remaining value once all outstanding liabilities like debt are repaid.

Intangible assets are excluded from the tangible book value calculation because such assets cannot be liquidated and sold off.

For instance, an intangible asset like goodwill is recognized on a company’s balance sheet for accounting purposes to capture the excess purchase price paid over the fair market value (FMV) of an asset.

Since only tangible assets are included in the calculation, the TBV is a closer estimate of the value of a company if it were to hypothetically file for bankruptcy and undergo a liquidation.

However, TBV is still an approximation rather than the actual value of a liquidated company, since certain intangible assets can still in fact be sold and the liquidation value of tangible assets is rarely perfectly equal to the full value recorded on the books.

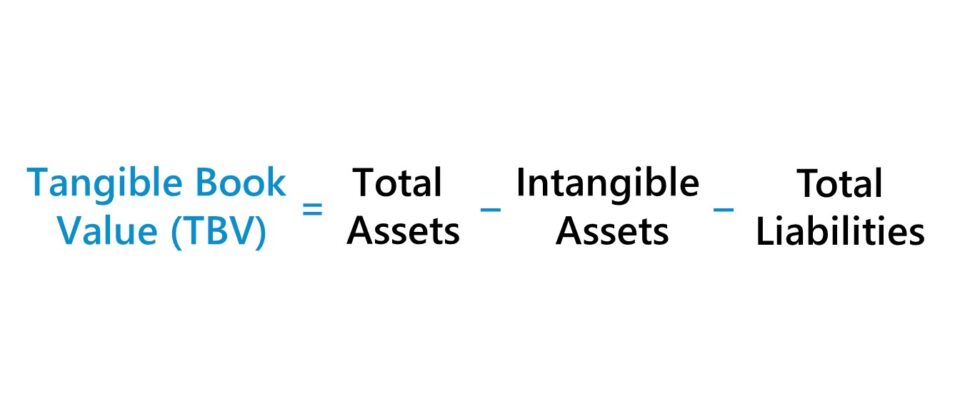

Tangible Book Value Formula (TBV)

The formula to calculate the tangible book value (TBV) is as follows.

Tangible Book Value (TBV) = (Total Assets – Intangible Assets) – Total Liabilities

The first part of the equation – i.e. total assets minus intangible assets – results in the value of a company’s tangible assets.

The value of all outstanding liabilities is then deducted from the value of the company’s tangible assets because claims such as debt and accounts payable are of higher priority and must be fulfilled before any proceeds can be distributed to common equity shareholders.