Real estate mania is a pernicious form of greed. There are several reasons why this can be such a dangerous manifestation of “irrational exuberance”. At the top of the list is mainstream media cheerleading. As housing markets devolve into obvious asset bubbles, instead of the media providing accurate information (and words of warning), all that is typically seen is mindless cheerleading.

“Look how high prices have gone already!”

“Look how high this analyst is projecting that prices will go!”

Such cheerleading is totally irresponsible. Real estate bubbles are the easiest category of asset bubble to identify. Why? It’s because the fundamental equation of every real estate market is both simple and unequivocal.

Real estate prices must remain parallel to incomes.

This is not a theory. It’s not an assertion. It’s simple arithmetic.

What do homebuyers rely upon to make the mortgage payments on their real estate? Their incomes. As a proposition of elementary logic, if homebuyers use their incomes to make their mortgage payments, then higher house prices can only be supported (over the long term) by an equal rise in incomes.

At best, Canadian incomes have been flat, for many years. The modest rise in nominal income levels has been offset (at the least) by the relentless rise in long-term/permanent unemployment – unemployment that is hidden and ignored by the fraudulent “unemployment statistics” that are quoted by Western governments.

Canadian incomes are flat. Now look at housing prices in Toronto and Vancouver.

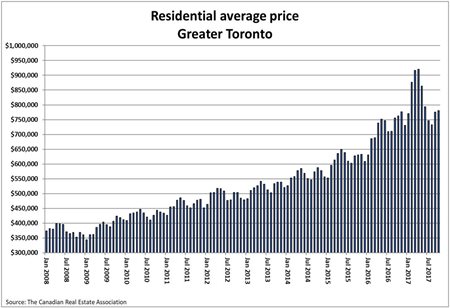

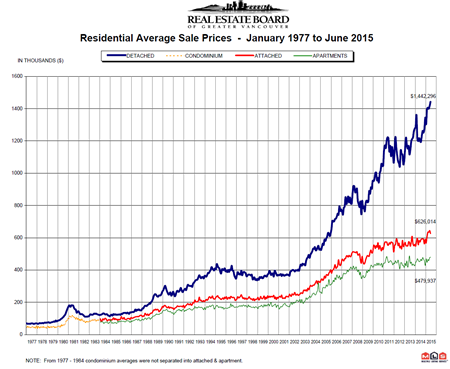

(click to enlarge above charts)

In 2008; average residential home prices in Toronto were well below $400,000. After briefly spiking above $900,000, Toronto’s bubble market has suddenly dipped below $800,000. As noted in previous articles on the Toronto housing bubble, this is only one of several extremely ominous signs that the Toronto bubble has popped.

Where are Toronto housing prices headed in the future? Back to $400,000? Think lower, much lower. Look at the Vancouver chart. Vancouver house prices (as with much of Canada) have been in a long-term uptrend that goes back to the 1980’s. However, throughout most of the 1990’s, Vancouver home prices were relatively stable. Let’s peg that as our equilibrium point.

During the 1990’s, Vancouver house prices gravitated around $400,000. Then the Big Bubble began. Since 2000; average residential prices have exploded to $1.44 million. That’s a 360% increase – while incomes have remained flat.

Where are Vancouver prices heading? Back to $400,000. But that’s only assuming that the anemic conditions in the Canadian labour market don’t continue to degenerate. If long-term/permanent unemployment continues to soar, that means less and less taxpayers.

The less people paying taxes, the more taxes that must be paid by each of us as individuals. With Canadian taxes (in all forms) rising much faster than incomes, this means that net incomes are actually falling – and that means that supporting house prices even at the $400,000-level (in Vancouver) becomes dubious.

Going from $1.44 million to $400,000 (or less) represents a real estate crash in the order of 70%. Of course, as we have already seen with the upside of this bubble, markets typically overshoot dramatically in both directions. The final peak-to-trough collapse of the Vancouver housing market will almost certainly represent an implosion well in excess of 70%.

Toronto homebuyers can expect roughly equal carnage in their own bubble market. But wait, shout the real estate promoters and housing-bubble enthusiasts. What about “the Asian buyers”? For a decade, when media shills refused to denounce the Vancouver and Toronto housing markets as bubbles, their excuse has always been the infamous (yet invisible) “Asian buyers”.

Unquestionably, this is a demographic that does exist. But does it justify current house prices in Toronto and Vancouver? Can it support these bubble prices over the longer term? No, to both questions.

There are several reasons why Asian buyers must be regarded as a temporary prop for these bubble markets, not long-term support.

- Momentum chasing

- Loss of purchasing power (and credit)

- Greener pastures

Many of the Asian homebuyers in Toronto and/or Vancouver are momentum-chasers: buyers who have piled into these markets who were attracted mostly (or completely) by soaring valuations. For any readers who question the size/importance of this component of Asian demand, just look to the leading equity markets in Asia: the Hang Seng and Nikkei.

These markets have seen more spectacular rises (and falls) than Western markets, fueled by momentum-chasing Asian investors. When the bottom falls out of these Canadian housing bubbles, “Asian buyers” will be leading the stampede – out.

Equally, when Canada’s housing bubbles collapse this will almost certainly be accompanied by crashes of all the other urban housing bubbles across the Western world, and very possibly a broader crash across all markets. Western housing bubbles have been fueled entirely by the lowest interest rates in history – frozen at this reckless level now for nearly a decade.

There is only one direction in which interest rates can move, and any significant rise in Western interest rates will be the financial equivalent of detonating a nuclear bomb in these bubble markets. Trillions of dollars in phantom “home equity” will evaporate – over a period of months, if not weeks.

No one will want to buy Western real estate (in the midst of a historically unprecedented collapse). Few will be able to afford to buy land.

Finally, those that do still retain purchasing power during this real estate collapse will almost certainly see greener pastures for their investment dollars. Why try to catch History’s most-dangerous “falling knife”? Much better to put that capital into an emerging sector – with obvious upside potential.

One last myth in Canadian real estate mythology needs to be dispelled: that current (ridiculous) house prices can be supported over the longer term because there is “a shortage of available real estate”. In a Globe & Mail article, Dr. John Rose dispels this myth.

An academic based in B.C., Rose is blunt. Vancouver doesn’t have a housing “shortage”. It has a surplus – a large surplus. Again, this is just simple arithmetic. Going back to 2001; for every new household formed in the Metro Vancouver region since that time, 1.19 new housing units have come onto the market – an average surplus of nearly 20% per year.

A previous Stockhouse article on the Toronto housing bubble reported similar numbers there. Those taking a superficial look at these bubble markets may perceive a “shortage”, but this is totally due to the large numbers of units being purchased by pure speculators.

Speculators are the first to bail out when any housing bubble pops. When the speculators are gone, Vancouver and Toronto will see the largest housing gluts in the history of either one of these cities.

The bigger they are, the harder they fall.

Nowhere is this old cliché more applicable than with respect to Canada’s urban housing bubbles.