NEW YORK, Aug. 9, 2018 /PRNewswire/ --

Fellow Cigna Shareholders:

Our firm, Glenview Capital Management ("Glenview"), is a 10-year investor in Cigna (NYSE:CI), and we support the Express

Scripts (NASDAQ:ESRX) transaction for the following reasons:

1. Together, Cigna and Express Scripts will save their customers billions of incremental dollars annually with better

healthcare outcomes, consistent with the social mission of each entity.

- Cigna projects an incremental $253 per member of annual medical cost savings, the vast

majority of which will flow to customers and payors, for customers who use managed care and PBM services from the newly

combined Cigna / Express Scripts, an estimate corroborated by other leading industry players.

- Cigna projects total spend growth below CPI, which will mean a 1-2% reduction in spend for its members, totaling more than

$5b annually in the coming years. For example, this could be achieved with $253 of annual medical cost savings across 20m lives, or 20% of the total base

who may adopt the full suite of Cigna / Express Scripts capabilities.

2. Cigna's long-term growth prospects will be stronger with the deal, and its per-share financial results will also be

approximately 15% higher both near and long-term.

3. Cigna is paying a cheap price for Express Scripts compared to its history and precedent PBM transactions, paying 13x

forward earnings (excluding Anthem) or 11.5x fully synergized earnings – approximately 25% below precedent transactions on an

EV/EBITDA basis and an even greater discount on a price / earnings basis.

4. Cigna has earned long term shareholders' trust based upon its 21%+ annual shareholder returns during Mr. Cordani's

eight-year term as CEO and its industry-leading control of medical costs.

5. Sensationalist headlines and intentionally misleading assertions from those with conflicting interests and limited analysis

should not carry more weight than balanced diligence.

Long-term healthcare services investors, including Glenview, have done well investing in companies who do good, such as Cigna.

Contrary to the sensationalist rhetoric of those pushing personal agendas, PBMs combat drug price inflation and encourage

better pharmaceutical adherence, improving patient outcomes. For this reason, nearly all major US corporations, including

nine owned by Mr. Icahn and every one of the companies mentioned as a potential emerging competitor, use a PBM to reduce their

pharmaceutical cost. In addition, the Trump Administration is pushing for more Medicare Part B drugs to be included in

PBM-assisted Medicare Part D. Both the Obama and Trump Administrations have challenged the for-profit healthcare system to

innovate to enhance quality while reducing the inflation rate and overall dollar spend within the US healthcare system.

Through the merger with Express Scripts, Cigna's Management and Board have provided shareholders the opportunity to do exactly

that, in a transaction that is additive to earnings and value per share for owners.

We welcome the debate and discussion raised by both supportive and dissenting analysts alike, and we strongly believe in the

democratic principles of shared governance. We agree that shareholders should do their own work, proxy advisory services

should delve into important governance and procedural issues, reporters and publishing analysts should ask critical questions and

seek substantiation for claims and assertions, and Management and Board members all should be accountable to shareholders.

Based upon our own analysis, which we further describe herein, we conclude the following:

a) Management and the Board have a strong track record worthy of respect for their views;

b) The proposed transaction is well valued, well financed and contains adequate margins of safety;

c) The strategic merit of vertical integration between managed care and pharmaceutical benefit management has been proven and

widely adopted by others in the industry;

d) The financial rewards of the transaction are compelling; and

e) The opportunity to lower health care costs for current and future consumers is exceedingly large, strengthening Cigna's

ability to grow and serve its clients for many years to come.

* * *

Glenview Capital Management, a hedge fund in its 18th year of operation, owns / controls an approximately

$1.3 billion investment in Cigna / Express Scripts, split approximately evenly between the two

companies. We have owned Cigna continuously since 2008. At the time of the deal announcement, we had no position in Express

Scripts. Following the deal announcement, we both increased our investment in Cigna and purchased a significant stake in Express

Scripts as a means to create "new Cigna" at a discount through the arbitrage spread.

A Look Back at Healthcare Services Overhangs Over the Years

We are well aware of the evolving regulatory and competitive landscape that both of the managed care and PBM industries face,

and experienced healthcare services investors have become used to such initial confusion. Set forth below are just a few of

the transitory concerns companies and owners have faced over the last two decades:

1. From 1998 through 2003, the PBM industry underwent enhanced regulatory, customer, activist and media scrutiny regarding its

transparency and the methods by which it reduced overall drug spend. Notwithstanding such oversight, PBMs were the best

performing sector in the S&P 500 in the decade of the 2000's, fueled by horizontal consolidation and strong earnings growth

generated by promoting price negotiation, generic conversion, pharmaceutical adherence, and mail order adoption.

2. In 2004 and 2005, pharmaceutical wholesalers fell out of favor with the investment community on fears that a migration to a

fee-for-service business model, as well as potential competition from global logistics players such as UPS, would negatively

impact their business. Yet, for the subsequent decade, the wholesale distribution industry generated strong per share

earnings and free cash flow growth driven by horizontal consolidation, scale purchasing, increasing capital efficiency and

logical capital allocation.

3. In September 2006, all of pharmaceutical services fell out of favor as Walmart, with its over

100 million[1] customers and immense purchasing power, introduced the concept of $4 generics

available in its stores, thus compressing the valuation multiples of drug retailers, distributors, and PBMs. Twelve years

later, Walmart's share of pharmaceutical retail has been cut in half.[2]

4. In 2008 through 2010, health insurers fell out of favor with investors as political and social advocates, as well as other

elements of the healthcare chain, blamed managed care for all that ailed the US healthcare system despite their profits being

less than 0.5% of total medical spend. Eight years later, the industry, including Cigna, has enjoyed strong membership and

profitability growth as it has served an increasing share of both private and government-run healthcare programs while curtailing

costs and promoting superior outcomes.

5. In 2011-2012, Medicare Advantage plans came under pressure as investors feared government mandated price reductions would

meaningfully reduce profit margins as reimbursement with traditional Medicare was equalized. Since then, shares of Humana,

the leading pure play Medicare Advantage company, increased five-fold, while its membership has nearly doubled.

6. In late 2016, hospital stocks suffered double digit declines upon the election results that welcomed in the Trump

Administration for fears that "Repeal and Replace" would pressure and eliminate both healthcare coverage for Americans as well as

hospital profits. Eighteen months later, the industry is experiencing strong admissions and fair reimbursement that

continue to power patient outcomes and earnings growth.

Pharmaceutical Inflation and the PBM Debate – Negotiation LOWERS Drug Prices

During the past four Presidential Administrations, much attention and focus has been paid to the price of pharmaceuticals and

the complexity of navigating the market. President and First Lady Clinton shined a light on the subject in the 1990s; in

the Bush Administration, we saw Medicare Part D rolled out to provide seniors with insurance coverage for pharmaceuticals; in the

Obama Administration, we saw several pilots to establish additional pathways for competition and innovation; and in the Trump

Administration, senior officials are focused on driving down list prices and closing the gap between US and global pharmaceutical

prices. Driven by the increasing mix of biologics and specialty drugs, along with the increased negotiating efficacy of

PBMs, the gap between list price inflation and net price inflation has grown ever wider in the past five years, keeping drug

costs within reach for American families.

According to IQVIA, both net prices paid and pharmaceutical co-pay inflation have been well controlled in recent years and are

projected to continue as such. Despite the media focus on drug prices, estimated price growth on high cost branded drugs has been

2-5% in recent years aided by PBMs' negotiating power. Absent the role PBMs played, branded drug prices would have risen at a

much greater rate over the same time frame.[3]

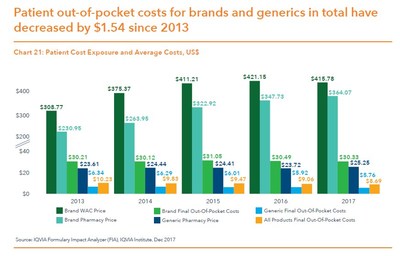

Additionally, out-of-pocket costs to consumers are actually down over the past five years. As shown below, while

branded prices have increased, out-of-pocket costs have been a) substantially lower and b) declining over time. This trend is the

result of PBM tools such as formularies and automatic substitution of generics.

Unfortunately, several bad actors in the pharmaceutical manufacturing space used either product shortages or other gimmicks to

push through usurious price increases, gouging consumers and burdening the healthcare system. While government officials,

activists and advocates have done an effective job in identifying and scrutinizing such behavior, it is appropriate that the

system remain vigilant to guard against another wave of bad faith by manufacturers. Notwithstanding, in the first six months of

2018, customers of Express Scripts experienced per member growth in pharmaceutical spending at about half the national inflation

rate, only 1.1%[4], reflecting the value of competitive negotiation through PBMs.

In addition, the government has recognized the excess value driven through Medicare Part D, which uses PBMs, versus Medicare

Part B, which presently does not. As described by CMS Administrator Seema Verma:

"The issues that we face are different in Part B and Part D. Let's start with Part B. Medicare pays Part B providers for

drugs at an amount equal to the average price the drug sells for plus a six percent add-on fee. This payment structure creates a

perverse incentive for manufacturers to set higher prices, and for providers to pick drugs that are more expensive. While this

system may have made sense when it was designed, in today's world, with some therapies costing over a half a million dollars,

adding 6% to the sales price doesn't make sense … Now to Part D, where the story is different. Part D is a market-based system.

At a time when premiums are rising in virtually every form of health insurance, premiums for Part D plans have been stable in

recent years and are actually lower this year than they were last year. In Part D, a group of negotiators works on behalf of

Medicare, to get a good deal for our beneficiaries. Plans hire PBMs to manage their drug benefit and to negotiate with drug

manufacturers." – CMS Administrator Verma, remarks at the American Hospital Association Annual Membership Meeting,

May 7, 2018. Emphasis added.

Finally, seniors who are in the "donut hole", or the uncovered portion of Medicare Part D, are charged proportional to List

rather than Net prices. As such, these Americans are victimized by growing gross price increases pushed through by the

manufacturers that are beyond the reach of PBMs. We applaud efforts by the Administration to attempt to collapse such gross

price increases provided that they don't eliminate the highly effective and functional negotiating incentives that PBMs have used

to drive down insurance premiums and overall drug spend for seniors.

While it is true that both HHS Secretary, Alex Azar, and Pfizer CEO, Ian Read, have made comments that question the alignment of interests inherent in the rebate system, these

comments need to be placed in context. Secretary Azar, FDA Commissioner Scott Gottlieb and CMS

Administrator Verma have all recognized the vital contribution of the PBM industry in recent commentary:

"And so we have actually proposed giving me the authority to move drugs from Part B into Part D where the PBMs can

negotiate on our behalf to secure -- to secure the kind of great deals -- the best -- we get the best deals of any payer in the

commercial marketplace right now in Part D because the PBMs negotiate that for us." – HHS Secretary Azar

testimony at the House Energy & Commerce Health Care Subcommittee hearing, February 15,

2018.

"I think that we need to do everything that we can do to make drugs more affordable for seniors and I'm thankful that we

have PBMs and the Part D program that are performing that negotiation on the behalf of seniors" – CMS Administrator Verma at

her Senate Finance Committee confirmation hearing, February 16, 2017.

"Part D is a market-based system – prescription drug plans compete for beneficiaries … At a time when premiums are

rising in virtually every form of health insurance, premiums for Part D plans have been stable in recent years and are actually

lower this year than they were last year." – CMS Administrator Verma remarks at the American Hospital Association Annual

Membership Meeting, May 7, 2018.

"PBMs have done important work in negotiating rebates that go toward reducing premiums – growth in rebates is a major

reason that Part D premiums have remained flat in recent years" – CMS Administrator Verma remarks at the American Hospital

Association Annual Membership Meeting, May 7, 2018.

"More broadly, the President has called on us to merge Medicare Part B into Part D, where negotiation has been so

successful on so many drugs. This is how we follow through on his promise to do smart bidding and tough negotiating for our

seniors." – HHS Secretary Azar remarks on Drug Pricing Blueprint, May 14, 2018.

"Generic substitution is just one of those success stories. The buying power of large PBMs and formulary design is one

reason that 81% of all small molecules drugs are available in generic formulations, and prices can fall by up to 80-90% after FDA

approves multiple generic competitors." – FDA Commissioner Gottlieb remarks in his 'Capturing the Benefits of Competition for

Patients' speech at America's Health Insurance Plans' (AHIP) National Health Policy Conference, March 7,

2018.

Further, prior Administration and government officials have similarly spoken to the good work of the PBMs:

"… [the PBMs] are the ones who have driven down prices. So Part D has been flat, price-wise, for almost ten years, it's

worked well, it's driven prices down." – Former CMS Administrator Tom Scully remarks in

CNBC interview, January 31, 2017.

"… PBMs compete to achieve lower costs, promote use of generics, use formularies to promote more affordable brand options …

This—the power of effective private sector negotiation and competition—is why the Medicare prescription drug plan has come in at

less than half of its original projected cost." – Former CBO Director Douglas Holtz-Eakin,

Forbes Magazine, November 29, 2016.

"Hypothetically, if full transparency of all rebates were implemented nationwide … manufacturers would probably reduce

their largest rebates because of the pressure that disclosure of such large rebates would place on their arrangements with other

customers" – Former CBO Director Peter Orszag in CBO letter to the Chairman & Ranking

Members of four Congressional committees, March 12, 2007.

We also note that Pfizer attempted to push through its second set of 2018 price increases in early July and then was convinced

by the Trump Administration to put such price increases on hold. Notwithstanding, for 2019, Pfizer saw Xyntha, Embeda and

Viagra excluded from Express Scripts' formulary in favor of clinically effective, lower-cost alternatives because Pfizer failed

to offer adequately low prices to Express Scripts' customers. We believe that Pfizer's commentary is best described as strategic

misdirection.

Much discussion has centered around the "elimination of rebates" in the system. We understand the theoretical argument

that if gross prices escalate and PBMs maintain a constant share of rebate dollars, then everyone appears to benefit from an

inflationary environment. However, a highly competitive PBM industry has behaved differently. Higher gross prices and

higher rebate dollars have led to lower percent rebate retention by the industry, as sophisticated clients and the myriad of

consultants and advisors who represent them in contract negotiation have become an adept check and balance. Over the last 15

years rebate retention in the industry has fallen from greater than 50% in 2003 to approximately a low-to-mid-single-digit

percent today. As disclosed by Cigna, rebates account for only 7% of Express Scripts' core EBITDA. Said differently and for

the sake of argument, assuming all rebates went away and ESRX could not find any alternative means for reimbursement from

clients, the acquisition P/E would increase to 14.0x stated and 12.4x synergized earnings per share, still well below comparable

transactions.

While competition caps PBM pricing and profitability, know-how and capability also places a floor under it, and PBMs are

functionally indifferent between rebates, point-of-sale discounts or other negotiated price breaks that carry with them

administrative or success fees. In point of fact, 100% of rebates collected in government programs are entirely passed

through to the government already, and Express Scripts' Tricare contract is done on a simple administrative fee, demonstrating

the flexibility PBMs offer today.

We offer these observations to support the following conclusions:

a) The noise in the PBM industry is not unique, nor existential. Prior episodes of regulatory scrutiny have favored those

businesses that do well for consumers and society. This time is not different;

b) The PBM industry has demonstrated an ability to lower drug costs and improve accessibility for American families;

c) The capabilities to adapt the business model have been repeatedly demonstrated by the industry as a whole and Express Scripts

in particular; and

d) By pattern and practice, the government is using private negotiating partners such as PBMs more to get a better deal:

a. Medicare Advantage penetration has grown from 13% to 33% from 2005 to 2017.[5]

b. Managed Medicaid penetration has increased from 63% to 81% from 2005 to 2016.[6]

c. Medicare Part D enrollment has expanded from 22m to 43m from 2006

to 2018.[7]

The Value of Independent Analysis

As analysts, we all are challenged to sort through the myriad of assertions and pick out the truth from the misleading, and to

resist succumbing to information that is incorrect but repeated so often that we assume it must be true. While we have

great respect for Mr. Icahn, we believe that analysts who are feeding him information and insight to encourage him to lead the

fight against this deal and the PBM industry may be arming him with information that is less than correct. We offer some

simple corrections and context as examples for the consideration of our fellow Cigna shareholders:

1. On Fox Business yesterday, Mr. Icahn said "They [Cigna] should have done that deal with Anthem, they could have fought the

Government and they could have got that thing accomplished." Cigna and Anthem did fight the Government, and lost in

court.

2. In his initial letter, Mr. Icahn said "Additionally, Express will go from being the 2nd largest PBM by number of

scripts to the 4th largest" once the Anthem prescriptions are removed in 2020. This is simply incorrect – pro

forma for the loss of Anthem, they remain #2.

3. In a letter this morning, Mr. Icahn says "According to a report published by Ross Muken and

Michael Newshel of Evercore ISI, Express Scripts likely earns close to $1.1

billion of EBITDA from rebates or $850 million ex-Anthem. This is more than 15% of their

total ex-Anthem EBITDA." Mr. Icahn chose to ignore a corrective note issued by Mr. Muken only six hours later that said,

based upon his review of an 8-K filed by Cigna, "Express Scripts retains approximately $400M of

rebates…far less than the roughly $850M we had estimated in a prior note this morning."

- This correction was published yesterday at 6pm, with plenty of time for Mr. Icahn to remove

the misleading information from his letter this morning.

- We applaud Mr. Muken for publishing this correction – while we have found much of his analysis to rely on significant

conjecture, we appreciate this effort to correct the record when possible.

4. Mr. Icahn repeatedly cites Pfizer CEO Ian Read's comments about PBM rebates as demonstrating

that PBMs somehow raise drug prices to consumers. A broader review of Pfizer's disclosures recognize that PBMs and tools

they employ in fact reduce cost and encourage the use of the lowest cost medically equivalent alternative, including the

following quotes from Pfizer's 2017 Form 10K:

- "[PBMs] increasingly employ formularies to control costs."

- "[PBMs] also use clinical protocols, requiring prior authorization for a branded product if a generic product is

available"

- "…biopharmaceutical companies may face greater pricing pressure from private third-party payers, who continue to drive more

of their patients to use lower cost generic alternatives"

5. Mr. Icahn cites that as a long-time trustee at Mount Sinai Medical Center, including his generous support of the Icahn

School of Medicine at Mount Sinai, he has seen first-hand the significant problem of

prescription drug pricing in America. We note that high drug prices in a hospital setting he may have witnessed are most

likely because of the absence of PBM access and tools in Mount Sinai, where new prescriptions

administered on site are paid for through either Medicare Part B, which does not partner with PBMs, or through a commercial

billing arrangement, which is largely prevented from accessing PBM discounts (as described by CMS Administrator Verma in quotes

we included earlier). The place Mr. Icahn could see PBMs value first-hand would be in the nine companies he controls, where

the experts he employs all renewed with Express Scripts within the past year.

6. Mr. Icahn asks index funds to vote against the deal because BlackRock CEO, Larry Fink, in a

2018 letter to CEOs laudably reminded our industry that companies must benefit the communities in which they operate.

Cigna's public disclosure indicates that the acquisition will enable them to reduce medical trend to below CPI, which implies an

incremental $5-10 billion of annual savings to Cigna customers and the payors responsible for their

healthcare (1-2% on $500 billion of aggregate spend). We believe that Cigna shareholders,

including Mr. Icahn, would be hard pressed to explain how saving customers and payors so much money is harmful to society and the

communities they serve, and that perhaps Mr. Icahn has been misled by misinformation fed to him by analysts with short-term

personal agendas.

Valuation and Financing Provide a Margin of Safety

Throughout our time as Cigna shareholders, we have found Management and the Board to be disciplined capital allocators.

Consistent with this approach, the negotiated price for Express Scripts appears highly attractive on a historical basis:

a) Cigna is paying 13x "core earnings" (excluding Anthem earnings that are going away in 2020) and 11.5x "synergized

earnings," which are core earnings including $600 million of synergies. This compares favorably to

other transactions on both a P/E and EV/EBITDA basis.

ESRX Multiple Paid

|

2019

|

|

|

|

EPS Adjustments

|

|

|

Consensus EPS[8]

|

$10.22

|

|

Less: EPS from Anthem[9]

|

($3.19)

|

|

EPS Adjusted for Anthem

|

$7.03

|

|

|

|

Purchase Price Adjustments

|

|

|

Value of Bid

|

$96

|

|

Less: Cash from Anthem[10]

|

($5)

|

|

Less: Capitalized Synergies[11]

|

($11)

|

|

Core Purchase Price

|

$81

|

|

Less: Added Capitalized Synergies per ESRX

|

($16)

|

|

Adjusted Core Purchase Price

|

$65

|

|

|

|

Core P/E including CI Synergies

|

11.5x

|

|

Core P/E including ESRX Synergies

|

9.2x

|

b) Cigna is financing the acquisition with 51% cash and 49% stock, maintaining investment grade ratings with a

well-termed debt structure and a clear path to delever to 40% debt-to-cap or below two years after the transaction's close.

We believe they will reach 32% debt-to-cap in this timeframe, leaving them $6-7b of firepower for share repurchase or even greater fire power for accretive M&A.

c) From 2008 to 2018, Express Scripts on average traded at 14x EPS and 9.2x EBITDA.[12] Clearly the private market value being

paid for the Company reflects a reasonable contingency for any degradation in economics due to incremental regulation or

competitive intensity. Moreover, we believe that the P/E multiple for ESRX backing out Anthem on average has been 16x over the

past five years and 18x over the past 10 years, magnifying the discount of its current valuation.

d) Tax reform increased Express Scripts' after-tax earnings and equity value by 21% as a result of higher retained earnings under

the new tax regime. We believe attempts to characterize the premium paid to "pre-affected" stock price fails to recognize

this exogenous event that drove the fundamental value of ESRX higher. The premium offered of 31%[13] is in line with prior

deals, but it is less relevant to us, as the value of a company is its chain weighted discounted cash flows, not an arbitrary

premium on a volatile trading value.

e) Mr. Icahn references the value destruction in the AOL / Time Warner transaction as a reason to vote against this deal.

At the time of that merger, AOL was trading for over 200x[14] forward earnings, a far cry from 13x / 11.5x standalone /

synergized earnings per share. While no price is low enough for a strategically poor deal, we believe that the acquisition

multiples provide adequate cushion for unexpected fundamental headwinds.

Cigna Management and Board Have Earned Our Trust

Under Mr. Cordani's leadership, Cigna has thrived:

a) Since taking the helm in 2009, CI's overall medical membership has grown from 11 million to 16 million, and the Company has

expanded into key growth areas like Medicare Advantage while avoiding industry pitfalls such as rushing into Public Exchanges.

b) Cigna has achieved the lowest medical trend of major Managed Care Organizations over the last eight years. Cigna expects this

performance to continue in 2018.[15]

c) During Mr. Cordani's tenure, shareholders have enjoyed a 21%+ annual return, outpacing relevant indices and benchmarks.[16]

d) We believe Cigna's Board has demonstrated responsible risk management. Under Mr. Cordani's leadership, Cigna exited the

Variable Annuity Defined Benefit business and associated liabilities (the "VADB" liabilities) that effectively exposed Cigna to

significant risk in an equity market downturn. This stands in stark contrast to the continuous ownership and losses of GE

Capital, the finance arm retained by GE, which was also referenced by Mr. Icahn as a reason not to pursue this deal.

e) Management and the Board entered into an agreement with Anthem to sell the Company, which was subsequently blocked by the

Department of Justice on anti-trust grounds. While it has been suggested that Mr. Cordani would have preferred to remain

CEO of an independent entity, he and the Board put shareholders first by agreeing to sell to Anthem, and thus, have reinforced

their alignment with owners.

f) Shareholders recognized the Board's stewardships with a 96% vote for the re-election of directors at the last annual meeting

and a 98%[17] vote for the re-election of Mr. Cordani, almost two months after the announcement of the Express Scripts

transaction.

Plan B – Voting Down the Deal – Appears to be Backward Looking and Brings Additional Risk

Our firm has been a steadfast advocate of share repurchase as a tool to create shareholder value in growing, undervalued

companies that are strategically complete. In addition, we do support measured, bolt-on acquisitions that are digestible,

well-diligenced and appropriately financed if they offer superior risk-adjusted returns. Thus, in general, strategies such

as those Mr. Icahn and external analysts he references hold some attraction. However, in this specific circumstance, a

share repurchase and PBM partnership strategy seems inferior:

a) If shareholders fail to approve the deal, Cigna will have failed to integrate both horizontally (anti-trust) and vertically

(lack of confidence from shareholders). Given Management's strong contention about the need for integrated scale

capabilities to continue to lead and innovate, Cigna will be rendered strategically incomplete without a clear path to closing

the gap.

b) While some suggest that a "no" vote means a simple return to the status quo, we believe such logic misses the simple

point that a "no" vote in this transaction is akin to a "no confidence" vote in Cigna Management and Board and could crystallize

a potentially irreconcilable difference between a block of dissenting shareholders and this top tier Cigna management team. A

"no" vote may prompt turnover in senior management or the Board leading the Company to deviate from its strong historical path.

c) Strategically, ESRX is the best asset to position CI for the evolving, vertically integrating health care supply chain. Other

PBMs are captive, subscale, or both. In the managed care and PBM space, JVs and strategic alliances have been tried by multiple

players and have proven to be incapable of capturing full value for consumers and shareholders. The industry has shown that fully

integrated ownership is more efficient and effective in driving economics and outcomes for sponsors and patients.

a. In one example, 40% of diabetics have behavioral co-morbidities. Those patients tend to spend

30% more on medical care. By integrating pharmacy, medical, and behavioral benefits, Cigna would be able to identify diabetic

patients and provide medical and behavioral health support to lower medical expenses. This sort of care coordination is far more

difficult to achieve effectively - or with the necessary speed to drive optimal outcomes - unless the PBM and managed care plan

are under common ownership

b. In 2013, Cigna outsourced its PBM to Catamaran, which was later acquired by UNH. Having operated this strategic alliance for

five years, Cigna concluded that owning the PBM was the best way to achieve the benefits of integration. According to a Cigna

study, when pharmacy and medical benefits are integrated, customers save $253[18] per member per

year on medical expenses and members achieve better health outcomes. With ESRX, the pool of relevant patients and cost savings

will expand, offering an integrated pharmacy and medical benefit, with the top-tier scale and leadership that ESRX brings on the

pharmacy side.

c. UNH and OptumRx are regarded as the first fully integrated medical and pharmacy benefit manager and together, are a market

leader. By combining the medical and pharmacy files, UNH can save its customers over $200[19] per

year on medical expenses, or ~4%.

d. When AET and CVS merge, the combined entity expects to reduce medical expenses by $240[20] per

member per year through integration. Importantly, AET and CVS had been operating in partnership for the past eight years. Based

on the learnings of that experience, the companies decided that a business combination was the optimal path forward.

Proxy Advisory Services Have Illustrated the Benefits of Looking Past Short-Term Stock Reactions and Towards

Underlying Strategic and Financial Rationale – to the Benefit of Investors

Mr. Icahn writes that Cigna's stock price has traded lower since before announcing the deal. While that is true, we do not

believe that it provides any indication of the long term value creation of the deal. Further, we applaud shareholder advisory

services like Glass Lewis and ISS for focusing on the fundamental merits of a transaction instead of this short-term and less

meaningful indicator.

When Centene announced the acquisition of HealthNet in 2015, Centene shares traded down by 34%, underperforming the S&P

500 and the relevant healthcare index[21] by 29% and 23%, respectively. Despite this initial reaction, ISS and Glass Lewis

correctly identified the long term fundamental benefits of the transaction, including strategic rationale and EPS accretion.

After ISS and Glass Lewis recommended that shareholders vote for the deal, Centene shares outperformed benchmarks by over 90%,

including a total shareholder return of 117% in the first two years following the vote.

Similarly, following the announcement of CVS's acquisition of AET, CVS shares traded down by 10%, underperforming the S&P

500 and the relevant healthcare index[22] by 19% and 21% respectively. Again, ISS and Glass Lewis were able to focus on the right

fundamentals: EPS accretion and strong industrial logic, which mirrors that of the ESRX/CI transaction. We applaud ISS and Glass

Lewis for taking into account the fundamental positives and risks to the transaction, including the current regulatory

environment, and recommending the transaction.

* * *

Critics of the PBM industry and this acquisition have questioned to role and value of middlemen, characterizing them as an

unnecessary, unwise and unfair tax on the system. We believe such arguments are incorrect, and short-sighted:

a) In order to procure consumer goods cheaper, Americans turn daily to stores like Costco, who for a fee, access cheap

branded and generic food and dry goods on behalf of their members and deliver significant savings and value to their customers

through their bulk purchasing power. They collect both a membership fee and a "spread" or gross margin on the goods that

they sell, but clearly Costco customers are better off for the net savings they enjoy.

b) In order to procure travel services cheaper, Americans turn daily to on-line travel agencies such as Expedia, who aggregate

demand for rooms and airline seats and through their bulk purchasing power deliver great deals to travelers that were otherwise

inaccessible on their own. They earn proportional to the value they provide and the competitiveness of the OTA market – if

they are earning too much for the value they provide, then consumers will switch OTAs.

c) In order to obtain raw materials and inventory efficiently, American corporations employ procurement departments or

participate in GPOs, or group purchasing organizations, who use their collective heft to bid venders of functionally equal goods

or services against one another in order to obtain the most efficient price. Surely firing the procurement department would

save money the next day, but it would also be exceedingly costly to the system and the consumer over any reasonable period of

time.

Each of these entities is value added, and each of them earns a return proportional to the value it brings to its

consumers. They are not a tax on the system, they are a service to their consumers, containing costs and overseeing quality

on behalf of their constituents. The value PBMs produce are so significant that client retention rates are in the high 90s,

and they serve nearly all significant American corporations and health plans. While we could reduce the price of a car by

eliminating airbags, it would certainly not be advisable. We believe PBMs are a vital tool for consumers and payers to

negotiate fair rates for medications and to promote competition amongst vendors of functionally equivalent products.

In conclusion, we thank the Board and Management of Cigna for allowing us as shareholders the opportunity to do well while the

Company is doing significant good for its customers and constituents. We believe that Cigna has well exceeded the "burden

of proof" necessary to support a transaction of this magnitude, and we hope that the vast majority of Cigna shareholders will

reach the same conclusion. Thank you for your time and consideration.

Respectfully,

Glenview Capital Management

Disclaimers

Glenview Capital Management, LLC ("Glenview") serves as the investment manager to each of Glenview Capital Partners, L.P.,

Glenview Institutional Partners, L.P., Glenview Capital Master Fund, Ltd., Glenview Capital Opportunity Fund, L.P., Glenview

Offshore Opportunity Master Fund, Ltd., GCM Equity Master Fund LP and a separately managed account (collectively, the "Glenview

Funds"). The Glenview Funds hold or have long economic exposure to 3,222,210 shares of common stock of Cigna Corporation

("Cigna") and 8,699,819 shares of common stock of Express Scripts Holding Company ("Express Scripts"). These holdings are

subject to change, and Glenview may buy additional shares of Cigna or Express Scripts, sell shares of Cigna or Express Scripts,

or enter into derivative transactions (whether "long" or "short") with respect to Cigna or Express Scripts at any time. The views

and opinions set forth in this letter should not be considered as a recommendation to buy, sell or hold any particular security,

including those of Cigna or Express Scripts.

Glenview is not engaged in a proxy solicitation, is not soliciting proxies relating to either the Cigna special meeting of

shareholders or the Express Scripts special meeting of stockholders and does not have, and is not seeking, the authority to vote

your proxy at either meeting. No agreement, commitment, understanding or other legal relationship exists or may be deemed

to exist between or among Glenview or any other person by virtue of Glenview issuing this letter.

This material set forth in this letter is for general informational purposes only and is not intended to be relied upon as

investment advice. The views and opinions expressed are those of Glenview as of the date hereof and are subject to change at any

time due to changes in market or economic conditions. Glenview makes no undertaking (and is under no obligation) to update

any such views or opinions.

The information and opinions contained in this material are derived from proprietary and non-proprietary sources deemed by

Glenview to be reliable and are not necessarily all inclusive. Glenview does not guarantee the accuracy or completeness of this

information. There is no guarantee that any forecasts made will come to pass. Glenview disclaims any liability for any

reliance upon information in this letter.

This presentation does not constitute (and may not be constructed to be) a solicitation or offer by Glenview or any of its

directors, officers, employees, representatives or agents to buy or sell any securities of Cigna, Express Scripts or any

other person in any jurisdiction or an offer to sell any interest in funds managed by Glenview. This

presentation does not constitute financial promotion, investment advice or an inducement or encouragement

to participate in any product, offering or investment or to enter into any agreement with Glenview, a Glenview Fund or

any other person. No representation or warranty is made that Glenview's investment processes or objectives will be

achieved or that Glenview's investments will not sustain losses. Past performance is not indicative of future

results.

Cautionary Statement Regarding Forward-Looking Statements

This letter may contain forward-looking statements. All statements contained in this letter that are not clearly

historical in nature or that necessarily depend on future events are forward-looking, and statements that include the words

"anticipate," "believe," "expect," "estimate," "plan," "will" and similar expressions are generally intended to identify

forward-looking statements. These statements are based on current expectations of Glenview and currently available

information. They are not guarantees of future performance, involve certain risks and uncertainties that are difficult to

predict, and are based upon assumptions as to future events that may not prove to be accurate.

[1] PBS (https://www.pbs.org/wgbh/pages/frontline/shows/walmart/secrets/stats.html)

[2] Per data from Chain Store Review (8/2/2007), Drug Store News (4/2/2015), and US Census Bureau

[3] IQVIA Report, Understanding the Drivers of Drug Expenditure in the U.S., 9/2017

[4] Express Scripts Press Release, 8/1/2018

[5] Kaiser Family Foundation (https://www.kff.org/medicare/issue-brief/medicare-advantage-2017-spotlight-enrollment-market-update/)

[6] CMS (Medicaid Managed Care Enrollment Report: Summary Statistics as of July 1, 2011 and

Medicaid Managed Care Enrollment and Program Characteristics, 2016)

[7] Kaiser Family Foundation (https://www.kff.org/medicare/issue-brief/medicare-part-d-in-2018-the-latest-on-enrollment-premiums-and-cost-sharing/)

[8] Bloomberg Consensus EPS estimate as of 3/7/2018

[9] Anthem contract is stated to contribute approximately $2.4B in EBITDA

[10] We reduce the value of ESRX stock by the cash value expected from the remainder of the Anthem contract

[11] $600MM of synergies capitalized at 10x

[12] These valuation metrics are understated due to the inclusion of Anthem earnings in historical ESRX estimates

[13] ESRX Press Release, 3/8/2018

[14] CapitalIQ

[15] Cigna Investor Presentation, 2/1/2018

[16] Including S&P 500 and the GICS index

[17] Cigna 8-k, 4/30/2018

[18] Cigna Presentation, "The Point of Connection", 2/2018

[19] Sanford Bernstein Conference, 5/31/2018

[20] AET/CVS Deal Announcement Conference Call

[21] Per ISS, MSCI ACWI: Healthcare Providers and Services Index GICS 351020

[22] Per ISS, MSCI ACWI: Healthcare Providers and Services Index GICS 351020

Mike Geller

Prosek Partners (on behalf of Glenview Capital Management)

347-275-3577

Pro-glenview@prosek.com

View original content with multimedia:http://www.prnewswire.com/news-releases/long-term-cigna-shareholder-glenview-capital-submits-open-letter-to-shareholders-in-support-of-cigna--express-scripts-transaction-300694989.html

View original content with multimedia:http://www.prnewswire.com/news-releases/long-term-cigna-shareholder-glenview-capital-submits-open-letter-to-shareholders-in-support-of-cigna--express-scripts-transaction-300694989.html

SOURCE Glenview Capital Management