The Stockhouse audience is now familiar with junior copper producer Amerigo Resources Ltd. (TSX: ARG, OTCQB: ARREF, Forum). It’s a good-news story: rising production, safe production, located in the world’s copper-producing capital (Chile), with declining costs.

The Stockhouse audience is now familiar with junior copper producer Amerigo Resources Ltd. (TSX: ARG, OTCQB: ARREF, Forum). It’s a good-news story: rising production, safe production, located in the world’s copper-producing capital (Chile), with declining costs.

Sound too good to be true? It gets better.

On November 16, 2017; Stockhouse investors were introduced to ARG in a full-length feature article. That piece laid out the unique business model of this copper-producing company. Amerigo Resources produces copper via a tailings operation. Sounds boring.

Amerigo Resources operates one of the world’s most-sophisticated tailings operations. Better. Amerigo Resources operates a large copper-tailings operation, strategically located amidst many of the world’s largest copper-producing mines, with a high-efficiency operation that can remain in production for many years to come. Much better.

This explains why ARG is considered a “safe” copper producer. The Company does not incur the primary risks of operating a copper mine. It processes the accumulated waste product from the production of these huge mines, with vast stockpiles already in existence. Investors wanting more details on the interesting history and logistics for this copper-producer should refer to the previous full-length feature.

Amerigo knows it has a secure, reliable source of copper-mineralized input for production. From an operational standpoint, the only potential variable is the processing of these tailings. This “variable” is also the path to increasing profits for the Company and a greater rate of return for investors.

Without the need to devote considerable time and energy to ore-extraction operations (i.e. actual mining), this allows management to devote all their energies to optimizing processing. This is where both rising production and declining costs enter the picture.

The Company is currently nearing completion of its Cauquenes Phase Two expansion. This project consists of additional process plant equipment to enable the Company to maximise recovery of copper from the high grade historic Cauquenes tailings deposit.

On May 9, 2017; ARG released its Q1 2018 financial results. The Company reported cash costs of $1.77/lb, on total quarterly production of 14.2 million pounds of copper. Management also reported that the Phase Two expansion is on-budget and on schedule, due to come fully online in the fourth quarter of this year.

When Cauquenes Phase Two is factored into operations, copper output is projected to rise to 85 – 90 million pounds per year (21.25 – 22.50 million pounds per quarter). Cash costs are projected to decline to a range of $1.45 to $1.60/lb.

This equates to roughly 50% more output than Q1 2018, with cash costs declining by as much as 18%. What’s missing from this equation? A higher share price.

(click to enlarge)

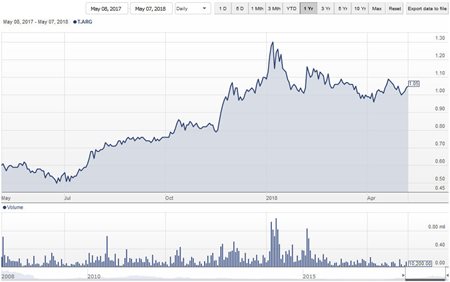

Despite this imminent jump in production, with improving margins, the Company’s share price has flattened out. True, the price of copper has also flattened out over the past several weeks. However, the real story in the copper market is revealed by a long-term chart of inventories.

[chart appears courtesy of InfoMine.com]

Copper inventories are at roughly half the levels of five years ago and roughly one-third of the levels from 15 years ago. Copper is one of the essential building blocks of the global economy. In historical terms, copper inventories are low. Very clearly, the only long-term direction for the price of copper is higher.

This seems to make Amerigo Resources a no-brainer for mining investors. Can the market rely upon the Company to deliver the projected improvements in production and costs? In a word, yes.

Investors have seen this movie before, it’s called “Cauquenes Phase One”. ARG has already delivered on one of its expansion plans. This took production from a previous level of 25 million pounds per year up to the current level, with full-year production guidance of 60 – 65 million pounds of copper. A longer 3-year chart shows how long-term ARG investors have been handsomely rewarded for their investment.

(click to enlarge)

Amerigo Resources offers investors reliable and increasing copper production. It will deliver this increased production at improved margins, in a copper market where prices must rise over the long term (to rebuild inventories back to normal levels). Over the short term, ARG’s President and CEO, Rob Henderson, puts the Company’s latest results into context.

MVC’s robust production results together with stronger metal prices have improved our financial position and our focus is to safely complete our expansion to 85 – 90 million pounds of copper per year on budget in Q4-2018.

The Big Picture is that this is a Company that has already delivered one substantial production increase (that rewarded investors), and it is on-budget and on schedule for Cauquenes Phase Two.

Easy money.

www.amerigoresources.com

FULL DISCLOSURE: Amerigo Resources Ltd. is a paid client of Stockhouse Publishing.