Positive tidings continued from the retail sector Thursday with Walmart Inc. (NYSE: WMT) reporting solid results highlighted by a recharged performance from its

e-commerce business. Despite that, major stock indices ticked lower in pre-market futures trading as U.S. government bond yields

continued to march upward.

WMT earnings of $1.14 beat third-party consensus estimates by a penny, and sales of $122.7 billion topped estimates of $120.13

billion. Perhaps more importantly, e-commerce sales rose 33 percent in the quarter thanks in part to accelerating results in online

grocery shopping. That could help erase memories of less than stellar e-commerce growth the previous reporting period that helped

weigh on WMT shares. Though WMT remains lower for the year, its shares got a boost in pre-market trading after the earnings

release.

If you’re listening to WMT’s conference call, you might want to consider focusing on any potential conversation about the

company’s $16 billion deal that gives it a 77 percent stake in India’s Flipkart. The acquisition, announced earlier this week, is

WMT’s biggest ever, and Flipkart is a big player in India’s growing e-commerce market.

Arguably, the challenge for WMT’s executives is to convince the Street that this is the acquisition many investors hope it can

be, and the conference call might end up being as much about what Flipkart can do for WMT as it is about WMT’s actual earnings.

There’s a lot of apprehension around the deal, which is part of WMT’s strategy to expand its digital offerings and compete with

Amazon.com, Inc. (NASDAQ: AMZN).

The news wasn’t all good early Thursday. Results from J.C. Penney Company Inc. (NYSE: JCP) appeared to disappoint investors, who sent shares down more than 11 percent in

pre-market futures trading. The company said in a press release that its overall top-line sales came in below management’s

expectations, blaming cold April weather. We’re not done with retail yet. Nordstrom, Inc. (NYSE: JWN) reports after the close today.

As retail earnings flick across the screens each day, it’s important for investors—especially long-term investors who may be

looking for investment products that give them exposure to the retail sector—to understand that the dynamics are very different for

each company. It’s hard to think of an industry over the last 10 years that’s been more of an individual stock story, with so many

different things affecting different companies. The overriding factor is figuring out where are customers going to go, but what’s

going to get customers into the stores is a little bit different for each major name. Macy’s Inc. (NYSE: M), for instance, appears to be achieving a bit of success by setting

aside parts of some stores for discounts (see below).

Attention Turns to Bonds, Geopolitics

WMT’s solid results aside, the market braced for the possibility of more pressure Thursday from rising bond yields. Early in the

day, the benchmark 10-year yield rose above 3.1 percent to its highest level since mid-2011. That’s just one basis point above the

week’s high, but the psychological aspect of pushing above 3.1 percent could be spooking some investors. Higher yields can make

some stocks appear less attractive, particularly those that pay dividends or are loaded with debt. They also raise the cost of

borrowing.

Weekly jobless claims of 222,000 topped Wall Street analysts’ expectations for 215,000, so maybe that could cool off yields a

bit. We’ll have to wait and see.

With earnings season rapidly approaching the end of its long run on the Street, focus again could turn toward outside events. As

investors might remember, worries about geopolitics helped keep the action pretty turbulent heading into earnings season, and

volatility has smoothed out over the last few weeks with earnings in the spotlight. Still, news that North Korea had threatened to

abandon a meeting with President Trump appeared to have surprisingly little impact on the futures market when it popped up late

Tuesday, and volatility barely moved on the report.

Though the potential for geopolitical bumps and bruises remains a factor, perhaps many investors are starting to get wise to the

fact that these negotiations between countries can take a long time and that politicians often like to make big statements.

Since earnings season is so far along, it’s a good time to glance again at results to date. With 91.7 percent of S&P 500

companies reporting, 77 percent beat bottom line estimates while an impressive 75 percent beat sales estimates, according to

research firm CFRA. Meanwhile, average EPS growth of 23.1 percent is significantly better than the 16.3 percent that CFRA had

expected at the start of earnings season. Despite this, the S&P 500 Index (SPX) hasn’t really budged much over the last month

since earnings started. It’s up only about 1.5 percent in that period. The market isn’t really giving companies much credit for

their accomplishments. The earnings week continues tomorrow morning as Deere (DE) reports.

Financials Still Missing Parade

From a sector standpoint, most of the market moved higher Wednesday except for real estate and utilities. However, financials

weren’t able to get their engines really running despite the climbing interest rates that often help bank profits. Lack of

participation by the financials could be one reason the market isn’t able to really make a solid run toward the upside.

Maybe the problem is we’re focusing on large caps, not small-caps. Because on Wednesday, small-caps outperformed their bigger

brothers as the Russell 2000 (RUT) jumped more than 1 percent. Small-caps can be thought of as potentially providing a better

mirror of the U.S. economy than large- caps because a larger percentage of small-caps’ business tends to be domestic.

Also on the domestic front, the dollar index advanced slightly on Wednesday and is now back above 93 after slipping under 93

earlier in the week. Sometimes strength in the dollar can help keep crude oil under pressure, but that wasn’t the case Wednesday.

Instead, oil appeared to get a lift from the U.S. government reporting a weekly drop in oil and gasoline stockpiles. That might

have been a surprise to some investors after a private industry group on Tuesday reported rising supplies. This is normally the

time of year when stockpiles fall due to stronger demand from drivers, but overall stockpiles are much lower now than they were

last year at this time, and that could add to strength in the commodity.

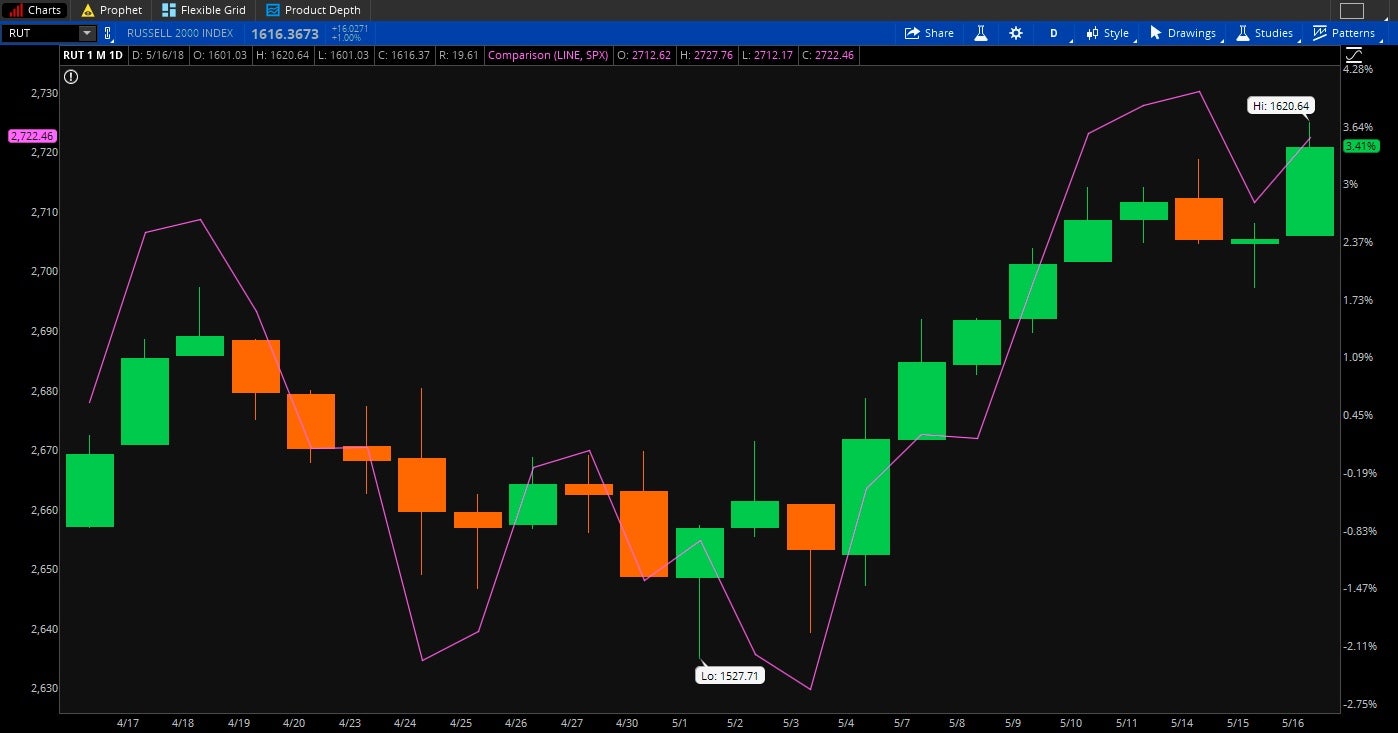

FIGURE 1: RUT N' ROLL. The small-cap Russell 2000 Index (RUT, candlestick) has been carving out big gains lately

and outpaced the S&P 500 (SPX) on Wednesday. One school of thought holds that the RUT is a somewhat better barometer of the

U.S. economy because small-cap stocks tend to have a larger percentage of their business at home. Chart source: FTSE Russell,

S&P Dow Jones Indices. The thinkorswim® platform from TD

Ameritrade. For illustrative purposes only. Past performance does not guarantee future results.

What’s at Stake

According to ancient legend, a stake through the heart can be useful to kill a vampire. Maybe some investors thought the recent

plunge in the Cboe’s VIX volatility indicator from above 20 for to around 13 might have put a metaphorical stake into VIX’s heart,

but action this week suggests VIX could have some life left in it. VIX scampered from around 13 up to nearly 15 on Tuesday amid

fears that rising bond yields might indicate inflation, but then quickly scurried back Wednesday to below 14 again. Arguably, this

indicates the possibility that some investors—many of whom were hurt last year by holding long positions in VIX—are prepared to

quickly bail at the slightest sign of a turndown in volatility. So maybe those stakes are raised and at the ready.

Pedal to the Metal on GDP?

It’s still nearly two weeks until the government issues its second estimate for Q1 gross domestic product (GDP) on May 30, but

that doesn’t mean it’s too early to start talking about potential Q2 GDP. If you recall, the government’s first crack at Q1 GDP

showed a somewhat disappointing 2.3 percent, down from levels of around 3 percent seen late last year. It’s unclear if the

government might raise that estimate May 30, but either way, it’s a look back. The Atlanta Fed’s GDP Now indicator looks ahead to

what GDP might end up being this quarter, and right now it’s projecting very solid 4.1 percent growth. There’s still a lot of data

between now and the end of Q2, but recent retail sales and industrial production figures both seemed to point toward strength in

the economy.

North Star Not Taking Backstage

Macy’s impressive earnings this week appears to be a sign that the company’s so-called “North Star” strategy announced last year

is having a positive impact on the struggling department store chain. One aspect of North Star was to emphasize M’s “Macy’s

Backstage,” a concept that offers more affordable items. It’s basically a discount area of the store, and it’s expanding to more

locations. Another aspect of the quarter was double-digit growth in digital earnings, something M highlighted in its earnings

release. All this said, one bright quarter isn’t necessarily the end of M’s challenges, and the company itself said in its press

release that it has “more work to do.” What’s unclear is whether M can find the right combination of brick-and-mortar to keep its

traditional customers while still appealing to those who want an online experience and might be tempted by electronic

competitors.

Information from TDA is not intended to be investment advice or construed as a recommendation or endorsement of any

particular investment or investment strategy, and is for illustrative purposes only. Be sure to understand all risks involved with

each strategy, including commission costs, before attempting to place any trade.

© 2018 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.