WELL Health Technologies (TSE:WELL) Seems To Use Debt Quite Sensibly

Published

Source: Shutterstock

Source: Shutterstock David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that WELL Health Technologies Corp. (TSE:WELL) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for WELL Health Technologies

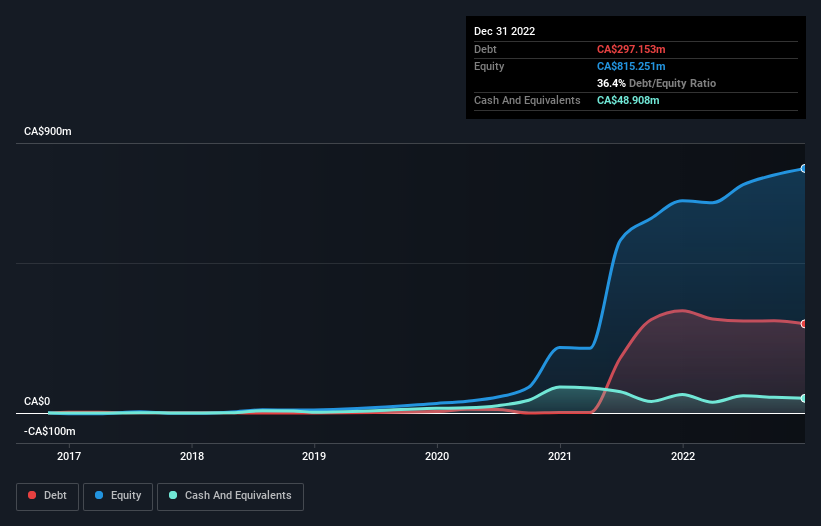

What Is WELL Health Technologies's Debt?

The image below, which you can click on for greater detail, shows that WELL Health Technologies had debt of CA$297.2m at the end of December 2022, a reduction from CA$340.7m over a year. On the flip side, it has CA$48.9m in cash leading to net debt of about CA$248.2m.

TSX:WELL Debt to Equity History April 18th 2023

TSX:WELL Debt to Equity History April 18th 2023 How Healthy Is WELL Health Technologies' Balance Sheet?

Zooming in on the latest balance sheet data, we can see that WELL Health Technologies had liabilities of CA$136.5m due within 12 months and liabilities of CA$367.3m due beyond that. Offsetting this, it had CA$48.9m in cash and CA$95.8m in receivables that were due within 12 months. So it has liabilities totalling CA$359.0m more than its cash and near-term receivables, combined.

While this might seem like a lot, it is not so bad since WELL Health Technologies has a market capitalization of CA$1.23b, and so it could probably strengthen its balance sheet by raising capital if it needed to. However, it is still worthwhile taking a close look at its ability to pay off debt.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

While we wouldn't worry about WELL Health Technologies's net debt to EBITDA ratio of 3.1, we think its super-low interest cover of 1.3 times is a sign of high leverage. It seems that the business incurs large depreciation and amortisation charges, so maybe its debt load is heavier than it would first appear, since EBITDA is arguably a generous measure of earnings. So shareholders should probably be aware that interest expenses appear to have really impacted the business lately. The silver lining is that WELL Health Technologies grew its EBIT by 2,172% last year, which nourishing like the idealism of youth. If it can keep walking that path it will be in a position to shed its debt with relative ease. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine WELL Health Technologies's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Happily for any shareholders, WELL Health Technologies actually produced more free cash flow than EBIT over the last two years. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Our View

WELL Health Technologies's conversion of EBIT to free cash flow suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14's goalkeeper. But we must concede we find its interest cover has the opposite effect. We would also note that Healthcare industry companies like WELL Health Technologies commonly do use debt without problems. When we consider the range of factors above, it looks like WELL Health Technologies is pretty sensible with its use of debt. While that brings some risk, it can also enhance returns for shareholders. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. For example - WELL Health Technologies has 2 warning signs we think you should be aware of.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

Valuation is complex, but we're helping make it simple.

Find out whether WELL Health Technologies is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

Vi