Doran Clark

What

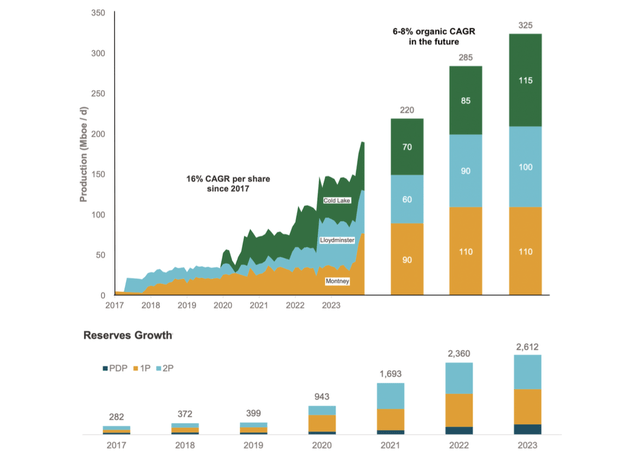

Historically, Strathcona Resources Ltd. (OTCPK:STHRF) expanded its production at a compound annual growth rate (or CAGR) of 16% on a per-share basis, which has been supported by per-share 1P reserve growth at a CAGR of 19%, as shown in Figure 1.

Fig. 1. Historical and projected production and reserves growth of Strathcona Resources (modified from Strathcona Resources)

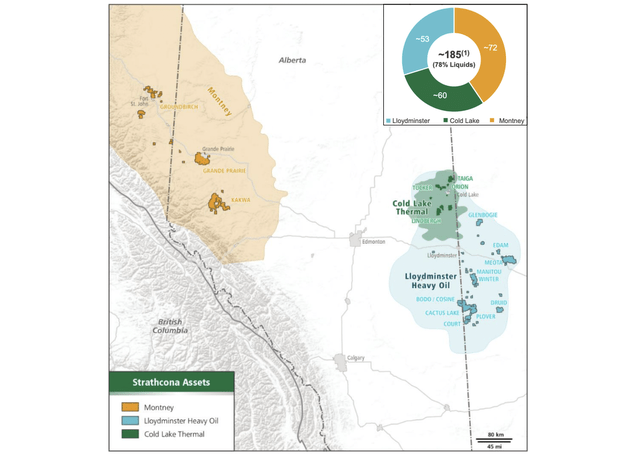

Going forward, Strathcona expects to achieve organic growth at a CAGR of 6-8%. To that end, Strathcona reported its second quarter 2024 financial and operational results last week. In the quarter, the company produced at a quarterly average of 181,766 boe/d (78% liquids, 22% natural gas) from its three operating areas including Montney, Lloydminster heavy oil, and Cold Lake thermal as illustrated in Figure 2, up an impressive 26.4% from 143,778 boe/d in Q2 2023.

Fig. 2. Production contribution of Strathcona's three operating areas, including Montney, Lloydminster heavy oil, and Cold Lake thermal (modified from Strathcona Resources)

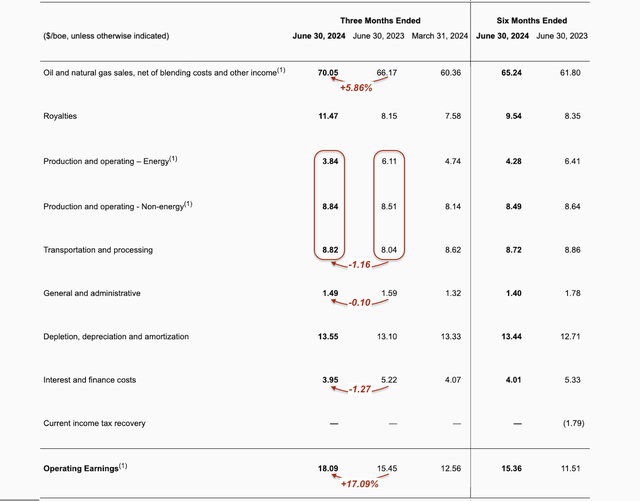

Strathcona managed to reduce the ex-G&A operating expenses (OpEx) for the quarter to C$21.50/boe, down from C$22.66/boe in Q2 2023, and cut G&A expenses to C$1.49/boe from C$1.59/boe one year ago. Thanks to the OpEx decline, the company was able to transform a 5.9% increase in realized total price into a 17.1% gain in operating earnings, as shown in Table 1.

Table 1. Operating results of Strathcona Resources in the Q2 2024, Q2 2023, and Q1 2024 on a C$/boe basis (modified from Strathcona Resources)

On the back of 26.4% production growth and a 17.1% gain in unit operating earnings, Strathcona generated operating earnings of C$306.1 million (C$1.43 per share) and free cash flow of C$247.3 million (C$1.15 per share), up 46.5% and 56.6% year over year, respectively. Quarterly capital expenditures were C$297.4 million, up 28.4% from C$231.7 million one year ago. The company will continue to have no current cash taxes until 2027. Strathcona converted 108.8% of the quarterly net income into free cash flow, attesting to the quality of its earnings.

So what

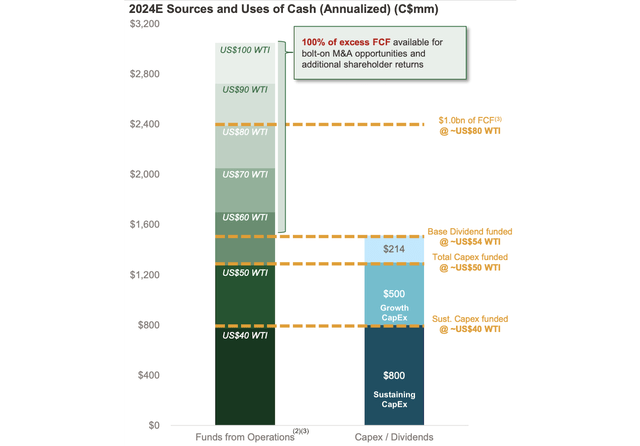

Strathcona Resources has stated that once the C$2.5 billion debt target is reached, it will allocate 100% of the excess free cash flow beyond the base dividend to additional shareholder returns and/or bolt-on M&A opportunities. The company successfully reduced debt from C$2,898.2 million one year ago to C$2,435.6 million by the end of the second quarter, achieving its debt target. As a result, the company declared its inaugural base quarterly dividend of C$214 million as illustrated in Figure 3, which comes to C$0.25 per share to be paid on September 27, 2024, to shareholders of record on September 16, 2024, with an implied base dividend yield of 3.24%. The company explained:

"The base dividend has been sized to increase Strathcona's full-cycle WTI breakeven by less than US$5 / bbl, ensuring it remains durable at trough periods of the oil price cycle. In turn, Strathcona's board of directors will consider potential future increases in the base dividend based on growth in Strathcona's oil production and / or reductions in Strathcona's full-cycle breakeven."

Fig. 3. Sources and allocation of cash in C$ millions for 2024, estimated under a production guidance of 185,000 – 190,000 boe/d, and assumptions that the WCS differential equal to 10% x WTI + US$5/bo, FX = 1.50 – 0.15% x WTI, and AECO per Mcf = US$ WTI / 25. (modified from Strathcona Resources)

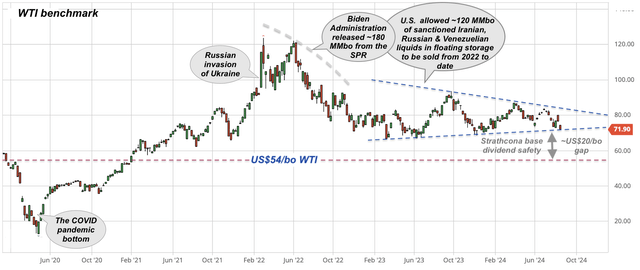

Strathcona exercised a great deal of conservatism in declaring the C$0.25 per-share quarterly base dividend. As long as WTI remains above US$54/bo, the company will be able to generate enough free cash flow to cover the base dividend, as shown in Figure 4. In other words, the base dividend has a high level of safety. I expect the base dividend to be raised by at least 6-8% per year in the next few years as organic growth in production continues, or at a faster pace if the company makes further acquisitions.

Fig. 4. WTI benchmark oil price, shown with major events, in relation to Strathcona dividend safety (Laurentian Research)

Additionally, if WTI averages US$80 this year, Strathcona will generate approximately C$514 million of excess free cash flow after base dividends. The company may use that excess FCF for bolt-on M&A opportunities and/or additional shareholder returns. Even if one half of the excess FCF is allocated to special dividends, the total dividend yield would be as high as 7.1%.

In summary, I am pleased with the second quarter results reported by Strathcona: its impressive production growth, well-controlled costs, achievement of its debt target, announcement of inaugural dividends, and management that is running a tight ship.

Now what

Year to date, Strathcona Resources - the newest large-cap heavy oil producer in Canada - has been one of the best performers among Canadian E&P stocks, as investors were attracted by its deep undervaluation created as a result of the selloff following its stock market debut through the reverse takeover of Pipestone Energy, as illustrated in Figure 5.

Fig. 5. Stock chart of Strathcona Resources, shown with WTI benchmark oil price (modified after Seeking Alpha)

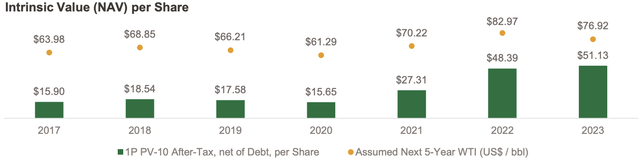

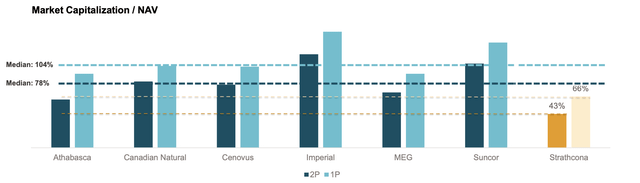

However, even after the share price appreciation, Strathcona is still a deep value relative to its free cash flow, net asset value and heavy oil producing peers, judging from its current P/FCF multiple of 6.7x, 60% of the 1P net asset value, or US$4.43/boe of 1P reserves, as shown in figures 6 and 7.

Fig. 6. Net asset value per share of Strathcona Resources. NAV reflects market cap as of July 31, 2024, divided by year-end 2023 after-tax 1P or 2P PV-10, less debt as of year-end 2023, with the market value of any downstream operations added to peer upstream NAVs based on BMO estimates, as of April 2024 (Strathcona Resources)

Fig. 7. A comparison of Strathcona Resources and its oil sand producing peers in terms of the P/NAV metric (Strathcona Resources)