I've read severa lreports now, and dependent upon which cut off used, the indicated + inferred all read differently.

Braveheart i noticed is running with, 1.51 million tonnes of copper, gold and silver mineralized material in indicated resources with an average copper equivalent grade of 2.263% CuEq. While the 2018 ( Gallowai prior owner ) ran with, In November 2018, an updated mineral resource estimate for the Bul River deposit was reported at 2.179 million tonnes indicated grading 1.517 copper, 0.352 gram per tonne gold and 12.2 grams per tonne silver and 0.513 million tonnes inferred grading 1.279 per cent copper, 0.284 gram per tonne gold and 8.7 grams per tonne silver, using a 0.6 per cent copper equivalent cut-off grade and a minimum mining width of 2.5 metres (Bird, S. (2019-01-22): NI43-101 Technical Report - Gallowai-Bul River Resource Estimate).

SOURCE - https://minfile.gov.bc.ca/summary.aspx?minfilno=082GNW002 Braveheart's 2021 estimates are shy when compared to Gallowai's 2018 report - - 669,000 tonnes ( indicated )

- no inferred mentioned.

With in one of the - Gallowai reports - It states Gallowai was granted a - small mining permit - 75,000/t per year.

I couldn't help but think, what if Braveheart ran - 2 - small mining permits ?

- Alpine

- Bull River

Both mines contributing - 75,000 tonnes perr year. Alpine - try to maintain a 22/g high grade

6,350 tonnes per month (

211 tonnes day ) x 12 = 75,000/t year.

x 22g

= 137,500 grams / gold x 87% recovery ( using former Gallowai's stats )

= 116,875 ~ 31.1

= 3,846/ounces

x 2,000/cdn

= $7,692,000/ cdn COPPER STOCKPILE ( 75,000/t ) 2200 ( tonne ) x .015% ( chose .015% though... over 3% grade was reported )

= 33/lbs copper per tonne

x 6,250/t per month

= 206,250 lbs copper

x $4.50/lb US

x $5.40 cdn = $ 1,113,750.00 cdn

X 12 months

= $13,365,000.00 cdn COMBINED ( hypothetical )

$21,057,000.00 cdn / year As you may have noticed, i chose full value of copper spot, in plight of, hoping the junior rethinks their mine model and " just maybe " entertains the purchase of, electrolysis - enabling full capture of copper profits- why piss it away with a concentrate - right ?

As per Alpine maintaining a 22/g average - is most like in fram land - but... one never knows.

I shudder the tohught when thinking Hearte gold and how they painfully couldn't maintain thier

7.1 gram average and suddenly fell short to - 6.1/grams.

750/tonne per day operation would certainly up the profits. 750 tonnes

x 365 days

= 273,750 tonnes per year

Based on Gallowai's report - Bul River deposit was reported at

2.179 million tonnes indicated grading 1.517 copper

2,179,750 tonnes

~ 273,750 tonnes ( current mill )

= 7.9/year operation ( not including the inferred )

+ 165,000/t - stockpile tonnage = 9 year operation ( not including inffered )

Inferred can run from 500k to 1 million tonnes,

dependent upon which report one read and cutoof.

Which if inferred was proved - it could push it into a 11 - 13 year operation. ( give or take )

What's Braveheart thinking ?

6.5 year operation but with the caveot of, based on increased production -

uhhh... the 750/t per day mill makes this a sweet lil project - with a running year class of,

9 - 13/yrs ( give or take )

INCREASED PRODUCTION ?

I have a hard time weith this, given the estimated reosurce belwo grade and the current 750/t day mill makes it a perfect fit. Any larger the operation becomes a quick fly by night - job wise and comminity wise - and longer 20+ yrs and like any mining peroject it becomes an isore.

Logic dictates, an evaluation should be based on - current infastructure is already there, resources proved and a - hangman - all upon increased production and drystacking.

How about placing - 20 copper juniors on the table with no mine to speak of, then, pull forward Bull River - that's how you assess which project should be put into production. own opinion.

In the mean time... Junior,

has to continue to advance, and hope they keep the interest of the investor, while their stock is tethered by a silly requirement. I can put those words into a different translation which might spell, junior tethered and forcedd ot dilute while larger fish curcle and laugh it up.

To conclude my research on Braveheart...

Gallowai's report mentions - open pit mining was practiced -

And... was stopped due ot depletion of ores.

Or, was there another reason,like, lower grad eores ?

What if the pits still had, 1% copper ?

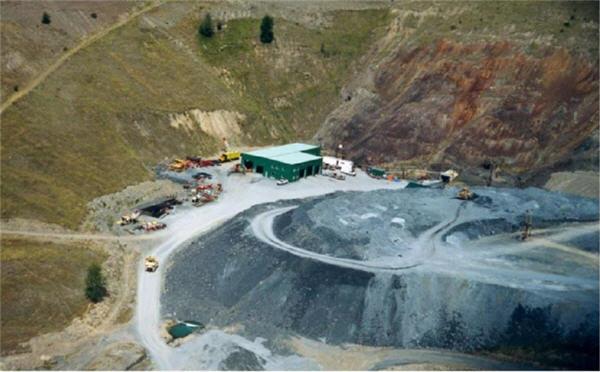

Now... i have since looked at more pics of Bull River's landscape, and well,

I'm seeing volcanics or argilites at surface and perhaps an extention outwardly fro mthe former open pits....

My question is... could the pits have more copper ores that might have been considered lessor grade and thus, provoked the past miner to seek to create an underground mine ?

What if, there was a solid 1% copper in what appears

to be exposed darker ores flanking the open pit walls ?

Have these open faced walls ever been sampled and assayed ?

All other photos i've seen show the mine site as flat terrain.

Yet.. .this pic - yeah.. .this pic has some interesting characteristics.

= look at those side walls. ( dark, perhaps argilites, and sulphides )

Perhpas Braveheart should do a retake - and sift the stockpiles ot see if al lthe copper ores

are from veining or, more like, argilites.... ?

Hence, could the open pits harbor more copper ?

Copper prices back then are no where near what they are now.

A 1% copper grade is considered very sweet.

And... could those ore blocks between each drift, contain copper outside the veining have they ever drilled the host rock ourside veining to see if copper is present ?

That's all i've gotr shareholders....

Short and sweet study.

Cheers....