Like clockwork, big bank earnings keep rolling in better than expected. Goldman Sachs Group Inc

(NYSE: GS) and Citigroup

Inc (NYSE: C), both of which

reported early Wednesday, are the latest to beat Wall Street’s bottom-line estimates, though C came in a bit shy on the revenue

side of the equation.

Today is the last day of banks basking in the earnings spotlight. Inflation data and a speech later this afternoon by Fed Chair

Janet Yellen are the other key agenda items. Yellen is scheduled to speak on monetary policy and its tools in an address to

the Commonwealth Club in San Francisco at 3 p.m. EST. Meanwhile, overseas, Japan’s Nikkei Stock Average, which had tanked on

Tuesday in part due to a weaker dollar, posted moderate gains Wednesday as the dollar rebounded a bit.

Getting back to earnings: C came in at $1.14 per share, beating the average Wall Street analyst estimate by two cents. However,

C fell short of estimates on revenue. GS killed it on earnings, reporting $5.08 per share, vs. a $4.82 Wall Street estimate, and

also easily beat top-line estimates. Trading results looked awesome, and GS is the bank most influenced by trading. In its press

release, GS said bond-related trading soared 78% in Q4, and cited “an environment generally characterized by improved market

conditions, including rising interest rates and tighter credit spreads.”

Starting this afternoon, it’s on to other industries, with Netflix, Inc. (NASDAQ: NFLX) today, International Business Machines

Corp. (NYSE: IBM) tomorrow, and

General Electric Company (NYSE: GE) on Friday. There was widespread thought going into earnings that financials

would do well. Now how about the other areas of the economy?

Let’s start with NFLX, since it’s batting first. Last time out, NFLX surpassed analysts’ earnings expectations, so we’ll see if

that happens again. NFLX has a big international business, so it could be interesting to see how the stronger dollar affected that.

Wall Street consensus is for earnings per share of $0.13 cents, up from $0.10 cents a year earlier, according to Briefing.com.

Tomorrow, IBM will be the first major tech company to report. And GE’s earnings on Friday could serve as an indicator of how the

broader economy is performing, simply because GE has its proverbial hands in so many different types of products.

Currency continues to be a factor, with the British pound making its biggest one-day gains in eight years yesterday after

President-elect Trump said the dollar was looking too strong.

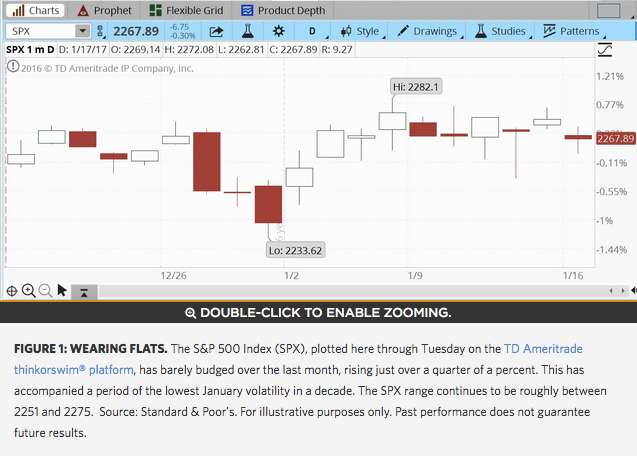

Volatility turned upward early Tuesday but then slipped back toward recent levels later in the day, according to the CBOE’s VIX.

With inauguration just two days away, some market participants are beginning to wonder when they’ll see more concrete proposals on

health care, taxes, fiscal stimulus, and infrastructure from the new administration, and those concerns may have fueled some of the

rise in volatility. However, VIX was back below 12 by early Wednesday.

Additionally, we saw some weakness in the Nasdaq yesterday, especially among semi-conductors, but Nasdaq has had an incredible

run and was slightly higher in pre-market trading.

The U.S. Consumer Price Index (CPI) for December rose 0.3%, in line with expectations, the government reported early

Wednesday.

More Housing Numbers Up Next

Thursday brings December housing starts, which are expected to rebound slightly following a rather weak November report. Wall

Street analysts expect improvement in the December number, to around 1.2 million from below 1.1 million in November, Briefing.com

said. The three-month average is around 1.16 million, which remains near one-decade highs. The November downturn was paced by a 45%

decline in multi-unit starts, yet it also featured a 4.1% decline in single-family starts to a seasonally adjusted annual rate of

828,000.

Fed Just Two Weeks Away, So Watch Volatility

Today’s CPI report puts the focus once again on inflation, which the Fed watches closely. The futures market continues to point

toward the Fed’s early February meeting being a quiet one, with just a 4% chance of a hike at that time, according to the

CME. The March meeting brings about a 21% chance, and that rises to 34% in May.

Health Care M&A Ahead?

Health care remains one of the best-performing S&P 500 sectors over the last month, and many analysts remain bullish about

prospects for the full year. There’s a sense that more M&A activity might occur, as many larger drug companies have cash on

hand. Tighter government rules on inversions, deals in which the acquiring company moves its headquarters overseas to save on

taxes, could make domestic drug companies look more inviting for big pharma.

© 2017 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.