While mining investors wait for bull market sentiment (and valuations) to return to the mining sector, they still want to make money. It’s not as easy as when metals markets are flying high, but it can be done.

While mining investors wait for bull market sentiment (and valuations) to return to the mining sector, they still want to make money. It’s not as easy as when metals markets are flying high, but it can be done.

It requires being selective. Looking for the best projects, in mining-friendly jurisdictions, with solid management. One gold mining company that meets these criteria – and is generating strong returns for investors – is Gran Colombia Gold Corp. (TSX: GCM, OTCQB: TPRFF, Forum).

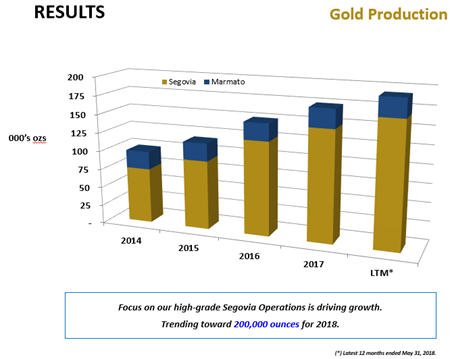

This TSX-listed mid-tier gold miner is nearing a major plateau: 200,000 oz’s per year of gold production (along with silver credits), with large high-grade resources that are certain to whet the appetite. The center of operations is the Company’s flagship Segovia Mine in Colombia: the largest underground gold/silver mining operation in this rising gold jurisdiction.

It’s easy for investors to wrap their heads around this story because it’s all in the numbers. It starts with the chart for GCM:

(click to enlarge)

While most of the gold mining industry has struggled over the past year, Gran Colombia has roughly doubled its share price over this period. That’s despite a recent pullback caused by a drop in the price of gold.

How has the Company generated this impressive return? More numbers. It starts with rising production…

(click to enlarge)

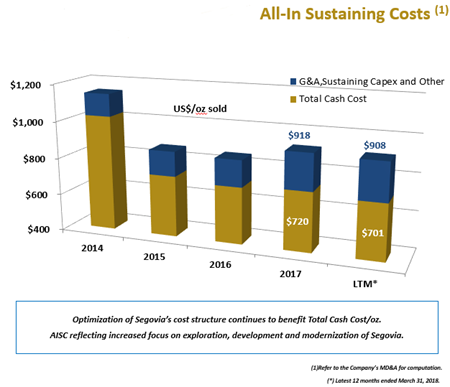

…then add in declining cash costs.

(click to enlarge)

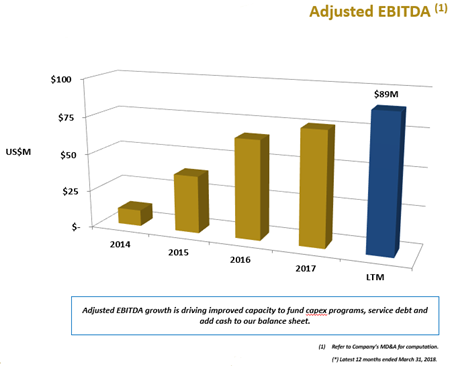

Put those two things together and you get stronger margins, rising cash flow, and more profit.

(click to enlarge)

In a conference call with Stockhouse Editorial, CEO Lombardo Paredes provided some details on how the Company has produced this strong operational profile. Calculated over the 12-month period ending March 31, 2018, GCM has recorded total EBITDA of US$89 million.

Focusing on what we can control has been the cornerstone of the turnaround we have successfully completed in our operations and financial results since I started with the Company in early 2014. Initially, our efforts were centered on improving our cost structure at Segovia. Then we turned our attention to optimizing our mine plans at Segovia.

Our initial emphasis was the Providencia Mine, which has been paying great dividends to us over the past year and has been a key catalyst for our production and EBITDA growth. Similarly, we have been investing in the modernization of our El Silencio Mine which contributes about half of our gold production at Segovia, and this year we are commencing the development of new areas in our Sandra K Mine to bring on stream to add to our production profile.

Simultaneously, we have invested in our processing plant and laboratory to modernize our facilities at Segovia while adding a new long-term tailings storage facility and water treatment plant to manage our environmental responsibilities. Exploration programs in 2016 and 2017 have led not only to increased mineral resource estimates but also to our first ever proven and probable reserve at Segovia reported earlier this year. With our focus on execution, we are firing on all cylinders.

It’s been several successive years of rising production and declining costs for Gran Colombia, but it’s only in the last year that the market has started to reward the Company (and its shareholders) for this steady improvement.

Why? One word: self-sufficiency.

This is a mid-tier gold mining operation that has turned the corner. Even with the current weak price for gold, GCM has the cash flow needed to fund day-to-day operations, conduct the exploration necessary to ensure efficient production and mine planning, and continue to add to the Company’s impressive high-grade resource base.

Running a modern mining operation is not a simple task. There are bureaucracies to deal with, contracts to be negotiated, international markets to navigate.

Still, even in comparison to running a mine, starting up a new mining operation can be a major challenge. Mining companies plan very carefully when commissioning a new mine. But famed poet Robert Burns had a retort for such planning.

“The best laid schemes o' mice an' men / Gang aft a-gley.”

For Stockhouse readers who are not conversant with Old English, a more modern rendering translates into: the best laid plans of mice and men often go awry.

Even for experienced management teams, there can be growing pains with a new mine. Despite the spectacular grades of its gold resources, the Segovia Mine experienced growing pains.

Operating costs were too high. The decline in the price of gold in 2013 eroded margins further. Consequently, Gran Colombia ran into debt problems. With the bottom line not as strong as projections, the market reacted in an expected manner: punishing GCM’s share price.

The response of management to this state of affairs was simple, they rolled up their sleeves and went to work. First on the agenda was mine optimization: reduce cash costs, streamlining production to increase throughput and boost operating margins. As the graphics above indicate, the Company has been very successful in improving the cash flow and profitability of its Segovia Operations.

What makes this optimization all the more impressive is that Segovia is not a single mine, but rather a mining complex that is currently producing gold from three separate locations on the Segovia property.

Then there is the Marmato Project. The Segovia Mine Complex is a robust mid-tier gold mining operation by itself, with an abundant resource base and very high grades. Grades at Marmato are not quite as high (~ 2.5 g/t to 5 g/t Au) as with the Segovia resources, but Marmato is a monster.

The Spanish originally began mining gold from this site nearly 500 years ago. Indeed, the Marmato Mine was considered to be such a lucrative asset that it was used as collateral with British banks during Colombia’s war of independence against Spain. Over a span of five centuries, gold mining at Marmato has continued almost continuously.

For mining investors who are suspecting that this property has been mined out, guess again. Marmato has a current resource of nearly 4 million ounces of gold (Measured & Indicated) along with over 4 million ounces as an Inferred resource. In addition, these resources contain roughly 38 million ounces of silver.

The land package was consolidated by the previous operator (Medoro Resources) during 2009 and 2010. In 2011, Gran Colombia merged with Medoro to become the leading gold mining company in Colombia. The property benefits from abundant infrastructure, with access directly off of the Pan American Highway.

Longer term, the Company sees Marmato as a separate underground mine. With operations at Segovia now firing on all cylinders, producing a long-term development strategy for Marmato is high on management’s agenda.

That’s the operational picture for Gran Colombia. However, if investors really want to understand this strong turn-around story, they also need to take a close look at the Company’s finances.

GCM’s previous large debt-load was more than just a financial millstone around the neck of the Company and its shareholders. It was creating a large overhang of dilution. What was needed was a full restructuring.

With the operational parameters all tracking better, management turned their attention to finance. Gran Colombia cleaned up its balance sheet, lowering the Company’s debt level while also reducing the impact of dilution in financing this debt.

Here GCM looked even higher up its corporate ladder in devising a plan of action to address Gran Colombia’s debt burden and capital structure. Executive Co-Chairman Serafino Iacono led the way. A veteran in capital markets, Iacono has played an instrumental role in raising billions for natural resource projects around the world.

(click to enlarge)

Iacono strengthened GCM’s balance sheet, and he did so in an innovative manner – effectively selling a new debt product as a means of minimizing future dilution while Gran Colombia paid down its debt. What was this “new product”? Gold-backed notes.

The low current price of gold is a concern to gold mining companies and gold investors, but it also represents opportunity: the chance to cash in when the price of gold corrects higher to a more rational level. Knowledgeable gold investors understand this reality. Consequently, there was no shortage of takers for Gran Colombia’s gold-backed notes to refinance its debt. Co-Chairman Iacono went into further detail on this successful restructuring.

We offered a very attractive piece of paper to the market and the market overwhelmingly responded. We raised US$98 million which allowed us take out our senior secured debentures, reducing potential dilution in the process, and putting in place a new 6-year note that allows us to use less than 10% of Segovia’s expected gold production to repay the debt while providing investors in the notes with an 8 ¼% coupon and upside in their return if gold is above US$1,250 per ounce.

We added about US$14 million to our cash position through this financing and the units we sold also included some warrants, an additional source of future capital for our balance sheet. Our operational improvement combined with our improved balance sheet puts us in a very nice position to explore and expand our assets at Segovia and Marmato.

Growing pains. It’s common for people to experience them. It’s common for new mines to experience growing pains too. Gran Colombia Gold experienced these growing pains with its Segovia Gold Mine and now these issues are all disappearing in the rearview mirror.

For new investors, however, the bottom line is opportunity. Gold mining investors can buy into this mid-tier producer as it nears 200,000 ounces per year of gold production. With vast resources and high-grade mineralization, the Company’s current $89 million market cap represents a bargain-basement valuation.

From an operations standpoint, Gran Colombia Gold is just hitting its stride and the market is just beginning to notice. This means for GCM’s share price the best is yet to come. It’s all in the numbers.

www.grancolombiagold.com

FULL DISCLOSURE: Gran Colombia Gold Corp. is a paid client of Stockhouse Publishing.