For seasoned gold mining investors, the name “Val d’Or” requires no introduction. The Val d’Or Gold Camp is part of Canada’s most prolific gold-producing region: the Abitibi greenstone belt. This world famous geological formation has already yielded roughly 200 million ounces of gold, with much of that total coming from the Val d’Or Camp itself.

The Camp takes its name from the city of Val d’Or, located in the Province of Quebec, roughly 500 kilometers northwest of Montreal. It was a focal point of an investor presentation at the 2017 Sprott Natural Resource Symposium, held from July 25 – 28 in Vancouver: Val d’Or Quebec – In the Heart of a World Class Gold District.

The presentation was made by Dr. Eric Owen, the President, CEO, and Founder of Alexandria Minerals Corp. While Owen’s primary emphasis was on the growth and development of Alexandria’s Val d’Or assets, much of what he passed along to the audience was applicable to the collection of junior gold mining companies inhabiting this highly prospective neighbourhood.

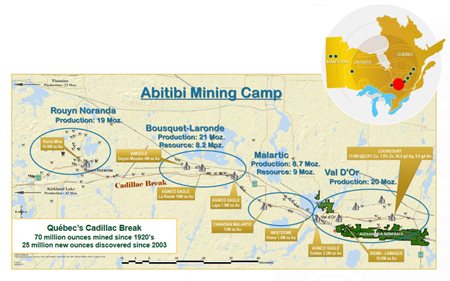

(click to enlarge)

That “neighbourhood” is centered along the Cadillac Break fault, the dominant geological trend in this gold camp. The string of gold mines (past and present) situated along this fault are a testament to the economic potential of this mining district. But Val d’Or is not a historical story.

The Camp not only remains a vibrant gold-producing district today, but the junior exploration companies operating here continue to strike and develop more robust gold resources. The significance of this fact explains why Val d’Or is back in the spotlight in the gold mining industry.

The gold mining industry, as a whole, is currently in a state of crisis. This crisis is a direct function of two factors:

- A suppressed gold price which is currently well below the price level required to make the industry sustainable.

- Extreme short-sightedness on the part of senior gold producers.

Addressing the second point first, the senior gold producers are generally not “mining companies” in the true sense of the term. These large corporations produce most of the world’s gold. But they find almost none of this gold, and they do very little to actually develop their gold projects.

While these companies mine millions of ounces of gold per year, they have done almost nothing in recent years to replenish the gold reserves which have been mined-out. The result of these gold producers grossly neglecting their own supply chains is both obvious and predictable. Gold mine reserves have been steadily falling, and, globally, mine reserves are now at a 30-year low.

If the senior gold producers don’t start adding millions of ounces of reserves to their holdings every year, these corporations will simply cease to exist. This begs an obvious question. How (or where) will these senior gold producers obtain these millions and millions of ounces of gold in the ground?

The senior gold producers do virtually no exploration of their own. This is how these companies pretend that their “all in” costs of gold production are so low. If they did all their own exploration and development of these gold projects, this would add somewhere in the vicinity of $500/oz to their cash costs.

What do these corporations do instead of organically developing their own projects? They write cheques. The bankers running these large gold corporations wait until some junior gold mining company has discovered and developed some highly prospective, multi-million ounce gold deposit (at considerable expense). Then they either buy the project or simply buy the company.

Typically, these senior producers overpay for these projects. By the time they invest the cap-ex necessary to take these deposits into production, little profit is left over for shareholders. This is also a function of the below-sustainable gold price.

Where can these senior gold companies replenish their reserves, in a hurry, in a safe jurisdiction with ample infrastructure and a skilled workforce? Val d’Or. This is not speculative. Eric Owen presented the audience attending the presentation with a prime example of how and why Val d’Or is back in the gold mining spotlight: Integra Gold.

On May 15, 2017; Eldorado Gold Corporation, a mid-tier gold producer, announced the acquisition of Integra Gold Corp., in a transaction which just recently closed. The deal was comprised of $129 million (CAD) in cash and 77 million ELD common shares, equating to a price tag of $590 million (CAD) – roughly $450 million (USD).

Even with a share count of close to 500 million, this represented a price in excess of $1/share. What is important to note is that as recently as 2014, the Company had a share price down around $0.10, with a market cap of approximately 1/10th of its purchase price. A ten-bagger for those buying in at that time.

A recent Stockhouse article also highlighted this renewed focus on M&A activity in the gold mining sector. That article pointed to another $500+ million acquisition of a junior gold company: Goldcorp’s $520 million purchase of Kaminak Gold Corp.

The relevance here is that there are several Val d’Or juniors with projects and properties which, as part of the same geological formation, exhibit considerable similarity with the assets of Integra. Today, most of these junior exploration companies are sporting market caps very similar to Integra’s old market cap.

The question which all gold mining investors should be asking themselves today is a simple one. When these extremely hungry, larger gold mining companies pull out their cheque-books next, who will they be buying, and how much will they pay?

For gold mining companies with a large appetite, there is plenty on the “menu” in Val d’Or. Several of these companies are already familiar to the Stockhouse audience:

Alexandria Minerals Corporation (TSX: V.AZX, OTCQB: ALXDF, Forum)

Dr. Eric Owen, President and CEO: Alexandria Minerals is a gold exploration company. Our focus is on a large land package in the Val d’Or (Quebec) Mining Camp, one of the world’s premier gold mining districts. We have discovered and identified a series of high-grade, gold veins. We have now been able to extend that footprint of high-grade veins to about 1.1 kilometers [of strike length]. We are neighbours of Integra Gold, and we have a higher potential for resource growth because we have a much larger property package. We are currently drilling a 30,000-meter drill program and plan on updating our resource later this year.

Cartier Resources Inc (TSX: V.ECR, OTCQB: ECRFF, Forum)

Knick Exploration Inc (TSX: V.KNX, Forum)

Jacques Brunelle, President and CEO: The 2017 drilling campaign on Knick Exploration Inc.’s (TSX-V: KNX) Trecesson Gold Property returned a substantial intersection of 94.4 g/t gold over 6.65 meters. Adjacent sections returned 3.2 g/t gold over 2.20 m and 3.8 g/t gold over 3.30m. These intersections are located at shallow depths, -35 meters or less. This area is indicative of a potential 100 meter long dilation zone within the system which calls for drilling at depth. The company’s Phase III drill program is planned for this fall upon completion of its present financing of 1M. The drill program will be focused primarily on drilling at depth in pursuit of defining a gold resource.

Feed or die. Either senior gold mining companies load up on new gold resources to replace what they have mined-out, or they cease to exist (as gold mining companies). In a world where accessible, commercially-viable, multi-million ounce gold resources are becoming increasingly rare, there will be more acquisitions and take-outs of Val d’Or projects – and companies.

For gold mining investors who have had little to show for their patience over the past several years, this pending feeding-frenzy offers the clear potential to make up for lost time.

FULL DISCLOSURE: Alexandria Minerals Corp, Cartier Resources Inc, and Knick Exploration Inc are all paid clients of Stockhouse Publishing.