VANCOUVER, British Columbia, Sept. 12, 2022 (GLOBE NEWSWIRE) -- K92 Mining Inc. (“K92” or the “Company”) (TSX: KNT; OTCQX: KNTNF) is pleased to announce the results of its Integrated Development Plan (“IDP”) for its Kainantu Gold Mine Project (the “Kainantu Project”) in Papua New Guinea. The IDP comprises two scenarios: 1) Kainantu Stage 3 Expansion Definitive Feasibility Study Case (“DFS” or “DFS Case”); and 2) Kainantu Stage 4 Expansion Preliminary Economic Assessment Case (“PEA” or “PEA Case”). The results of the IDP will be set forth in an independent technical report prepared in accordance with National Instrument 43-101- Standards for Disclosure of Mineral Projects (“NI 43-101”) within forty-five days from this date.

Integrated Development Plan Highlights:

- The DFS Case evaluates the Stage 3 Expansion to 1.2 million tonnes per annum (“mtpa”), representing a 140% throughput increase from the Stage 2A Expansion. Stage 3 involves a new standalone 1.2 mtpa process plant and supporting infrastructure constructed with mining focused on the Kora Central Zone within the Kora Deposit and Judd Deposit, utilizing a cut-off grade of 3.0 grams per tonne (“g/t”) gold equivalent (“AuEq”).

- After-tax NPV5% of US$586 million at US$1,600 per ounce gold, with no internal rate of return (“IRR”) as the project generates cashflow during construction. After-tax NPV5% of US$855 million at US$2,000 per ounce gold.

- Average annual run-rate production of 290,771 ounces AuEq per annum, run-rate achieved in 2025 and a peak annual production of 308,793 ounces AuEq in 2026.

- Life of Mine average cash costs of US$366 per gold ounce and all-in sustaining cost (“AISC”)(2) of US$545 per gold ounce over a 7-year mine life.

- Growth capital cost of US$177 million, sustaining capital cost prior to commissioning of US$125 million and life of mine sustaining capital cost of US$218 million.

- The alternate PEA Case evaluates two-stages of expansions to a run-rate throughput of 1.7 mtpa, representing a 240% throughput increase from the Stage 2A Expansion. The ultimate run-rate throughput of the second expansion is referred to as Kainantu Stage 4 Expansion, operating two standalone process plants, larger surface infrastructure and mining throughputs achieved through mining Kora Upper, Lower, and Central Zones within the Kora Deposit, and the Judd Deposit, utilizing a cut-off grade of 4.5 g/t AuEq.

- After-tax NPV5% of US$1.3 billion at US$1,600 per ounce gold with no IRR as the project generates cashflow during construction. After-tax NPV5% of US$1.8 billion at US$2,000 per ounce gold.

- Average annual run-rate production of 405,661 ounces AuEq per annum, run-rate achieved in 2027 and a peak annual production of 500,192 ounces AuEq in 2027.

- Life of Mine average cash costs of US$275 per gold ounce and AISC(2) of US$444 per gold ounce over an 11-year mine life.

- Growth capital cost of US$187 million, sustaining capital cost until operating both process plants of US$235 million and life of mine sustaining capital cost of US$429 million.

- Both the DFS and PEA Cases are fully funded from mine production and mine cash flow. K92 has a strong financial position having, as at June 30, 2022, a cash balance of US$82 million and no debt, and on July 6, 2022, closed a C$50 million bought deal equity financing.

- Low environmental impact through being supplied with clean hydroelectricity, mining high grades with both the DFS and PEA Cases outlining a low footprint, no-cyanide operation, with a majority of tailings reporting underground as paste fill, and an environmentally friendly paste binder solution. K92 plans to upgrade the grid infrastructure, which is expected to significantly reduce greenhouse gas emission intensity per ounce produced near-term. WSP Consultants has been engaged to complete a green house gas emissions forecast for the IDP which will improve K92’s corporate climate change goal and target setting, and which will be released in due course.

- AuEq – calculated on the following metal prices: Au – US$1,600/oz, Ag – US$20.00/oz, Cu – US$4.00/lb. Note that gold equivalence factors for the production estimates are different to those used for reporting the Mineral Resource estimate.

- AISC – All-In Sustaining Costs include cash costs plus estimated corporate general and administrative (“G&A”) costs, sustaining costs and accretion.

The IDP, which includes the Kainantu Stage 3 Expansion DFS Case and the alternative Kainantu Stage 4 Expansion PEA Case, was independently prepared by Lycopodium Minerals Pty Ltd (“Lycopodium”) of Brisbane, Australia; Entech Pty Ltd of Perth, Australia and Entech Mining Ltd of Toronto, Canada (collectively referred to as “Entech”); ATC Williams Pty Ltd (“ATC Williams”) of Brisbane, Australia; MineFill Services Pty Ltd. (“MineFill”) of Newcastle, Australia, and; H & S Consultants Pty. Ltd of Sydney, Australia.

The PEA is preliminary in nature and includes Inferred Mineral Resources that are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorized as Mineral Reserves, and there is no certainty that the PEA will be realized. Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability. Mineral Reserves are defined by the Definitive Feasibility Study and are not predicated on the Preliminary Economic Assessment in any way.

John Lewins, K92 Chief Executive Officer and Director, stated, “The Integrated Development Plan represents a major milestone for K92, providing independent verification by some of the world’s leading engineering firms of Kainantu’s robust economics. The Stage 3 Expansion Definitive Feasibility Study delivers capital expenditures fully funded from mine cash flow, Tier 1 peak production scale of 309 koz AuEq, Tier 1 costs averaging over the life of mine of $366/oz cash costs and all-in sustaining cost of $545/oz and a solid after-tax NPV5% of $586 million at US$1,600/oz or US$855 million at US$2,000/oz over a 7-year mine life.

The Preliminary Economic Assessment, shows potential for further growth, increasing throughput by 240% from the Stage 2A Expansion for a run-rate for a peak production of 500 koz AuEq, low life of mine average cash costs of $275/oz and all-in sustaining costs of $444/oz with a NPV5% of $1.3 billion at US$1,600/oz or US$1.8 billion at US$2,000/oz over an 11-year mine life. PEA capital expenditures are also fully funded from mine cash flow and it is important to highlight that K92’s financial position has never been stronger than it is today.

It is also important to highlight that we see a tremendous opportunity to enhance the outcomes of the Integrated Development Plan through exploration in addition to other regional targets and have placed a major focus on this. Since late-2021, we have increased our exploration budget and our drills have shifted from predominantly infill drilling to resource growth exploration. There are up to 11 drill rigs operating on surface and underground, targeting multiple near-mine targets including Kora, Kora South, Judd and Judd South, with plans to target Kora Deeps later this year from the twin incline. Porphyry exploration has also made considerable progress with the maiden inferred resource at Blue Lake announced last month and surface exploration at A1 has already commenced.”

1 – Kainantu IDP - Definitive Feasibility Study Case

1.1 - DFS Overview

The DFS evaluates an expansion of mining and processing to a run-rate throughput of 1.2 mtpa, representing a 140% increase from the Stage 2A run-rate of 500,000 tonnes per annum (“tpa”). This expansion is referred to as the Stage 3 Expansion and involves on-site treatment of ore by a new standalone 1.2 mtpa process plant, utilizing single stage crushing, SAG and ball milling, gravity and flotation recovery.

The DFS and mineral reserve statement is derived from the Company’s Mineral Resource estimate for Kora (effective date of October 31, 2021) and Judd (effective date of December 31, 2021), with Kora depleted based on mining actuals until December 31, 2021, and does not incorporate post-resource-estimate drilling results.

Table 1.1: DFS Highlights

| US Dollars unless otherwise stated |

Life of Mine

(starting January 2022) |

Stage 3 Expansion

(Q3 2024 onwards) |

| Production |

|

|

| Mine life (years) |

7 years |

|

| Total mill feed (000s tonnes) |

6,153 |

|

| Average mill throughput (tonnes per annum) |

879 ktpa |

1.2 Mtpa (run-rate)(1) |

|

|

|

| Total Metal Production |

|

|

| AuEq (000s ounces) |

1,544 |

1,049(2) |

| Gold (000s ounces) |

1,224 |

799(2) |

| Copper (mlbs) |

114 |

89(2) |

| Silver (000s ounces) |

2,773 |

2,164(2) |

|

|

|

| Peak Annual Production |

|

|

| Year |

|

2026 |

| AuEq (000s ounces per annum) |

|

309 |

|

|

|

| Average Annual Metal Production |

|

|

| AuEq (000s ounces per annum) |

221 |

291 (run-rate)(1) |

| Gold (000s ounces per annum) |

175 |

224 (run-rate)(1) |

| Copper (mlbs per annum) |

16 |

24 (run-rate)(1) |

| Silver (000s ounces per annum) |

396 |

574 (run-rate)(1) |

|

|

|

| Average Grade |

|

|

| AuEq grade (g/t) |

8.4 g/t |

|

| Gold grade (g/t) |

6.7 g/t |

|

| Copper grade (%) |

0.9% |

|

| Silver grade (g/t) |

18 g/t |

|

|

|

|

| Average Recovery |

|

|

| Gold Recovery (%) |

93% |

|

| Copper Recovery (%) |

95% |

|

| Silver Recovery (%) |

80% |

|

|

|

|

| Costs |

|

|

| Mining cost per tonne (US$/t) |

$66.54 |

$61.97 (run-rate)(1) |

| Processing cost per tonne (US$/t) |

$17.36 |

$15.32 (run-rate)(1) |

| G&A cost per tonne (US$/t) |

$32.43 |

$28.88 (run-rate)(1) |

| Total operating cost per tonne of mill feed (US$/t) |

$116.34 |

$106.17 (run-rate)(1) |

| Sustaining capital per tonne of mill feed (US$/t) |

$35.50 |

$19.26 (run-rate)(1) |

| Total cost per tonne of mill feed (US$/t) |

$151.83 |

$125.43 (run-rate)(1) |

|

|

|

| Expansion capital expenditure ($m) |

$177 |

|

| Sustaining capital expenditure ($m) |

$218 |

|

| Total capital expenditure with closure costs ($m) |

$402 |

|

|

|

|

| Cash cost per ounce AuEq ($/oz)(3) |

$574 |

$554 (run-rate)(1) |

| All-in sustaining cost per ounce AuEq ($/oz)(4) |

$716 |

$634 (run-rate)(1) |

| Cash cost per ounce gold ($/oz)(3) |

$366 |

$313 (run-rate)(1) |

| All-in sustaining cost per ounce gold ($/oz)(4) |

$545 |

$416 (run-rate)(1) |

|

|

|

| Base Case Economic Analysis at US$1,600/oz Gold, US$4.00/lb Copper and US$20.00/oz Silver |

| After-tax NPV0% |

$729 million |

|

| After-tax NPV5% |

$586 million |

|

| IRR (%) and Payback Period (years) |

N/A (Self-Funded) |

|

|

|

|

| Economic Analysis at $2,000/oz Gold, US$4.00/lb Copper and US$20.00/oz Silver |

| After-tax NPV0% |

$1,051 million |

|

| After-tax NPV5%(5) |

$855 million |

|

| IRR (%) and Payback Period (years) |

N/A (Self-Funded) |

|

- Run-rate excludes the final partial calendar year of production.

- Excludes 2H 2024 commissioning and initial ramp-up stage.

- Cash costs are net of by-product credits and are inclusive of mining costs, processing costs, site G&A and refining charges and royalties.

- AISC includes cash costs plus estimated corporate general and administration costs, sustaining costs and accretion.

- Net present value is calculated utilizing mid-year discounting.

1.2 - Kainantu Mineral Reserve Statement

The mineral reserve estimate outlined in the DFS was prepared by Patrick McCann PEng, of Entech Mining Ltd and Shane McLeay FAusIMM of Entech Pty Ltd, in accordance with the classification criteria set out in the 2014 CIM Definition Standards for Mineral Resources and Mineral Reserves prepared by the CIM Standing Committee on Reserve Definitions. Patrick McCann and Shane McLeay are independent consultants of the Company and are Qualified Persons as defined by NI 43-101. The total Mineral Reserve for the Kainantu Project is shown in Table 1.2. The mineral reserve estimate is based on the Judd mineral resource estimate (December 31, 2021 effective date – refer to Table 1.3) and the Kora mineral resource estimate (October 31, 2021 effective date – refer to Table 1.3), net of post-resource mining depletion from November 1, 2021 to December 31, 2021 of 36,765 tonnes at 12.94 g/t Au, 0.59 % Cu and 9.29 g/t Ag.

Table 1.2 – Kainantu Mineral Reserve Statement (Effective Date January 1, 2022)

|

Tonnes |

Gold |

Silver |

Copper |

AuEq |

|

Mt |

g/t |

moz |

g/t |

moz |

% |

kt |

g/t |

moz |

| Kora |

|

|

|

|

|

|

|

|

|

| Proven |

2.26 |

7.58 |

0.55 |

14.96 |

1.09 |

0.82 |

18.52 |

9.17 |

0.67 |

| Probable |

3.55 |

5.88 |

0.67 |

19.46 |

2.22 |

0.95 |

33.90 |

7.76 |

0.89 |

| Total P&P |

5.81 |

6.54 |

1.22 |

17.71 |

3.31 |

0.90 |

52.41 |

8.31 |

1.55 |

|

|

|

|

|

|

|

|

|

|

| Judd |

|

|

|

|

|

|

|

|

|

| Proven |

0.21 |

9.99 |

0.07 |

16.88 |

0.11 |

0.57 |

1.17 |

11.18 |

0.07 |

| Probable |

0.14 |

6.50 |

0.03 |

10.65 |

0.05 |

0.59 |

0.81 |

7.65 |

0.03 |

| Total P&P |

0.34 |

8.60 |

0.09 |

14.40 |

0.16 |

0.58 |

1.98 |

9.77 |

0.11 |

|

|

|

|

|

|

|

|

|

|

| Kora and Judd |

|

|

|

|

|

|

|

|

|

| Proven |

2.46 |

7.78 |

0.62 |

15.12 |

1.20 |

0.80 |

19.69 |

9.34 |

0.74 |

| Probable |

3.69 |

5.90 |

0.70 |

19.13 |

2.27 |

0.94 |

34.70 |

7.75 |

0.92 |

| Total P&P |

6.15 |

6.65 |

1.32 |

17.53 |

3.47 |

0.88 |

54.39 |

8.39 |

1.66 |

- The long-term metal prices used for calculating the financial analysis is US$1,600/oz gold, US$4.00/lb Copper, US$20/oz Silver.

- Gold Equivalents are calculated as AuEq = Au g/t + Cu % *1.7143 + Ag g/t*0.0125. Metal payabilities and recoveries are not incorporated into this formula.

- A minimum mining width of 3.0 m has been applied for stoping, inclusive of a 1.0 m dilution skin.

- In addition to the 1.0 m dilution skin, dilution of 5% has been added for Avoca mined stopes and 2.5% for long hole stoping with paste fill. This results in a total average dilution of 20%.

- Mining recoveries of 90% have been applied to Avoca mined stopes, and 95% for long hole stoping with paste fill.

- A cut-off grade of 3.0 g/t AuEq was used to define stoping blocks. Stope shapes with uneconomic development were excluded. The cut-off grade takes into account site operating costs, G&A costs, sustaining capital costs and relevant processing and revenue inputs.

- Measured Mineral Resources were used to report Proven Mineral Reserves.

- Indicated Mineral Resources were used to report Probable Mineral Reserves.

- Tonnage and grade estimates include dilution and recovery allowance.

- The Mineral Reserves reported are not added to Mineral Resources.

1.3 - Kainantu Mineral Resource Estimate

The Company’s current mineral resource estimate for Kora (effective date of October 31, 2021) and Judd (effective date of December 31, 2021) was completed by H & S Consultants Pty. Ltd. (Table 1.3). The Irumafimpa deposit was not incorporated into the IDP and will be reviewed at a later time.

Table 1.3 – Global Kora and Judd Mineral Resource Estimate for Kora and Judd, 1.75 g/t gold cut-off)

|

Tonnes |

Gold |

Silver |

Copper |

AuEq |

|

Mt |

g/t |

moz |

g/t |

moz |

% |

kt |

g/t |

moz |

| Kora |

|

|

|

|

|

|

|

|

|

| Measured |

2.8 |

9.07 |

0.8 |

15.7 |

1.4 |

0.85 |

24.1 |

10.51 |

1.0 |

| Indicated |

4.4 |

6.68 |

0.9 |

20.2 |

2.8 |

0.97 |

42.4 |

8.35 |

1.2 |

| Total M&I |

7.2 |

7.62 |

1.8 |

18.4 |

4.3 |

0.92 |

66.4 |

9.20 |

2.1 |

| Inferred |

8.1 |

7.12 |

1.8 |

27.3 |

7.1 |

1.38 |

111.1 |

9.48 |

2.5 |

|

|

|

|

|

|

|

|

|

|

| Judd |

|

|

|

|

|

|

|

|

|

| Measured |

0.22 |

11.26 |

0.08 |

19.9 |

0.14 |

0.72 |

1.59 |

12.56 |

0.09 |

| Indicated |

0.15 |

7.46 |

0.04 |

13.9 |

0.07 |

0.77 |

1.20 |

8.76 |

0.04 |

| Total M&I |

0.38 |

9.70 |

0.12 |

17.5 |

0.21 |

0.74 |

2.79 |

11.00 |

0.13 |

| Inferred |

1.01 |

4.24 |

0.14 |

11.0 |

0.36 |

0.87 |

8.82 |

5.66 |

0.18 |

|

|

|

|

|

|

|

|

|

|

| Kora and Judd |

|

|

|

|

|

|

|

|

|

| Measured |

3.1 |

9.23 |

0.9 |

16.0 |

1.6 |

0.84 |

25.7 |

10.66 |

1.0 |

| Indicated |

4.5 |

6.70 |

1.0 |

20.0 |

2.9 |

0.97 |

43.6 |

8.36 |

1.2 |

| Total M&I |

7.6 |

7.72 |

1.9 |

18.3 |

4.5 |

0.91 |

69.2 |

9.29 |

2.3 |

| Inferred |

9.1 |

6.80 |

2.0 |

25.5 |

7.4 |

1.32 |

119.9 |

9.05 |

2.6 |

- Estimates are from Technical Report titled, “Independent Technical Report, Mineral Resources Estimate Update Kora and Judd Gold Deposit, Kainantu Project, Papua New Guinea” dated January 20, 2022.

- The independent and Qualified Person responsible for the mineral resource estimate is Simon Tear, P.Geo. of H & S Consultants Pty. Ltd., Sydney, Australia. The effective date of the estimate for Kora is October 31, 2021 and the effective date of the Judd estimate is December 31, 2021.

- Mineral resources are not mineral reserves and do not have demonstrated economic viability.

- Resources were compiled at 1.75,2.5,3,4,5,6,7,8,9 and 10 g/t gold cut-off grades for Kora and 1.75,2.5,3,4,5 for Judd.

- Density (t/m3) is on a per zone basis, K1, K2: 2.84 t/m3; Kora Link: 2.74 t/m3; Judd: 2.71 t/m3; Waste: 2.67 t/m3.

- Minimun mining width for wireframes: Kora: 5.2 m; Judd: 5.2 m.

- Reported tonnage and grade figures are rounded from raw estimates to reflect the order of accuracy of the estimate.

- Minor variations may occur during the addition of rounded numbers.

- Estimations used metric units (metres, tonnes and g/t).

- Gold equivalents are calculated as AuEq = Au g/t + Cu%*1.607*92.8% + Ag g/t*0.0125*89%. Gold price US$1,600/oz; Silver US$20/oz; Copper US$3.75/lb. Metal payabilities and recoveries are incorporated into the AuEq formula. Recoveries of 92.8% for copper and 89% for silver.

1.4 - DFS Mining Operations

The Company engaged Entech to undertake the DFS for the Kainantu Project, which involved:

- Applying financial and processing parameters to determine cut-off grades for stope design.

- Generating three-dimensional stope shapes and mining inventory using the Datamine Mineable Shape Optimiser (MSO) program.

- Creating a conceptual development layout to suit the MSO inventory.

- Geotechnical assessment and generating the stoping parameters.

- Ventilation design and ventilation tradeoff studies.

- Mining capital and operating costings.

The Stage 3 Expansion mine plan considered in the DFS is designed as an incline access operation with a series of ore passes for efficient material movement between sublevels and the twin incline for material transport to surface. The DFS mine plan initially employs a long hole open stoping mining method utilizing Avoca and modified Avoca mining methods, which are currently employed at the mine. Upon construction of the paste fill plant, the mining method transitions to long hole open stoping with paste fill in Q2 2024.

Long hole open stoping has been successfully executed at both the Kora and Judd deposits, with the first long hole stope mined in Q1 2020 at Kora and Q4 2021 at Judd. The Avoca methods involve backfilling from the overcut sublevel while the long hole stope is advanced from the undercut sublevel to limit the strike length of the open stope. By limiting the strike length of the open stope, the method is designed to maintain stability of the stope walls and backs and increase the ultimate strike length extracted. The application of cemented paste fill provides improved geotechnical conditions for less dilution and higher mining recovery factors, greater operating flexibility through the ability to mine above and below paste fill and a reduction in surface tailings.

Stopes were identified for the mine plan contained in the DFS based on the Datamine Mineable Shape Optimiser (MSO) program at a cut-off grade of 3.0 g/t AuEq. Stope shapes with uneconomic development access requirements were excluded. Dilution was estimated based on a 0.5 m dilution skin for both the footwall and hanging wall using the MSO program for a minimum stope width of 3.0 m. An additional dilution factor of 5% for long hole stoping utilizing Avoca and modified Avoca and 2.5% for long hole open stoping with paste fill. The overall dilution averaged 20%. Mining recovery factors of 90% and 95% were applied for long hole open stoping with Avoca and long hole open stoping with paste fill, respectively. The life of mine average head grade is 6.65 g/t Au, 0.9 % Cu and 18 g/t Ag or 8.4 g/t AuEq.

The DFS Case ramps up to the Stage 2A 500,000-tonnes-per-annum throughput rate in late-2022 and continues to operate at that rate until early 2024, where the operation commences ramp up to the Stage 3 Expansion run-rate of 1.2 mtpa. Mining is predominately from the Kora Central Zone within the Kora deposit and the Judd deposit. See Table 1.6 for a material movement summary as part of the simplified economic model.

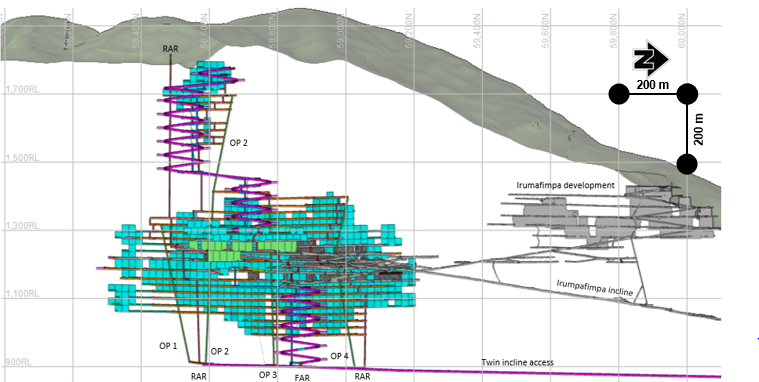

Figure 1.1 – DFS life of mine plan lateral, vertical development and stope shapes at 3.0 g/t AuEq cut-off grade (looking West)

https://www.globenewswire.com/NewsRoom/AttachmentNg/8ac17d1e-ffba-4dfd-923e-5fc5c9d305c4

1.4 - DFS Mineral Processing, Tailings and Infrastructure

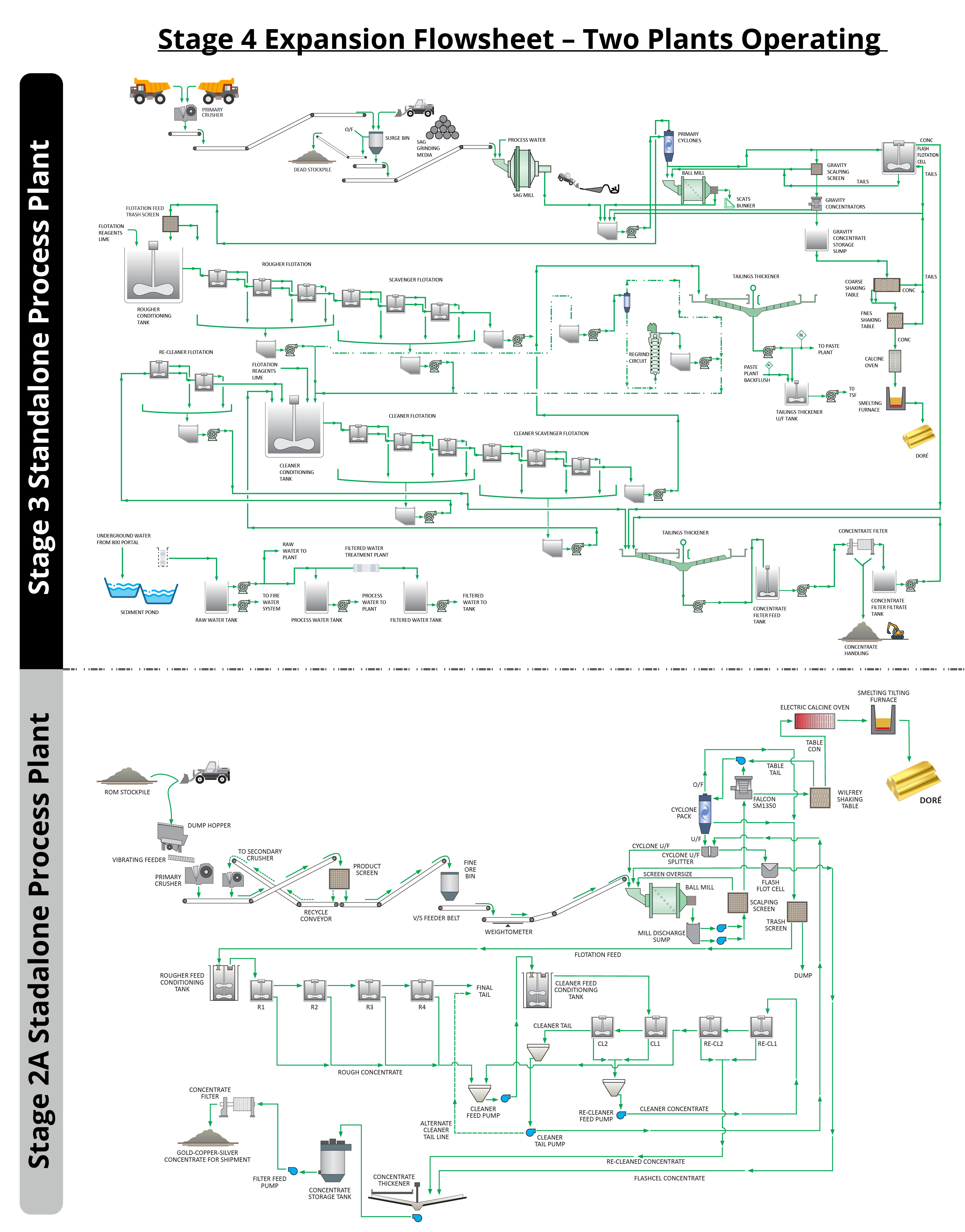

K92 engaged Lycopodium Minerals Pty Ltd to complete the DFS Stage 3 Expansion process plant and integration of surface infrastructure design. The DFS involves the construction of a standalone 1.2 mtpa processing plant and supporting infrastructure. The new plant is adjacent to the existing process plant, which is undergoing a Stage 2A Plant Expansion with a design throughput of 500,000 tpa. The existing plant will be placed on care and maintenance at the end of 2024 upon the ramp-up of the Stage 3 Process Plant commencing in Q3 2024.

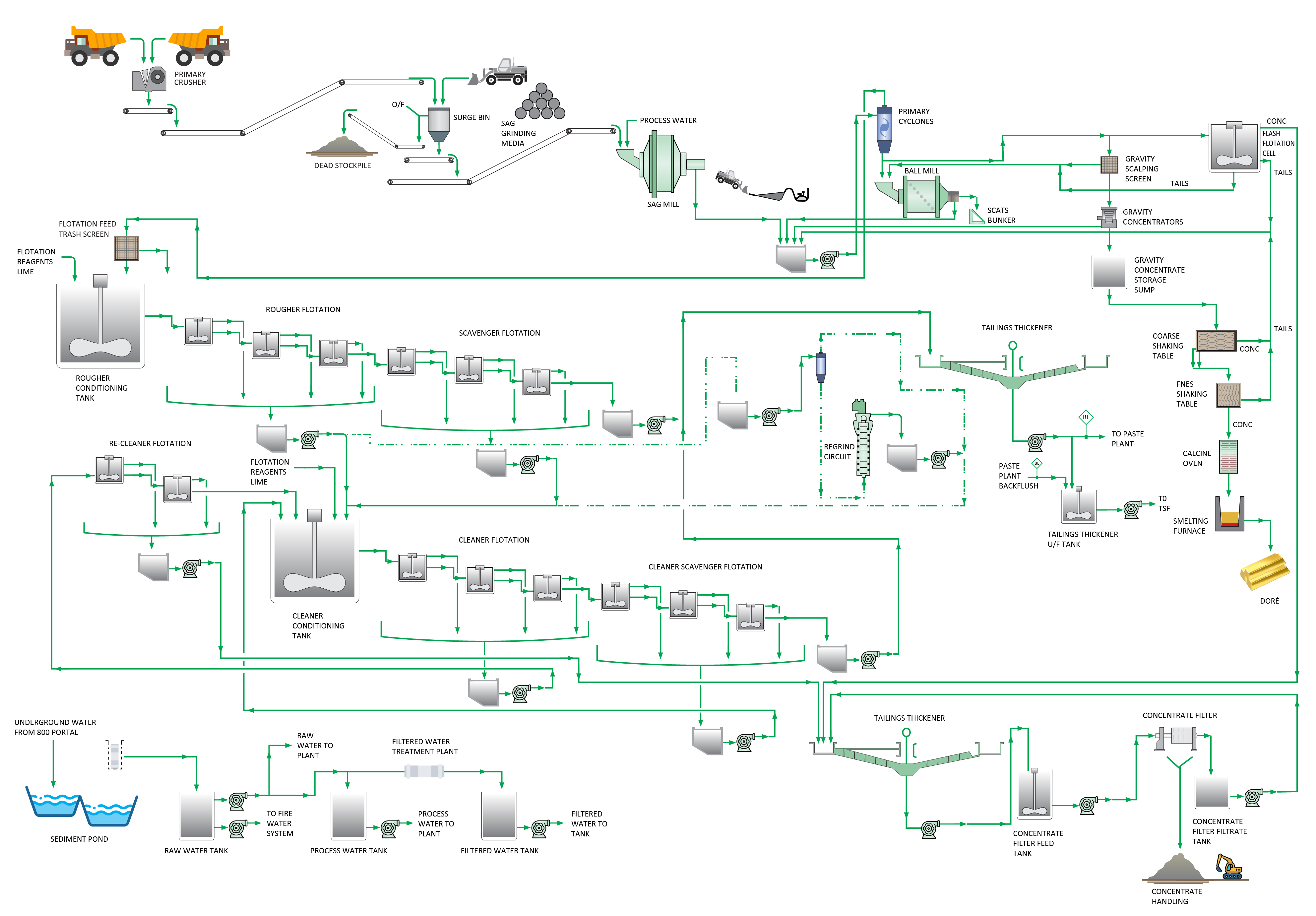

Run-of-mine (ROM) material is trucked ~6km from the 800 Portal to the Kainantu Process Plant, where it is either stockpiled or direct tipped. The 1.2 mtpa processing plant design flowsheet incorporates a conventional single stage jaw crushing (200tph) reporting to a crushed ore overflow surge bin and dead stockpile providing 16 hours of stockpile capacity. The primary crushed ore supplies a SAB milling circuit (150tph) that includes an open circuit SAG mill and closed circuit ball mill. The ball mill product reports to hydrocyclones, with cyclone overflow reporting to the flotation circuit and the cyclone underflow stream being split between the gravity circuit, flash flotation circuit and ball mill for grinding.

The gravity circuit involves one batch centrifugal concentrator followed by two stages of gravity separation using shaking tables to upgrade the gravity concentrate, which is then calcined and smelted to produce gold doré. The flotation circuit includes flash flotation and conventional sulphide flotation, followed by thickening and filtering to produce a gold-copper-silver concentrate. The circuit is based on simple conventional technology with the flowsheet largely similar but optimized from the existing Kainantu processing plant. The key difference between the existing plant and the proposed Stage 3 Expansion process plant is the implementation of a one stage crushing circuit (vs two stage crushing) and two stages of milling with a SAG and ball milling (vs one stage of ball milling).

Tailings management upgrades would be part of the Stage 3 Expansion, through the construction of a paste fill plant to provide improved underground support and mitigate surface tailings deposition. Thickened tailings at the process plant are designed to be pumped to the paste fill plant at the 800 Portal, with the final paste fill product pumped underground to void stopes for fill. Remaining thickened tailings report to the tailings impoundment on the surface. To support the increased processing capacity, implementation of the paste fill plant and increased underground mining activity, the standby diesel generator capacity is expanded. Additionally, the DFS involves an upgrade of the local electrical grid to facilitate improved availability and distribution of clean hydroelectricity to the mine. This is expected to considerably reduce the mine’s Scope 1 and Scope 2 greenhouse gas emission intensity per ounce produced - the amount of diesel fuel consumed for backup generators. K92 has already engaged with Papua New Guinea Power Limited (“PNG Power”) to commence this project and the Company expects it to have a notable improvement on our greenhouse gas emission intensity over the next 12 to 24 months.

The tailings storage facility (“TSF”) design was completed by ATC Williams. With the application of paste fill significantly reducing the amount of tailings reporting to surface, the current storage facility approval has sufficient capacity (constructed as staged development) for the DFS mine plan. The TSF is constructed as a downstream type, utilizing industry best standards and practices.

Figure 1.2 – DFS 1.2 mtpa Process Plant Flowsheet

https://www.globenewswire.com/NewsRoom/AttachmentNg/af4350e7-7338-4cac-8148-37ba30618cd6

1.6 - DFS Capital and Operating Costs

The initial capital cost estimate in the DFS includes contingency ranging from 10% to 20% depending on the capital item, with the major items outlined in Table 1.4. Operating costs are presented in terms of three categories: mining, processing and G&A per tonne processed. Processing costs also include costs related to the TSF and mining costs also include all paste fill costs.

Table 1.4: DFS - Capital Cost Estimates

| US Dollars unless otherwise stated |

|

| Process Plant |

$80.2m |

| Power Station |

$9.6m |

| Power Supply |

$13.8m |

| Camp Upgrade |

$5.5m |

| EPCM |

$20.4m |

| Owner’s Cost |

$4.2m |

| Other Infrastructure |

$3.7m |

| Paste Plant |

$39.9m |

| Initial Pre-Expansion Capital |

$177.3m |

|

|

| Total Life of Mine Sustaining Capital |

$218.4m |

Totals may differ due to rounding

Table 1.5: DFS - Operating Cost Estimates (Life of Mine Average)

| US Dollars unless otherwise stated |

|

| Mining Cost ($/t) |

$66.54 |

| Processing Cost ($/t) |

$17.36 |

| General & Administrative Cost ($/t) |

$32.43 |

| Total Cost Per Tonne Processed ($/t) |

$116.34 |

| Sustaining Capital per Tonne of Processed ($/t) |

$35.50 |

| Total Cost Per Tonne Processed ($/t) |

$151.83 |

Totals may differ due to rounding

1.7 DFS – Economic Analysis

Lycopodium prepared a pre-tax conceptual cashflow and discounted cashflow derived from the life of mine schedule. Tax calculations for the after-tax cashflow and discounted cashflow were prepared by K92. A summary of the cashflow analyses is shown in Table 1.6 and a sensitivity analysis to gold price is shown in Table 1.7.

Table 1.6: DFS - Simplified Financial Model at US$1,600/oz Au, US$4.00/lb Cu, US$20.00/oz Ag

| Year |

2022 |

2023 |

2024 |

2025 |

2026 |

2027 |

2028 |

|

|

|

|

|

|

|

|

| Mill Throughput (ktpa) |

435 |

500 |

850 |

1,200 |

1,200 |

1,200 |

768 |

|

|

|

|

|

|

|

|

| Gold Grade |

9.06 |

8.65 |

7.00 |

6.45 |

6.60 |

5.71 |

5.48 |

| Copper Grade |

0.56% |

0.64% |

0.75% |

0.91% |

1.02% |

0.89% |

1.12% |

| Silver Grade |

11.47 |

12.85 |

14.45 |

17.77 |

19.93 |

18.08 |

22.41 |

| AuEq Grade |

10.16 |

9.91 |

8.45 |

8.24 |

8.60 |

7.46 |

7.67 |

|

|

|

|

|

|

|

|

| Gold Production (000s oz) |

118 |

129 |

178 |

231 |

237 |

205 |

126 |

| Copper Production (m lbs) |

5.1 |

6.7 |

13.3 |

23.0 |

25.7 |

22.4 |

18.0 |

| Silver Production (000s oz) |

128 |

165 |

316 |

548 |

615 |

558 |

442 |

| AuEq Production (000s oz) |

132 |

147 |

212 |

291 |

303 |

263 |

172 |

|

|

|

|

|

|

|

|

| Net Revenue (US$m)(1) |

$195 |

$218 |

$311 |

$421 |

$438 |

$379 |

$245 |

| Total OPEX (US$m)(1) |

$63 |

$73 |

$112 |

$130 |

$128 |

$123 |

$87 |

| Growth Capital (US$m) |

- |

$71 |

$106 |

- |

- |

- |

- |

| Sustaining Capital (US$m) |

$46 |

$54 |

$42 |

$31 |

$27 |

$11 |

$7 |

|

|

|

|

|

|

|

|

| Pre-Tax Net Cashflow (US$m) |

$81m |

$14m |

$43m |

$249m |

$271m |

$236m |

$145m |

| After-tax Net Cashflow (US$m) |

$47m |

($14m) |

$11m |

$192m |

$208m |

$181m |

$109m |

| Cumulative After-tax Net Cashflow (US$m) |

$47m |

$34m |

$44m |

$237m |

$445m |

$625m |

$734m |

- Net revenue in summary model excludes the impact of royalty payments.

Table 1.7: DFS - After-Tax NPV5% Sensitivity to Gold Price

| Gold Price |

After-Tax NPV5% (US$M) |

| $1,400 |

$451 |

| $1,600 |

$586 |

| $1,800 |

$721 |

| $2.000 |

$855 |

| $2,200 |

$990 |

| $2,400 |

$1,125 |

2 - Kainantu IDP - Preliminary Economic Assessment Case

2.1 – PEA Overview

The alternative PEA Case conceptualizes a multi-expansion plan to an ultimate plant run-rate of 1.7 mtpa, representing a 240% increase from the Stage 2A run-rate of 500,000 tpa. The PEA Case involves the construction of a standalone 1.2 mtpa process plant adjacent to the 500,000 tpa Stage 2A process plant. At the end of 2024, the Stage 2A process plant is idled as the 1.2 mtpa Stage 3 process plant ramps up, with commissioning of the Stage 3 process plant commencing in Q3 2024. Upon achieving the Stage 3 run-rate throughput in 2025, the Stage 2A plant is recommissioned in mid-2026, ramping up to run-rate throughput of 500,000 tpa by year end, for a combined processing run-rate of 1.7 mtpa at the beginning of 2027.

To support the higher throughput rate, the underground mining fleet is significantly increased to support expanded mining operations opening up multiple mining fronts concurrently: Kora Upper, Lower and Central Zones within the Kora deposit, and the Judd deposit. Site infrastructure is also expanded, including power, camp facilities and the paste fill plant. Several capital items, such as the paste fill system, are configured during the construction of Stage 3 to be amenable to the larger ultimate Stage 4 run-rate.

The PEA uses the conclusions of the Company’s mineral resource estimate for Kora (effective date of October 31, 2021) and Judd (effective date of December 31, 2021) and does not incorporate post resource drilling results. The effective date of the PEA life of mine plan is January 1, 2022; therefore, Kora is net of post-resource mining depletion from November 1, 2021 to December 31, 2021 which totals 36,765 tonnes at 12.94 g/t Au, 0.59% Cu and 9.29 g/t Ag.

The PEA is preliminary in nature and includes inferred mineral resources that are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorized as mineral reserves, and there is no certainty that the PEA will be realized. Mineral resources that are not mineral reserves do not have demonstrated economic viability.

Table 2.1: PEA Highlights

| US Dollars unless otherwise stated |

Life of Mine

(starting January 2022) |

Stage 4 Expansion

(3Q 2026 onwards) |

| Production |

|

|

| Mine life (years) |

11 years |

|

| Total mill feed (000s tonnes) |

12,156 |

|

| Average mill throughput (tonnes per annum) |

1,105 ktpa |

1.7 Mtpa (run-rate)(1) |

|

|

|

| Total Metal Production |

|

|

| AuEq (000s ounces) |

3,398 |

2,134(2) |

| Gold (000s ounces) |

2,555 |

1,579(2) |

| Copper (mlbs) |

302 |

198(2) |

| Silver (000s ounces) |

7,040 |

4,726(2) |

|

|

|

| Peak Annual Production |

|

|

| Year |

|

2027 |

| AuEq (000s ounces per annum) |

|

500 |

|

|

|

| Average Annual Metal Production |

|

|

| AuEq (000s ounces per annum) |

309 |

406 (run-rate)(1) |

| Gold (000s ounces per annum) |

232 |

297 (run-rate)(1) |

| Copper (mlbs per annum) |

27 |

39 (run-rate)(1) |

| Silver (000s ounces per annum) |

640 |

928 (run-rate)(1) |

|

|

|

| Average Grade |

|

|

| AuEq grade (g/t) |

9.3 g/t |

|

| Gold grade (g/t) |

7.0 g/t |

|

| Copper grade (%) |

1.2% |

|

| Silver grade (g/t) |

23 g/t |

|

|

|

|

| Average Recovery |

|

|

| Gold Recovery (%) |

93% |

|

| Copper Recovery (%) |

95% |

|

| Silver Recovery (%) |

80% |

|

|

|

|

| Costs |

|

|

| Mining cost per tonne (US$/t) |

$72.05 |

$65.43 (run-rate)(1) |

| Processing cost per tonne (US$/t) |

$18.02 |

$17.65 (run-rate)(1) |

| G&A cost per tonne (US$/t) |

$28.19 |

$25.89 (run-rate)(1) |

| Total operating cost per tonne of mill feed (US$/t) |

$118.26 |

$108.97 (run-rate)(1) |

| Sustaining capital per tonne of mill feed (US$/t) |

$35.33 |

$20.79 (run-rate)(1) |

| Total cost per tonne of mill feed (US$/t) |

$153.59 |

$129.76 (run-rate)(1) |

|

|

|

| Expansion capital expenditure ($m) |

$187 |

|

| Sustaining capital expenditure ($m) |

$429 |

|

| Total capital expenditure with closure costs ($m) |

$628 |

|

|

|

|

| Cash cost per ounce AuEq ($/oz)(3) |

$546 |

$527 (run-rate)(1) |

| All-in sustaining cost per ounce AuEq ($/oz)(4) |

$674 |

$604 (run-rate)(1) |

| Cash cost per ounce gold ($/oz)(3) |

$275 |

$220 (run-rate)(1) |

| All-in sustaining cost per ounce gold ($/oz)(4) |

$444 |

$325 (run-rate)(1) |

|

|

|

| Base Case Economic Analysis at US$1,600/oz Gold, US$4.00/lb Copper and US$20.00/oz Silver |

| After-tax NPV0% |

$1.8 billion |

|

| After-tax NPV5% |

$1.3 billion |

|

| IRR (%) and Payback Period (years) |

N/A (Self-Funded) |

|

|

|

|

| Economic Analysis at $2,000/oz Gold, US$4.00/lb Copper and US$20.00/oz Silver |

| After-tax NPV0% |

$2.5 billion |

|

| After-tax NPV5%(5) |

$1.8 billion |

|

| IRR (%) and Payback Period (years) |

N/A (Self-Funded) |

|

- Run-rate excludes the final partial calendar year of production.

- Excludes 2H 2026 Stage 4 commissioning and initial ramp-up stage.

- Cash costs are net of by-product credits and are inclusive of mining costs, processing costs, site G&A and refining charges and royalties.

- AISC includes cash costs plus estimated corporate G&A, sustaining costs and accretion.

- Net present value is calculated utilizing mid-year discounting.

2.2 - PEA Mining Operations

The Company engaged Entech to undertake the PEA Case for the Kainantu Project, which involved:

- Applying financial and processing parameters to determine cut-off grades for stope design.

- Generating three-dimensional stope shapes and mining inventory using the Datamine Mineable Shape Optimiser (MSO) program.

- Creating a conceptual development layout to suit the MSO inventory.

- Geotechnical assessment and generating the stoping parameters.

- Ventilation design and ventilation tradeoff studies.

- Mining capital and operating costings.

The mine plan considered in the PEA is designed as an incline access operation with a series of ore passes for efficient material movement between sublevels and the twin incline for material transport to surface. Initially, the mine plan employs a long hole open stoping mining method utilizing Avoca and modified Avoca, with waste rockfill. This mining method has been successfully employed at the mine since Q1 2020 at Kora and Q4 2021 at Judd. The mining method will then transition to long hole open stoping with paste fill in Q2 2024, upon the construction of the paste fill plant. Cemented paste fill provides improved geotechnical conditions for less dilution, higher mining recovery factors, and greater operating flexibility through the ability to mine above and below paste fill, plus a reduction in surface tailings.

Stopes were identified for the PEA mine plan based on the MSO program at a cut-off grade of 4.5 g/t AuEq. Stope shapes with uneconomic development access requirements were excluded from the assessment. Dilution was estimated based on a 0.5 m dilution skin for both the footwall and hanging wall using the MSO program for a minimum stope width of 3.0 m. An additional dilution factor of 5% for long hole stoping utilizing Avoca and modified Avoca and 2.5% for long hole open stoping with paste fill. Dilution overall averaged 24%. Mining recovery factors of 90% and 95% were applied for long hole open stoping with Avoca and long hole open stoping with paste fill, respectively. The life of mine average head grade is 7.0 g/t Au, 1.2% Cu and 23 g/t Ag or 9.3 g/t AuEq.

The mine plan ramps up to the Stage 2A 500,000-tpa throughput rate in late-2022 and continues to operate at that rate until the end of 2024, with the operation commencing ramp up to the Stage 3 Expansion run-rate of 1.2 mtpa, sequentially ramping-up to the Stage 4 Expansion run-rate of 1.7 mtpa at the beginning of 2027. To support the Stage 4 mining rate, multiple mining fronts are mined concurrently: Kora Central, Kora Upper and Kora Lower within the Kora deposit, and the Judd deposit. See Table 2.6 for a material movement summary as part of the simplified economic model.

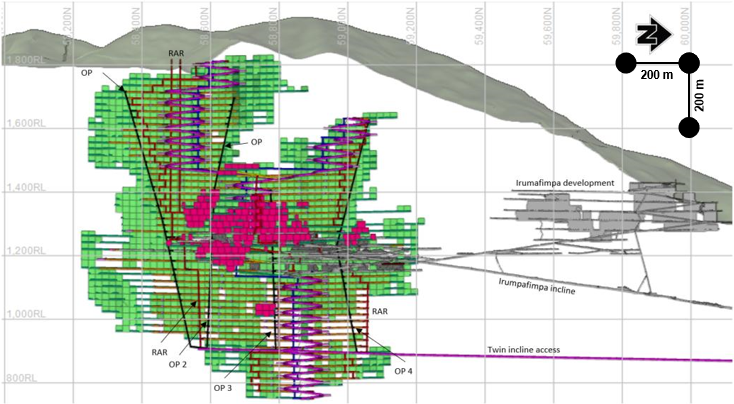

Figure 2.1 – PEA life of mine plan lateral, vertical development and stope shapes at 4.5 g/t AuEq cut-off grade (looking West)

https://www.globenewswire.com/NewsRoom/AttachmentNg/e52567a3-a374-4f5f-91f8-0c7615cab82c

2.4 - PEA Mineral Processing, Tailings and Infrastructure

K92 engaged Lycopodium to complete the PEA Stage 4 Expansion process plant and surface infrastructure design. The PEA conceptualizes constructing a new standalone processing plant for the Stage 3 Expansion adjacent to the existing Stage 2A Expansion process plant. The existing Stage 2A process plant operates until the end of 2024, where it is idled as the Stage 3 Expansion ramps-up (starting in Q3 2024). The process plants are fed from run-of-mine (ROM) material that is trucked ~6km from the 800 Portal to the Kainantu process plant, where it is either stockpiled or direct tipped.

The Stage 3 Expansion process plant design flowsheet incorporates a conventional comminution circuit, utilizing a single stage of jaw crushing (200 tph) reporting to a crushed ore overflow surge bin, followed by a SAB milling circuit (150 tph) with an open circuit SAG mill and close circuit ball mill. The ball mill product reports to cyclone classification, where the cyclone overflow reports to the flotation circuit and the cyclone underflow stream being split between the gravity circuit, flash flotation circuit and ball mill for grinding. The gravity circuit involves one batch centrifugal concentrator followed by two stages of gravity separation using shaking tables. The upgraded gravity concentrate is then calcined and smelted to produce gold doré. The flotation circuit consists of flash flotation and conventional sulphide flotation, followed by thickening and filtering to produce a gold-copper-silver concentrate.

The PEA incorporates tailings management upgrades, with underground paste fill commencing in Q2 2024 on the completion of construction of the paste fill plant. The delivery of paste fill involves pumping thickened tailings from the process plant to the paste fill plant at the 800 Portal, followed by pumping the final paste fill product underground to void stopes. Remaining tailings are pumped to the tailings impoundment. The significant increase to processing capacity, mining rates and underground infrastructure requires additions to the standby diesel generating capacity on site. The PEA also involves an upgrade to the local electrical grid to facilitate improved availability and distribution of clean hydroelectricity to the mine. This upgrade is expected to materially reduce Scope 1 and Scope 2 greenhouse gas emission intensity per ounce produced.

The implementation of paste fill significantly reduces the amount of tailings reporting to the TSF. The existing TSF has sufficient tailings capacity until 2027, where tailings then report to the new TSF. The development of the new tailings facility is adjacent to the existing TSF with a number of suitable sites identified. The new tailings facility design has significant capacity beyond the material movements in the PEA. The existing and new TSF design is downstream type, utilizing industry best practices and standards. The TSF design work was completed by ATC Williams.

Figure 2.2 – PEA 1.7 mtpa Process Plant Flowsheet

https://www.globenewswire.com/NewsRoom/AttachmentNg/31c46c2a-91f9-42d9-9c07-768395468e3e

2.5 - PEA Capital and Operating Costs

The initial capital cost estimate includes a contingency ranging from 10% to 20% and the major items are outlined in Table 2.4. Operating costs are presented in terms of three categories: mining, processing and G&A per tonne processed. Processing costs also include costs related to the TSF and mining costs also include all paste fill costs.

Table 2.4: PEA - Capital Cost Estimates

| US Dollars unless otherwise stated |

|

| Process Plant |

$80.2m |

| Power Station |

$12.5m |

| Power Supply |

$13.8m |

| Camp Upgrade |

$7.3m |

| EPCM |

$20.4m |

| Owner’s Cost |

$4.2m |

| Other Infrastructure |

$3.7m |

| Paste Plant |

$45.0m |

| Initial Pre-Expansion Capital |

$187.1m |

|

|

| Total Life of Mine Sustaining Capital |

$429.4m |

Totals may differ due to rounding

Table 2.5: PEA - Operating Cost Estimates (Life of Mine Average)

| US Dollars unless otherwise stated |

|

| Mining Cost ($/t) |

$72.05 |

| Processing Cost ($/t) |

$18.02 |

| General & Administrative Cost ($/t) |

$28.19 |

| Total Cost Per Tonne Processed ($/t) |

$118.26 |

| Sustaining Capital per Tonne of Processed ($/t) |

$35.53 |

| Total Cost Per Tonne Processed ($/t) |

$153.59 |

Totals may differ due to rounding

2.6 PEA - Economic Analysis

Lycopodium prepared a pre-tax conceptual cashflow and discounted cashflow derived from the life of mine schedule. Tax calculations for the after-tax cashflow and discounted cashflow were prepared by K92. A summary is shown in Table 2.6 and a sensitivity analysis to gold price is shown in Table 2.7.

Table 2.6: PEA - Simplified Financial Model at US$1,600/oz Au, US$4.00/lb Cu, US$20.00/oz Ag

| Year |

2022 |

2023 |

2024 |

2025 |

2026 |

2027 |

2028 |

2029 |

2030 |

2031 |

2032 |

|

|

|

|

|

|

|

|

|

|

|

|

| Mill Throughput (ktpa) |

435 |

500 |

850 |

1,200 |

1,500 |

1,700 |

1,700 |

1,700 |

1,502 |

845 |

224 |

|

|

|

|

|

|

|

|

|

|

|

|

| Gold Grade |

9.50 |

8.08 |

6.62 |

6.51 |

7.36 |

7.89 |

6.45 |

6.61 |

5.45 |

6.94 |

14.02 |

| Copper Grade |

0.76% |

0.82% |

1.18% |

1.28% |

1.09% |

1.00% |

1.12% |

1.33% |

1.52% |

1.28% |

0.94% |

| Silver Grade |

14.42 |

14.98 |

22.52 |

23.28 |

19.43 |

17.79 |

22.59 |

26.43 |

30.86 |

24.18 |

15.13 |

| AuEq Grade |

10.99 |

9.66 |

8.92 |

9.00 |

9.48 |

9.83 |

8.66 |

9.22 |

8.45 |

9.44 |

15.83 |

|

|

|

|

|

|

|

|

|

|

|

|

| Gold Production (000s oz) |

124 |

121 |

168 |

234 |

330 |

401 |

328 |

336 |

245 |

175 |

94 |

| Copper Production (m lbs) |

7 |

9 |

21 |

32 |

34 |

36 |

40 |

47 |

48 |

23 |

4 |

| Silver Production (000s oz) |

161 |

193 |

492 |

719 |

750 |

778 |

988 |

1,156 |

1,192 |

525 |

87 |

| AuEq Production (000s oz) |

143 |

145 |

227 |

323 |

425 |

500 |

441 |

469 |

380 |

239 |

106 |

|

|

|

|

|

|

|

|

|

|

|

|

| Net Revenue (US$m)(1) |

$210 |

$210 |

$319 |

$451 |

$604 |

$717 |

$619 |

$653 |

$515 |

$334 |

$156 |

| Total OPEX (US$m)(1) |

$77 |

$90 |

$122 |

$142 |

$163 |

$184 |

$187 |

$180 |

$154 |

$101 |

$37 |

| Growth Capital (US$m) |

- |

$75 |

$110 |

$3 |

$1 |

- |

- |

- |

- |

- |

- |

| Sustaining Capital (US$m) |

$46 |

$56 |

$59 |

$49 |

$61 |

$62 |

$38 |

$32 |

$17 |

$6 |

$3 |

|

|

|

|

|

|

|

|

|

|

|

|

| Pre-Tax Net Cashflow (US$m) |

$82m |

($17m) |

$19m |

$247m |

$364m |

$453m |

$379m |

$425m |

$330m |

$218m |

$102m |

| After-tax Net Cashflow (US$m) |

$48m |

($37m) |

($10m) |

$188m |

$268m |

$325m |

$270m |

$303m |

$231m |

$153m |

$71m |

| Cumulative After-tax Net Cashflow (US$m) |

$48m |

$11m |

$1m |

$189m |

$457m |

$783m |

$1,053m |

$1,356m |

$1,587m |

$1,740m |

$1,811m |

- Net revenue in summary model excludes the impact of royalty payments.

Table 2.7: PEA - After-Tax NPV5% Sensitivity to Gold Price

| Gold Price |

After-Tax NPV5% (US$B) |

| $1,400 |

$1.1 |

| $1,600 |

$1.3 |

| $1,800 |

$1.6 |

| $2.000 |

$1.8 |

| $2,200 |

$2.1 |

| $2,400 |

$2.3 |

Diamond Drill and Face Sampling Methodology, Data Verification and QA / QC

Diamond drill hole is first logged to determine the sampling intervals, which range from a minimum of 0.1 metres to generally 1 metre. The drill core is sawn half core cut along a reference line, with the remainder of the core returned to the core tray. Core samples are then placed in numbered calico and plastic bags, with a numbered sample ticket for dispatch to the assay laboratory. Samples are separately assayed for gold, copper and silver. K92’s procedure includes the insertion standards, blanks and duplicates. Gold assays are by the fire assay method. Copper and silver assays are by three-acid-digestion method (nitric, perchloric & hydrochloric mix).

Face channel samples under geological control, were taken across the full face of both the exposed lode system and any waste rock, with sample intervals ranging from 0.1 to 1m in width depending on the geologist’s interpretation. Two samples were taken per interval at waist and knee height and the corresponding widths recorded. Sample lengths are <1.5m, with samples approximately 3.5 kg in size. Samples were separately assayed for gold, copper and silver, and the results averaged out using length weighting and channel orientation before entry into the database. K92’s procedure includes the insertion standards, blanks and duplicates for the face sampling. Gold assays are by the fire assay method. Copper and silver assays are by three-acid-digestion method (nitric, perchloric & hydrochloric mix).

K92 maintains an industry-standard analytical quality assurance and quality control (QA/QC) and data verification program to monitor laboratory performance and ensure high quality assays. Results from this program confirm reliability of the assay results. All sampling and analytical work for the mine exploration program is performed by Intertek Testing Services (PNG) LTD, an independent accredited laboratory that is located on site. External check assays for QA/QC purposes are performed at SGS Australia Pty Ltd in Townsville, Queensland, Australia.

The analytical QA/QC program is currently overseen by Andrew Kohler, PGeo, Mine Geology Manager and Mine Exploration Manager for K92. Andrew Kohler, a qualified person under the meaning of Canadian National Instrument 43-101 – Standards of Disclosure for Mineral Projects.

Qualified Person

K92 Mine Geology Manager and Mine Exploration Manager, Mr. Andrew Kohler, PGeo, a Qualified Person under the meaning of NI 43-101 has reviewed and approved the technical content of this news release. The Company strictly adheres to CIM Best Practices Guidelines in conducting, documenting, and reporting the exploration activities on its projects.

Simon Tear, P.Geo of H & S Consultants Pty. Ltd. of Sydney, Australia is a Qualified Person as defined under NI 43-101 and has reviewed and approved the contents of this press release. Mr. Tear is an independent consultant and is responsible for the 2022 Mineral Resource Estimate for Kora and Judd.

Patrick McCann, P.Eng of Entech Mining Limited of Toronto, Canada is a Qualified Person as defined under NI 43-101 and has reviewed and approved the contents of this press release. Mr. McCann is an independent consultant and is responsible for mine planning and mine design. Mr. McCann completed a site visit from October 14th to 21st 2021.

Shane McLeay, FAusIMM of Entech Pty Ltd of Perth, Australia is a Qualified Person as defined under NI 43-101 and has reviewed and approved the contents of this press release. Mr. McLeay is an independent consultant and is responsible for mine planning and mine design.

Sandra (Sandy) Hunter, FAusIMM(CP) of Lycopodium Minerals Pty Ltd of Brisbane, Australia is a Qualified Person as defined under NI 43-101 and has reviewed and approved the contents of this press release. Ms. Hunter is an independent consultant responsible for the process plant and integration of surface infrastructure design.

Matt Helinski, P.Eng of MineFill Services Pty Ltd of Newcastle, Australia is a Qualified Person as defined under NI 43-101 and has reviewed and approved the contents of this press release. Mr. Helinski is an independent consultant and is responsible for the paste fill delivery and paste fill plant design.

Ralph Holding, FIEAust CPEng of ATC Williams Pty Ltd of Brisbane, Australia is a Qualified Person as defined under NI 43-101 and has reviewed and approved the contents of this press release. Mr. Holding is an independent consultant and is responsible for the tailing storage facility design.

On Behalf of the Company,

John Lewins, Chief Executive Officer and Director

For further information, please contact David Medilek, P.Eng., CFA at +1-604-416-4445.

About K92

K92 Mining Inc. is engaged in the production of gold, copper and silver at the Kainantu Gold Mine in the Eastern Highlands province of Papua New Guinea, as well as exploration and development of mineral deposits in the immediate vicinity of the mine. The Company declared commercial production from Kainantu in February 2018, is in a strong financial position. K92 is operated by a team of mining company professionals with extensive international mine-building and operational experience.

Non-GAAP Financial Measures

In this press release, we use the terms “cash costs" and "all-in sustaining costs ". These should be considered as non-GAAP financial measures as defined in applicable Canadian securities laws and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with GAAP.

Cash costs per ounce is a non-GAAP term typically used by gold mining companies to assess the level of gross margin available to the Company by subtracting these costs from the unit price realized during the period. This non-GAAP term is also used to assess the ability of a mining company to generate cash flow from operations. Cash costs per ounce includes mining and processing costs plus applicable royalties, and net of by-product revenue and net realizable value adjustments. Total cash costs per ounce is exclusive of exploration costs.

Cash costs per ounce is intended to provide additional information only and does not have any standardized meaning under IFRS and may not be comparable to similar measures presented by other mining companies. It should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. The measure is not necessarily indicative of cash flow from operations under IFRS or operating costs presented under IFRS.

The Company adopted an "all-in sustaining costs per ounce" non-GAAP performance measure in accordance with the World Gold Council published in June 2013. The Company believes the measure more fully defines the total costs associated with producing gold; however, this performance measure has no standardized meaning. Accordingly, there may be some variation in the method of computation of "all-in sustaining costs " as determined by the Company compared with other mining companies. In this context, "all-in sustaining costs" for the consolidated Company reflects total mining and processing costs, corporate and administrative costs, exploration costs, sustaining capital, and other operating costs.

All-in sustaining costs per gold ounce is intended to provide additional information only and does not have any standardized meaning under IFRS and may not be comparable to similar measures presented by other mining companies. It should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS.

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING INFORMATION: This news release includes certain “forward-looking statements” under applicable Canadian securities legislation. Such forward-looking statements include, without limitation: (i) the results of the Kainantu Project DFS, and the Kainantu 2022 PEA, including the Stage 3 Expansion, a new standalone 1.2 mtpa process plant and supporting infrastructure; (ii) statements regarding the expansion of the mine and development of any of the deposits; and (iii) the Kainantu Stage 4 Expansion, operating two standalone process plants, larger surface infrastructure and mining throughputs.

All statements in this news release that address events or developments that we expect to occur in the future are forward-looking statements. Forward-looking statements are statements that are not historical facts and are generally, although not always, identified by words such as “expect”, “plan”, “anticipate”, “project”, “target”, “potential”, “schedule”, “forecast”, “budget”, “estimate”, “intend” or “believe” and similar expressions or their negative connotations, or that events or conditions “will”, “would”, “may”, “could”, “should” or “might” occur. All such forward-looking statements are based on the opinions and estimates of management as of the date such statements are made. Forward-looking statements are necessarily based on estimates and assumptions that are inherently subject to known and unknown risks, uncertainties and other factors, many of which are beyond our ability to control, that may cause our actual results, level of activity, performance or achievements to be materially different from those expressed or implied by such forward-looking information. Such factors include, without limitation, Public Health Crises, including the COVID-19 Pandemic; changes in the price of gold, silver, copper and other metals in the world markets; fluctuations in the price and availability of infrastructure and energy and other commodities; fluctuations in foreign currency exchange rates; volatility in price of our common shares; inherent risks associated with the mining industry, including problems related to weather and climate in remote areas in which certain of the Company’s operations are located; failure to achieve production, cost and other estimates; risks and uncertainties associated with exploration and development; uncertainties relating to estimates of mineral resources including uncertainty that mineral resources may never be converted into mineral reserves; the Company’s ability to carry on current and future operations, including development and exploration activities; the timing, extent, duration and economic viability of such operations, including any mineral resources or reserves identified thereby; the accuracy and reliability of estimates, projections, forecasts, studies and assessments; the Company’s ability to meet or achieve estimates, projections and forecasts; the availability and cost of inputs; the price and market for outputs, including gold, silver and copper; inability of the Company to identify appropriate acquisition targets or complete desirable acquisitions; failures of information systems or information security threats; political, economic and other risks associated with the Company’s foreign operations; geopolitical events and other uncertainties, such as the conflict in Ukraine; compliance with various laws and regulatory requirements to which the Company is subject to, including taxation; the ability to obtain timely financing on reasonable terms when required; the current and future social, economic and political conditions, including relationship with the communities in jurisdictions it operates; other assumptions and factors generally associated with the mining industry; and the risks, uncertainties and other factors referred to in the Company’s Annual Information Form under the heading “Risk Factors”.

Estimates of mineral resources are also forward-looking statements because they constitute projections, based on certain estimates and assumptions, regarding the amount of minerals that may be encountered in the future and/or the anticipated economics of production. The estimation of mineral resources and mineral reserves is inherently uncertain and involves subjective judgments about many relevant factors. Mineral resources that are not mineral reserves do not have demonstrated economic viability. The accuracy of any such estimates is a function of the quantity and quality of available data, and of the assumptions made and judgments used in engineering and geological interpretation, Forward-looking statements are not a guarantee of future performance, and actual results and future events could materially differ from those anticipated in such statements. Although we have attempted to identify important factors that could cause actual results to differ materially from those contained in the forward-looking statements, there may be other factors that cause actual results to differ materially from those that are anticipated, estimated, or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements. The Company disclaims any intention or obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.