TPG Specialty Lending, Inc. Sends Letter to TICC Capital Corp. Chairman of the Board Highlighting Board’s Self-Serving

Actions and Lack of Alignment with Stockholders

TICC Board Prioritizes Own Interests Over Those of Stockholders by Collecting Oversized Fees, Defending a Failing External

Adviser, Delivering Poor Financial Results and Refusing to Engage with Largest Single Stockholder

TSLX Remains Committed to Effecting Change and Advocates for a More Sustainable Dividend Policy to Provide Greater Value to

Stockholders

TSLX Encourages TICC Stockholders to Vote the GOLD Proxy Card to Terminate TICC’s External Adviser’s Contract and

Elect T. Kelley Millet to the TICC Board

TPG Specialty Lending, Inc. (“TSLX”; NYSE:TSLX), a specialty finance company focused on lending to middle-market companies,

today issued a letter to TICC Capital Corp.’s (“TICC”; NASDAQ:TICC) Chairman of the Board, Mr. Steven Novak, calling out the

self-serving actions of the Board and its lack of alignment with stockholders’ best interests. In the letter, TSLX outlines how the

Board has failed TICC stockholders and how stockholders would benefit from a new, best-in-class external adviser.

This Smart News Release features multimedia. View the full release here: http://www.businesswire.com/news/home/20160802006086/en/

(Graphic: Business Wire)

A copy of the letter follows:

Mr. Steven Novak

Chairman of the Board

TICC Capital Corp.

8 Sound Shore Drive, Suite 255

Greenwich, CT 06830

Dear Mr. Novak,

We are writing as the largest single stockholder of TICC Capital Corp (“TICC” or the “Company) in response to your latest public

letter of July 28, 2016, in which we believe that, once again, you are blatantly misleading stockholders. We think it’s time to

finally set the record straight and end the fear tactics you continue to wield against your

stockholders.

We simply reject that you are a true representative of stockholder interests. We note that your purchase of 5,000 shares in May

2016, following our public letters, for an investment of $26,401, was the first time you acquired shares in almost eight years.

Only under threat of proxy contest did you hold your nose and break a near decade of avoiding the very stockholders you now purport

to represent.

TPG Specialty Lending (“TSLX”) has never once indicated that we encourage or support the reduction of TICC’s dividend. In fact,

we have advocated for a more sustainable dividend policy, one that would provide stockholders with greater value and a true return.

We believe the clearest path forward is to replace the current management team with one that can source and manage assets that earn

a return to meet its dividend.

Your leadership has overseen investment returns for stockholders that are so poor it is almost incomprehensible. However, you

and the TICC Board have clung to the life raft of false promises about the future of a clearly unsustainable dividend.

The fact is that your Board has shown a shocking misunderstanding of investment fundamentals mixed with a craven focus on

personal interests. You have delivered abysmal total returns, halved the core of your stockholders’ investment (net asset value)

and are now paying a dividend independent analysts almost universally call unsustainable. 1

How can you claim this disguised liquidation is a sustainable or fair way to deliver value to

stockholders?

The stockholders of TICC deserve directors that will put them first, and an external adviser that will create true value. Last

fall, you delivered a “teach-in” session for stockholders on your phony dividend. Let us return the favor on the basics of

investing.

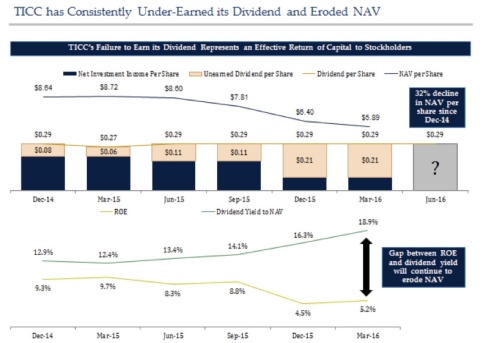

The facts are clear: in the first quarter of 2016, TICC management generated net investment income (“NII”) equivalent to 5% of

net asset value (“NAV”), but TICC has paid out a dividend equal to 20% of NAV.

Your materials have consistently ignored the underlying nature of the assets TICC owns, which are primarily broadly syndicated

securities. This creates a distortion when comparing TICC to BDCs that instead focus on bespoke, directly originated investments.

For example, even though we expect to see an increase in the fair value of the broadly syndicated and readily accessible assets

held in TICC’s portfolio during the quarter, this has no influence on the future earning power of TICC. The fact is the existing

portfolio of assets does not generate sufficient income to support the current dividend policy. We are confident that you will

attempt to use any fictional gain to further confuse stockholders with arcane and misleading references to accounting rules.

We are equally confident that stockholders will continue to recognize the simple facts. NAV is directly impacted by TICC’s

ability to earn its dividend – something TICC has yet to prove it is capable of doing in a sustainable manner.

We regret to state that we have lost all confidence in the Board and the management team’s ability to either protect our

investment or generate significant future returns. In our eyes, you are no longer a credible adviser and we believe other

stockholders feel similarly.

Your reputation and the reputations of the other directors at TICC are on the line in this fight. It is clear that you and other

“independent” board members are more than willing to throw that away to desperately protect a failing adviser given the Company has paid the Board in excess of $2.8 million in fees while stockholder returns have been less than

treasuries2.

Let us remind you of the indefensible actions the Board and management team have taken, all at the expense of their

stockholders:

- Collection of Oversized Fees

The external adviser has collected over $141.4 million in management and incentive fees from stockholders’ investment over the

past 12+ years. Mr. Novak, you personally collected more than $1 million in Board-related compensation, all while NAV decreased

by 57% since TICC’s IPO in 2003. The Board and management team continue to benefit from stockholders’ investment while TICC has

delivered abysmal returns, underperforming the BDC Composite by 192% since 20033. How can you

defend lining your own pockets like this while stockholders’ investments suffer?

- Defense of the Failing External Adviser

For the first time in its history, TICC’s annual meeting was not held in June. As a result of this delay, management insiders

have been permitted to accumulate TICC shares at record low prices, which they presumably will vote in their own self-interest.

How can you and the rest of the Board justify this? How can you defend an external adviser that has ignored the lack of earning

power of TICC’s portfolio and subsequently delivered such terrible returns for stockholders? You cannot.

- Likely Violation of Federal Securities Laws

It is nearly impossible for us to trust that the Board and management team can act independently following their role in the

flawed and failed transaction in 2015 that led a federal judge to find TICC to have misled stockholders and to have likely

violated federal securities laws.

- Facilitation of a Value Transfer from Stockholders to the Board

Mr. Novak, in the failed 2015 transaction, you and TICC led a campaign to sell the external adviser to a third party and

advocated the reduction of management fees, authorization of a share buyback program, and reconstitution of the Board. Although

in that solicitation, the Special Committee of the Board indicated it believed “[n]o alternative currently exists that the

Special Committee would approve or recommend because no current proposal is preferable to the status quo other than the approval

of BSP as the new manager,” we do not believe that to be the case and we note that, as part of its advocacy in favor of that

solicitation, the Company told Stockholders that failing to approve the BSP transaction would result in Stockholders being left

with the “[s]tatus quo: higher fee structure . . . [the] same advisor, and [the] same Board.” What has changed? To us, the

difference is clear. You will only support change that results in millions of dollars being paid to fellow

Board members.

- Refusal to Engage with Largest Single Stockholder

In February of 2016, TSLX made it clear that we wished to avoid a costly and drawn-out proxy contest and encouraged a productive

meeting with TICC to evaluate the Company’s options for a brighter future. However, TICC refused to engage with us in any

meaningful way and instead left TSLX with no choice but to pursue a campaign at the annual meeting to effect real change. TICC’s

unwillingness to consider terminating the external adviser to avoid a burdensome proxy contest again demonstrates its lack of

interest in doing what’s best for stockholders. If you won’t listen to us, your largest single stockholder,

what makes us believe you would listen to the rest of your stockholder base?

Your lack of leadership has led to terrible financial performance and an astounding decline in NAV of 57% since 2003. In our

eyes, you are unfit to manage stockholders’ investment given past performance. You have destroyed substantial value at the expense

of stockholders and you continue to misrepresent what a change in the external adviser could mean for stockholders. Stop lying to your stockholders! There is a promising future for TICC under new management.

TICC stockholders deserve more. TSLX intends to continue advocating for TICC stockholders’ best interests, including the pursuit

of the following reforms:

- The implementation of a sustainable dividend policy

- Greater total returns for stockholders, rather than the adviser

- The authorization of a meaningful share repurchase program

- The election of new independent directors

- No restrictions on value-creating opportunities

- The appointment of a new best-in-class external adviser that prioritizes stockholders’ best interests

and their investment

Stockholders deserve both a refreshed and independent Board and a capable management team and external adviser to drive growth,

generate value and deliver true meaningful change. The time for a new path forward is now.

Very truly yours,

TPG SPECIALTY LENDING, INC.

Joshua Easterly

Chairman and Co-Chief Executive Officer

Michael Fishman

Co-Chief Executive Officer

TSLX’s proxy materials are also available through the SEC’s website and at www.changeTICCnow.com.

About TPG Specialty Lending

TPG Specialty Lending, Inc. (“TSLX” or the “Company”) is a specialty finance company focused on lending to middle-market companies.

The Company seeks to generate current income primarily in U.S.-domiciled middle-market companies through direct originations of

senior secured loans and, to a lesser extent, originations of mezzanine loans and investments in corporate bonds and equity

securities. The Company has elected to be regulated as a business development company, or BDC, under the Investment Company Act of

1940 and the rules and regulations promulgated thereunder. TSLX is externally managed by TSL Advisers, LLC, a Securities and

Exchange Commission registered investment adviser. TSLX leverages the deep investment, sector, and operating resources of TPG

Special Situations Partners, the dedicated special situations and credit platform of TPG, with approximately $16 billion of assets

under management as of March 31, 2016, and the broader TPG platform, a global private investment firm with approximately $74

billion of assets under management as of March 31, 2016. For more information, visit the Company’s website at www.tpgspecialtylending.com.

Forward-Looking Statements

Information set forth herein may contain forward-looking statements, including, but not limited to, statements with regard to

the expected future financial position, results of operations, cash flows, dividends, portfolio, financing plans, business

strategy, budgets, capital expenditures, competitive positions, growth opportunities, plans and objectives of management of TICC

Capital Corp. (“TICC”), statements with regard to the expected future financial position, results of operations, cash flows,

dividends, portfolio, financing plans, business strategy, budgets, capital expenditures, competitive positions, growth

opportunities, plans and objectives of management of TPG Specialty Lending, Inc. (“TSLX”), and statements with regard to TSLX’s

proposed business combination transaction with TICC (including any financing required in connection with a possible transaction and

the benefits, results, effects and timing of a possible transaction). Statements set forth herein concerning the business outlook

or future economic performance, anticipated profitability, revenues, expenses, dividends or other financial items, and product or

services line growth of TSLX, TICC and/or the combined businesses of TSLX and TICC, including, but not limited to, statements

containing words such as “anticipate,” “approximate,” “believe,” “plan,” “estimate,” “expect,” “project,”

“could,” “would,” “should,” “will,” “intend,” “may,” “potential,” “upside” and other similar

expressions, together with other statements that are not historical facts, are forward-looking statements that are estimates

reflecting the best judgment of TSLX based upon currently available information.

Such forward-looking statements are inherently uncertain, and stockholders and other potential investors must recognize that

actual results may differ materially from TSLX’s expectations as a result of a variety of factors including, without limitation,

those discussed below. Such forward-looking statements are based upon TSLX’s current expectations and include known and unknown

risks, uncertainties and other factors, many of which TSLX is unable to predict or control, that may cause TSLX’s plans with

respect to TICC or the actual results or performance of TICC, TSLX or TICC and TSLX on a combined basis to differ materially from

any plans, future results or performance expressed or implied by such forward-looking statements. These statements involve risks,

uncertainties and other factors discussed below and detailed from time to time in TSLX’s filings with the Securities and Exchange

Commission (“SEC”).

Risks and uncertainties related to a possible transaction include, among others, uncertainty as to whether TSLX will further

pursue, enter into or consummate a transaction on the terms set forth in its proposal or on other terms, uncertainty as to whether

TICC’s board of directors will engage in good faith, substantive discussions or negotiations with TSLX concerning its proposal or

any other possible transaction, potential adverse reactions or changes to business relationships resulting from the announcement or

completion of a transaction, uncertainties as to the timing of a transaction, adverse effects on TSLX’s stock price resulting from

the announcement or consummation of a transaction or any failure to complete a transaction, competitive responses to the

announcement or consummation of a transaction, the risk that regulatory or other approvals and any financing required in connection

with the consummation of a transaction are not obtained or are obtained subject to terms and conditions that are not anticipated,

costs and difficulties related to a potential integration of TICC’s businesses and operations with TSLX’s businesses and

operations, the inability to obtain, or delays in obtaining, cost savings and synergies from a transaction, unexpected costs,

liabilities, charges or expenses resulting from a transaction, litigation relating to a transaction, the inability to retain key

personnel, and any changes in general economic and/or industry specific conditions.

In addition to these factors, other factors that may affect TSLX’s plans, results or stock price are set forth in TSLX’s Annual

Report on Form 10-K and in its reports on Forms 10-Q and 8-K.

Many of these factors are beyond TSLX’s control. TSLX cautions investors that any forward-looking statements made by TSLX are

not guarantees of future performance. TSLX disclaims any obligation to update any such factors or to announce publicly the results

of any revisions to any of the forward-looking statements to reflect future events or developments.

Third Party-Sourced Statements and Information

Certain statements and information included herein have been sourced from third parties. TSLX does not make any representations

regarding the accuracy, completeness or timeliness of such third party statements or information. Except as expressly set forth

herein, permission to cite such statements or information has neither been sought nor obtained from such third parties. Any such

statements or information should not be viewed as an indication of support from such third parties for the views expressed herein.

All information in this communication regarding TICC, including its businesses, operations and financial results, was obtained from

public sources. While TSLX has no knowledge that any such information is inaccurate or incomplete, TSLX has not verified any of

that information. TSLX reserves the right to change any of its opinions expressed herein at any time as it deems appropriate. TSLX

disclaims any obligation to update the data, information or opinions contained herein.

Proxy Solicitation Information

In connection with TSLX’s solicitation of proxies for the 2016 annual meeting of TICC stockholders in favor of (a) the election

of TSLX’s nominee to serve as a director of TICC and (b) TSLX’s proposal to terminate the Investment Advisory Agreement, dated as

of July 1, 2011, by and between TICC and TICC Management, LLC, as contemplated by Section 15(a) of the Investment Company Act of

1940, as amended, TSLX filed an amended definitive proxy statement in connection therewith on Schedule 14A with the SEC on July 14,

2016 (the “TSLX Proxy Statement”). TSLX has mailed the TSLX Proxy Statement and accompanying GOLD proxy card to stockholders

of TICC. This communication is not a substitute for the TSLX Proxy Statement.

TSLX STRONGLY ADVISES ALL STOCKHOLDERS OF TICC TO READ THE TSLX PROXY STATEMENT AND THE OTHER PROXY MATERIALS AS THEY BECOME

AVAILABLE BECAUSE THEY CONTAIN IMPORTANT INFORMATION. SUCH TSLX PROXY MATERIALS ARE AND WILL BECOME AVAILABLE AT NO CHARGE ON THE

SEC’S WEB SITE AT HTTP://WWW.SEC.GOV AND ON TSLX’S WEBSITE AT HTTP://WWW.TPGSPECIALTYLENDING.COM. IN ADDITION, TSLX WILL PROVIDE COPIES OF THE TSLX PROXY STATEMENT WITHOUT

CHARGE UPON REQUEST. REQUESTS FOR COPIES SHOULD BE DIRECTED TO TSLX’S PROXY SOLICITOR AT TPG@MACKENZIEPARTNERS.COM.

The participants in the solicitation are TSLX and T. Kelley Millet, and certain of TSLX’s directors and executive officers may

also be deemed to be participants in the solicitation. As of the date hereof, TSLX beneficially owned 1,633,719 shares of common

stock of TICC. As of the date hereof, Mr. Millet did not directly or indirectly beneficially own any shares of common stock of

TICC.

Security holders may obtain information regarding the names, affiliations and interests of TSLX’s directors and executive

officers in TSLX’s Annual Report on Form 10-K for the year ended December 31, 2015, which was filed with the SEC on February 24,

2016, its proxy statement for the 2016 annual meeting of TSLX stockholders, which was filed with the SEC on April 8, 2016, and

certain of its Current Reports on Form 8-K. These documents can be obtained free of charge from the sources indicated above.

Additional information regarding the interests of these participants in the proxy solicitation and a description of their direct

and indirect interests, by security holdings or otherwise, is available in the TSLX Proxy Statement and other relevant materials to

be filed with the SEC (if and when available).

This document shall not constitute an offer to sell, buy or exchange or the solicitation of an offer to sell, buy or exchange

any securities, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale would be

unlawful prior to registration or qualification under the securities laws of any such jurisdiction. No offering of securities shall

be made except by means of a prospectus meeting the requirements of Section 10 of the Securities Act of 1933, as amended.

1 Results Miss on Professional Fee Expense – Maintain Neutral on Uncertain Outlook, Ladenburg Thalmann, May 10, 2015;

TICC: CORRECTION: Uncertainty Surrounding New Inv. Strategy, Wells Fargo, March 18, 2016 and TICC: We Hope TICC Mgmt Will Take

Questions On This Quarter's Conf. Call--Just Saying…, Wells Fargo, February 4, 2016; TICC at Crossroads, Barclays, October 6, 2015;

Board Making a Poor Deal? Should Shareholders Reject the Current Proposal?, Keefe, Bruyette& Woods, September 16, 2015; TICC

Report, Egan‐Jones Proxy Services, October 27, 2015

2 Company Filings. Capital IQ

3 BDC Composite comprised of ACAS, AINV, ARCC, BKCC, FSC, GBDC, HTGC, MAIN, MCC, NMFC, PNNT, PSEC, SLRC, TCAP, and

TCRD Note: Market data as of July 26, 2016

TPG Specialty Lending, Inc.

Investors:

Lucy Lu, 212-601-4753

llu@tpg.com

or

MacKenzie Partners, Inc.

Charlie Koons, 800-322-2885

tpg@mackenziepartners.com

or

Media:

Luke Barrett, 212-601-4752

lbarrett@tpg.com

or

Abernathy MacGregor

Tom Johnson, 212-371-5999

tbj@abmac.com

or

Pat Tucker, 212-371-5999

pct@abmac.com

View source version on businesswire.com: http://www.businesswire.com/news/home/20160802006086/en/