This is not another story about global warming. The “heat” being generated in Canada’s far north by the gold mining industry is economic heat. As gold mining companies hunt for increasingly elusive projects which offer both robust grades and multi-million ounce potential, more and more of these companies are looking north – as in far north.

This is not another story about global warming. The “heat” being generated in Canada’s far north by the gold mining industry is economic heat. As gold mining companies hunt for increasingly elusive projects which offer both robust grades and multi-million ounce potential, more and more of these companies are looking north – as in far north.

One of the companies cashing in on this new, northern gold-rush is Cache Exploration Inc. (TSX: V.CAY, OTCQB: CEXPF, Forum). CAY’s base of operations is Nunavut. The Company’s operational focus is the Kiyuk Lake Gold Project.

Kiyuk Lake is a huge land package, encompassing approximately 491 square kilometers. This is a true “district” play, as management was intent on locking up the majority of the entire Kiyuk Basin, a Proterozoic geological formation. Mineralization has already been identified along a 15 kilometer strike length.

Previous work on the property includes approximately 12,000 meters of drill results, compiled between 2008 and 2013. Those results have consistently yielded broad bands of gold mineralization, with solid grades, including numerous intercepts in excess of 3 g/t Au.

Some mining investors may be leery of mining projects situated this far to the north, concerned that the climate/geography may be a significant impediment to mining operations. What separates Cache Exploration (and Kiyuk Lake) from some of these northern projects is that Kiyuk Lake is amenable to year-round operations.

In terms of the geography, not only is the terrain relatively flat, but there is only a very thin layer of overburden before immediately hitting bedrock. This thin overburden at Kiyuk Lake significantly simplifies exploratory drilling now and mining down the road.

The Company didn’t simply stumble upon this highly prospective Project. CAY’s management team includes Robert Bick, Corporate Development who is intimately familiar with the Kiyuk Lake Project.

In fact, during the time Bick was CEO of Evolving Gold Corp. (2007-2010), he was instrumental in acquiring the Kiyuk Lake Project for Evolving Gold. Kiyuk Lake was subsequently spun out into Prosperity Goldfields. Tracing the history of the Project, gold mineralization was originally discovered in the area by prospectors in the early 1990’s. Initial drilling was conducted by Newmont Mining Corporation in 2008. However, with the precipitous (but temporary) drop in the price of gold in 2008, Newmont – and many other senior gold miners – simply walked away from many of their promising development-stage properties.

Prosperity Goldfields conducted the most recent drilling, which ended in 2013 with the downturn in the junior resource activity.

Enter Cache Exploration. In March, 2017 CAY announced a definitive agreement to acquire a 100% interest in the Project. More recently, on July 19th, Cache announced its summer drill program for Kiyuk Lake, commencing at the end of July.

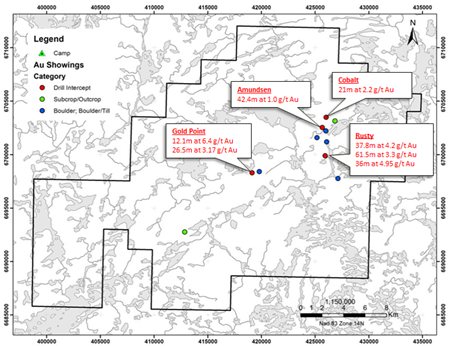

Kiyuk Lake doesn’t represent a single deposit. Instead, the Company has identified four, discrete mineralized zones. These “pods” of gold mineralization are open both laterally and at depth. The Rusty Zone has seen the most exploration work to date, and boasts many of the best intercepts.

(click to enlarge)

Highlights of previous drilling at Rusty include 3.3 g/t Au over 61.5 meters, 4.95 g/t Au over 36 meters, and 4.2 g/t Au over 37.8 meters. However, broad intercepts of gold mineralization have also been recorded at the Gold Point, Amundsen, and Cobalt Zones. The Rusty Zone will be the principal focus of the upcoming exploration program, with a secondary emphasis on Gold Point.

In addition to the four zones which have already been discovered, five new target areas have been identified. Meanwhile, many parts of the 15-kilometer trend remain untested by drilling. Previous airborne magnetic work indicates plenty of magnetic anomalies which could yield additional “pods” of gold.

For investors, apart from the quality of the project itself, it’s important to understand that Cache Exploration isn’t alone in seeking gold riches in Nunavut. Prominent gold mining companies are presently active in Nunavut, with additional projects springing up elsewhere in the Canadian Arctic.

(click to enlarge)

Meadowbank is a producing gold mine, pouring its first gold for owner/operator Agnico Eagle Mines Ltd in 2010. AEM has already approved a satellite deposit for development, in order to extend the life of the Meadowbank Mine.

Meliadine is also owned by Agnico Eagle, and is presently that company’s largest gold development project. Even further to the north, Auryn Resources Inc. is developing the Three Bluffs project, and has just commenced a new 25,000 meter drill program.

Situated much farther north than Kiyuk Lake, these other mines/projects present considerably more geographical and logistical challenges for their operators. Yet even with the current, anemic price for gold, these other mining companies remain fully committed to their Nunavut projects.

The presence of these other mining companies with their Arctic operations represents more than merely validation for the management team of CAY. As more of these projects are developed, this represents a steady, if gradual, increase in mining infrastructure. But it represents even more than that.

As noted earlier; in 2008 senior gold mining companies were backing away from project commitments – with respect to all but the largest gold deposits. A lot has changed in the decade since.

The refusal of senior gold mining companies to remain active on the exploration front is coming back to haunt these large-cap producers. These largest gold miners have mined 10’s of millions of ounces of gold over the past decade. The problem is that they have not been adding nearly enough new reserves/resources to replace what has been mined out.

Globally, overall gold reserves have declined for five consecutive years. But that number fails to capture the significance of this crisis in the sector. According to a report from AGF Investments, these five years of declining mine reserves have taken global gold reserves to a 30-year low.

Gold Miners Are Running Out of Metal: Five Charts Explaining Why

Even in August 1999, with the price of gold crashed to a low of $250/oz (USD), mine reserves were significantly higher than current levels. If these senior gold producers don’t each start adding millions of ounces to their own reserves – quickly – then these companies simply will not be “senior gold producers” much longer.

While senior gold mining companies were generally walking away from the Arctic in 2008, today they are taking a renewed interest, as reflected by the two, large Nunavut projects operated by senior producer, Agnico Eagle. As management targets a multi-million ounce gold resource at Kiyuk Lake, industry spectators will be watching very closely – in addition to CAY’s own shareholders.

This is the situation in the gold mining industry now, with the price of gold still mired near multi-year lows. This is a market with fundamentals which dictate much higher prices, but almost all mainstream commentary on the gold market is completely uninformed.

To start with, what the mainstream media (and even senior gold miners) call “the gold market” is a paper market – it’s not the gold market at all. This truth was laid bare back in 2010.

In a 2010 hearing before the Commodity Futures Trading Commission (CFTC), industry expert Jeffrey Christian of the CPM Group confessed that 99% of the “gold” traded in these markets is not gold at all, it is paper – paper-called-gold.

When supply and demand numbers are reported (by the World Gold Council) these numbers are not the supply and demand for gold, they are the supply/demand numbers for paper-called-gold.

The real gold market is a market with a perpetual supply deficit. It is a market with falling reserves, which are now at a crisis level. It is a market which now is also seeing falling production.

The only way to reverse falling production is with a significantly higher price for gold. The only way to reverse falling reserves is with a significantly higher price for gold. The only way to reverse this perpetual supply deficit is with a significantly higher price of gold.

These are only the mining fundamentals which support higher gold prices. The economic fundamentals are even more spectacular.

U.S. dollars have value only to the extent that they are strictly limited in supply. [emphasis mine]

-- Federal Reserve Chairman (then Governor), B.S. Bernanke, November 21, 2002

So said B.S. Bernanke back in 2002. Then this is what Bernanke did, starting in 2009: the Bernanke Helicopter Drop.

The Bernanke Helicopter Drop represents the most radical and reckless expansion of the supply of a major currency since the Weimar Republic – and Germany’s hyperinflation following World War I. The U.S. dollar is not “strictly limited in supply”. Instead, its supply is virtually completely unlimited.

According to the (former) Chairman of the Federal Reserve, U.S. dollars no longer have any value. What is the price of gold, denominated in a worthless currency (the U.S. dollar)? This is just simple arithmetic: $infinity/oz – not $1,250/oz.

Mining is a somewhat speculative industry in that operational success is rarely a guarantee. In contrast, the (physical) gold market is not speculative. This is a market with only one, possible long-term direction for prices: up.

A strongly rising price of gold (to levels well beyond previous highs) is not a question mark, it is a certainty. The permanent supply deficit, falling reserves, and falling production in the gold sector are all indicators of a commodity that is radically under-priced.

The gold market is a market waiting to take off. Gold mining in the Canadian Arctic is just beginning to take off. Cache Exploration is positioned to take advantage of both of these trends -- and so are its shareholders.

FULL DISCLOSURE: Cache Exploration is a paid client of Stockhouse Publishing.