Stocks in the financial sector have been putting up some mixed performances of late as the Fed has

continued to hike interest rates. Overall, the S&P Financial Select Sector Index (IXM) is down 1.2 percent year-to-date,

although the sector dropped 2.89 percent in September alone, with one red day after another from September 21 to the end of the

month.

Within the sector, credit card companies and payment processors like Square Inc. (NYSE:

SQ), MasterCard Inc. (NYSE: MA), Visa Inc. (NYSE: V) and PayPal Holdings Inc. (NASDAQ: PYPL) have outperformed the S&P 500 (SPX) by a wide margin, with year-to-date

returns ranging from 18.96 percent for PYPL to 173.74 percent for SQ. Data and exchange-related financial businesses, like the

Intercontinental Exchange Inc. (NYSE: ICE), CME Group

Inc. (NASDAQ: CME) and S&P Global

Inc. (NYSE: SPGI) have been stronger performers

within the sector as well.

The laggards have been the investment banks and asset managers, while many of the larger, diversified banks

have been underperforming: Goldman Sachs Group Inc. (NYSE: GS), Morgan Stanley (NYSE: MS) and Wells Fargo & Co. (NYSE: WFC) are all down more than double-digits in 2018. JP Morgan Chase &

Co. (NYSE: JPM) is one of the few of the big banks

that is positive on the year, up 4.53 percent as of October 1.

At this point, prospective regulatory reform has likely been baked into stock prices. The rewrite of

Dodd-Frank went through at the end of May, which was mostly geared towards loosening regulation for small and mid-size banks. Tax

reform and continued economic strength have also provided a positive backdrop for the sector this year.

While there have been a lot of positives for the sector, some analysts are starting to question how long

the economy can grow at this pace, and how long corporations and consumers can maintain demand for loans.

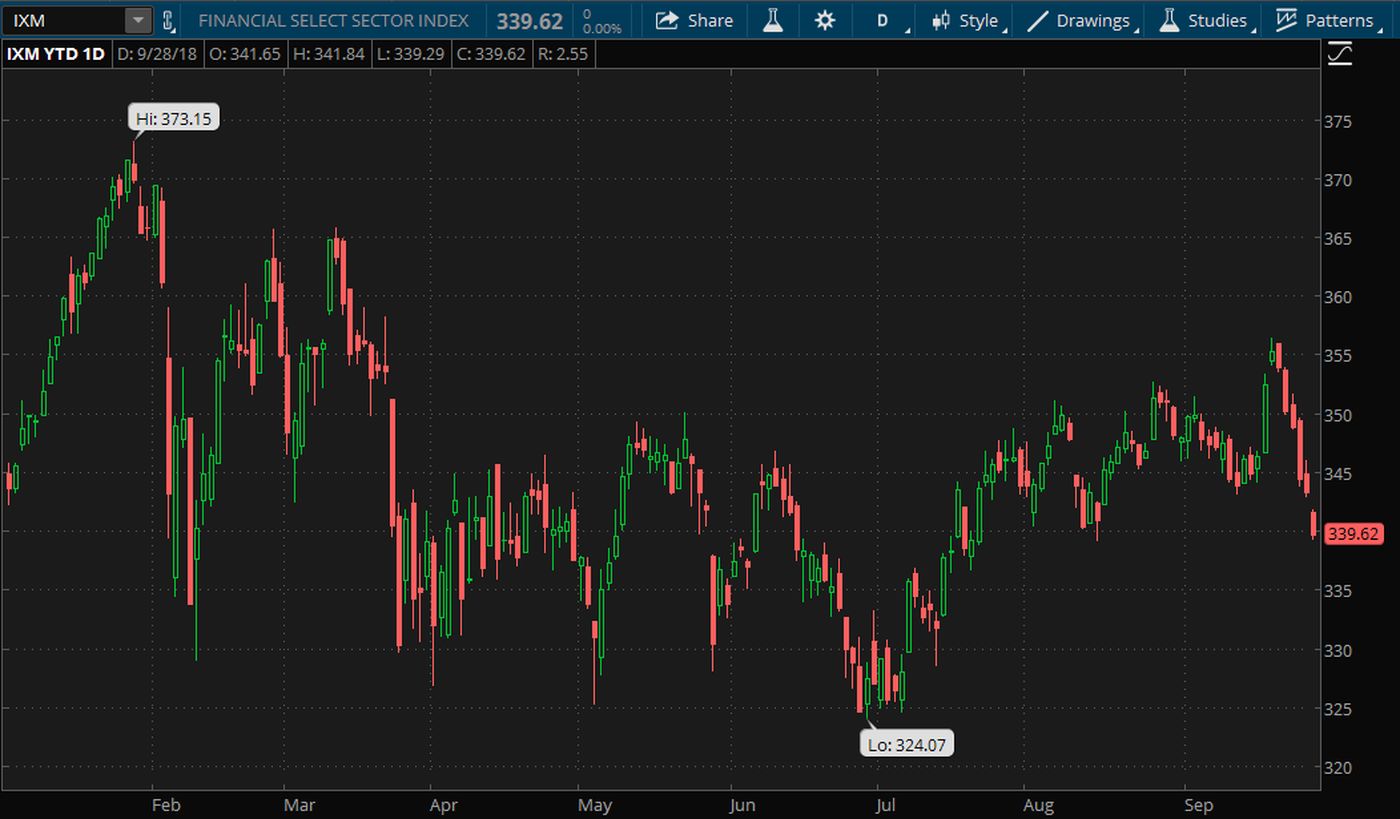

Financial Sector 2018 Performance. The S&P Financial Select Sector has been trading in

a tighter range since mid-July. Leading up to the recent September Fed meeting, financial stocks put in a stretch of

underperformance. Goldman Sachs (GS) declined for 11 sessions straight at the start of September, its longest losing streak since

its IPO in 1999. Chart source: thinkorswim® by TD Ameritrade.

Not a recommendation. For illustrative purposes only. Past performance does not guarantee future results.

Q3 Earnings Season

Revenue estimates have been trending downward for the financial sector. The consensus analyst estimate for revenue growth was

3.2 percent year-over-year on June 30, according to FactSet, but that had dropped to a 1.4 percent decline by September

28.

Despite the downward revisions to revenue estimates, analyst expectations are still on the high end for earnings. The financial

sector currently has the second highest expected earnings growth out of all eleven sectors in the S&P 500, according to

FactSet, and all five industries are expected to report double-digit earnings growth.

Since the insurance industry had weak earnings last year due to hurricane-related losses, its estimated earnings growth rate is

159 percent.

Checking in on the Fed

The Fed’s recent interest rate hike marked the third rate increase this year and the eighth in the current hiking cycle, which

began in late 2015. The Treasury markets didn’t move too much following the announcement, potentially due to the fact that many had

been pricing in the Fed’s expected quarter-point bump for several months.

As of October 1, odds of a fourth rate hike this year were at about 77 percent, according to CME Group futures. Since the Fed’s

meeting at the end of September, the chances for more rate hikes in 2019 have been on the climb, with about a 45 percent chance of

another one in March followed by around a 30 percent chance of a June hike.

The Fed’s forecast for future rate levels, known as the “dot plot”, didn’t change all that much this time out. A December rate

hike looks pretty certain if you follow the dots, and many Fed officials indicated they think the appropriate Fed Funds rate is

around 3 percent in 2019 and closer to 3.5 percent by 2020.

No Help from Yield Curve

As the Fed has hiked rates, the yield curve has continued to flatten, weighing on the financial sector’s performance. When the

yield curve is flatter, there is less of a difference between short and long-term yields, which weighs on banks’ net interest

income since they tend to borrow in the short-term and lend in the long-term (mortgages, auto loans, etc.)

Not only has the flattening yield curve posed challenges for the sector, higher interest rates can crimp corporate borrowing,

and they can make buying a house more expensive at a time when prices are already at record highs.

Overall, most analysts are still positive regarding the current interest rate cycle and expect that the curve will normalize

over time.

Spread Between 10-Year and 2-Year Treasuries. The difference between the 10-year and

2-year Treasury yields, two benchmark interest rates, has remained low after continuing to decline over the first half of the

year. TD Ameritrade clients can access economic data points by going to Analyze > Economic

Data in the thinkorswim® platform. For illustrative

purposes only.

Upcoming Earnings Dates

Below are some of the upcoming earnings dates for financial sector companies that have confirmed their dates:

- JP Morgan (JPM), Wells Fargo (WFC), Citigroup Inc. (NYSE: C), and PNC Financial Services Group Inc. (NYSE: PNC) all report before market open Friday, October 12.

-

Bank of America Corporation (NYSE: BAC)

releases results before the open Monday, October 15.

- Investment banks Goldman Sachs (GS) and Morgan Stanley (MS) report before the open Tuesday, October 16.

- MasterCard (MA) reports before the open Tuesday, October 30.

CME Group (CME), S&P Global (SPGI), and Visa (V) are expected to report towards the end of October, but they haven’t

confirmed their reporting dates yet. For a rundown on what’s been going on at different companies and a review of options activity

ahead of major reports, make sure to check out the Ticker Tape throughout earnings season.

Information from TDA is not intended to be investment advice or construed as a recommendation or endorsement of any

particular investment or investment strategy, and is for illustrative purposes only. Be sure to understand all risks involved with

each strategy, including commission costs, before attempting to place any trade.

© 2018 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.