Sales and cash spend fall before the usual Christmas upturn, although inflation means spending higher than the same period in 2022

The FICO UK Credit Card Market Report for October 2023 reflects the typical trend of lower spend before the Christmas rush, although average balances continued their upward trajectory year-on-year. The financial pressures facing many UK households are also evidenced in falling monthly and annual payments to balance.

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20231214091277/en/

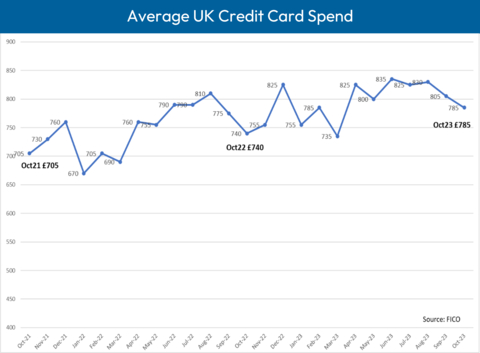

Spending on UK credit cards fell in October by 3% month-on-month although it remains higher than October 2022, probably due at least in part to higher prices. (Graphic: FICO)

Highlights

- Sales dropped 3% from September, but are still 6% higher than October 2022

- Average balances fell slightly month-on-month, down 0.4%, but remain 9.8% higher than the previous year

- Once again the percentage of payments to balance fell, now standing at 37.8%

- Customers missing one payment decreased month-on-month by 4.3%

- The number of customers missing two payments rose by 8%.

- The average balance where one payment has been missed continued on an upward trend, rising 1% from September and 5.5% year-on-year, now standing at £2,180

FICO Comment

It is common to see a dip in spending in the autumn, ahead of higher spending in the run-up to and during the festive season. This year, spending in October fell by 3% month-on-month although it remains higher than October 2022, probably due at least in part to higher prices.

Looking at outstanding balances, while the average card balance decreased 0.4% month-on-month, the balance for customers who have missed payments is trending upwards and the percentage of payments to balance has decreased for four months in a row.

37.8% of balances were paid in October, a reduction of 0.7% month-on-month and 6.8% year-on-year. 2022 saw a similar reduction, before increased payments in January 2023, however it is likely this figure will continue to fall over the next couple of months due to continued financial hardship and increased spend over the festive period.

The number of customers missing one payment decreased by 4.3% from September to October, which was expected after the 13.5% increase seen in September. The September increase has rolled forwards and subsequently there has been a larger increase in customers now missing two payments in October — an 8% increase month-on-month. Customers missing three payments have experienced more stability, dropping by just 0.4% on the previous month. However, the number of customers missing one, two or three payments remains significantly higher year-on-year.

The average balance for customers missing payments has continued to trend upwards during 2023, with the average balance for one missed payment increasing 1% month-on-month to £2,180 and 5.5% year-on-year. A similar pattern is seen for the average balance for three missed payments, increasing 0.4% month-on-month to £2,950 — a 2.4% increase year-on-year. However, customers missing two payments have seen their average balance reduce by 0.7% to £2,585, although this is still 1.3% higher than the same month in 2022.

Although the average missed payment balance has been increasing throughout much of 2023, when comparing the ratio of missed payment balances to the overall credit card balance, this has been fairly stable. This suggests missed payment balances have not increased at a faster rate than the overall balance. However, this ratio has increased by 1.48% month-on-month for the average one missed payment balance. With increased seasonal spend expected over the coming months, risk teams should monitor this closely.

Key Trend Indicators – UK Cards October 2023

|

Metric

|

Amount

|

Month-on-Month

Change

|

Year-on-Year

Change

|

|

Average UK Credit Card Spend

|

£785

|

-3%

|

+6%

|

|

Average Card Balance

|

£1,725

|

-0.4%

|

+9.8%

|

|

Percentage of Payments to Balance

|

37.8%

|

-0.7%

|

-6.8%

|

|

Accounts with One Missed Payment

|

1.6%

|

-4.3%

|

+7.2%

|

|

Accounts with Two Missed Payments

|

0.3%

|

+8%

|

+11.9%

|

|

Accounts with Three Missed Payments

|

0.2%

|

-0.4%

|

+18.9%

|

|

Average Credit Limit

|

£5,605

|

+0.1%

|

+1.8%

|

|

Average Overlimit Spend

|

£90

|

+2.3%

|

-4.2%

|

|

Cash Sales / Total Sales

|

0.9%

|

-4.2%

|

-4.6%

|

|

Source: FICO

|

|

|

|

These card performance figures are part of the data shared with subscribers of the FICO® Benchmark Reporting Service. The data sample comes from client reports generated by the FICO® TRIAD® Customer Manager solution in use by some 80% of UK card issuers. For more information on these trends, contact FICO.

About FICO

FICO (NYSE: FICO) powers decisions that help people and businesses around the world prosper. Founded in 1956, the company is a pioneer in the use of predictive analytics and data science to improve operational decisions. FICO holds more than 220 US and foreign patents on technologies that increase profitability, customer satisfaction and growth for businesses in financial services, insurance, telecommunications, health care, retail and many other industries. Using FICO solutions, businesses in more than 100 countries do everything from protecting 2.6 billion payment cards from fraud, to improving financial inclusion, to increasing supply chain resiliency. The FICO® Score, used by 90% of top US lenders, is the standard measure of consumer credit risk in the US and other countries, improving risk management, credit access and transparency. Learn more at www.fico.com.

FICO and TRIAD are registered trademarks of Fair Isaac Corporation in the U.S. and other countries.

View source version on businesswire.com: https://www.businesswire.com/news/home/20231214091277/en/