F&M continues strong start to 2024 with solid second quarter results.

See associated, unaudited summary consolidated financial data for additional information.

TIMBERVILLE, VA / ACCESSWIRE / July 29, 2024 / F&M Bank Corp. (the "Company" or "F&M"), (OTCQX:FMBM), the parent company of Farmers & Merchants Bank ("F&M Bank" or the "Bank"), today reported results for the quarter and six months ended June 30, 2024.

Net income was $3.0 million or $0.86 per share for the quarter ended June 30, 2024, compared to $1.2 million or $0.35 per share for the linked quarter ended March 31, 2024, and compared to $241,000 or $0.07 per share for the prior year quarter ended June 30, 2023. For the six months ended June 30, 2024, net income was $4.2 million or $1.21 per share, which exceeds net income of $1.3 million, or $0.37 per share, for the same period in 2023. Net income for the six months ended June 30, 2023, included $810,000 in after-tax, one-time expenses, including severance accruals for former bank officers.

On June 30, 2024, the Company had total assets of $1.31 billion, total loans of $826.3 million, and total deposits of $1.19 billion, reflecting growth in second quarter 2024 of $468,000 in total loans and $28.9 million in total deposits. Our loan portfolio consists of a mix of loan types, intended to hedge against risks associated with concentrations in any particular type of loan.

Also noteworthy, the Company's tangible book value per common share has increased to $22.621 at June 30, 2024 from $21.551 on December 31, 2023. Tangible book value per common share is a non-GAAP financial measure. Further information can be found under the heading "Non-GAAP Financial Measures" and in the footnotes to the table accompanying this release.

"I am pleased to share F&M's financial results for second quarter and year-to-date 2024," said Mike Wilkerson, chief executive officer. "During the second quarter, we continued to achieve positive trends in increased revenue and interest income, controlled operational expenses, experienced solid growth in both deposits and loans, and benefited from strong asset quality.

"These results reflect our focus on generating ‘sufficient and sustainable profit,' which is our number one priority. They also show our focus on the Company's future, as the execution of our strategic plan continues and as the results from that plan are realized. Across the board, these outcomes and growth are a team effort, with each area and business line of F&M stepping up and contributing. It is through this team effort, for which we are all grateful, that we will continue to grow as a Company and in our ability to serve the people and businesses of the Shenandoah Valley."

SECOND QUARTER INCOME STATEMENT COMPARISON

Overview

Net income for second quarter 2024 was $3.0 million or $0.86 per share, compared to $1.2 million or $0.35 per share for first quarter 2024, an increase of $1.8 million or $0.51 per share. Return on average assets was 0.93% and return on average equity was 15.59% for the three months ended June 30, 2024. Both ratios are higher than those reported for first quarter 2024. The improvement in net income is attributed primarily to a recovery of credit losses of $458,000 in the second quarter compared to a provision of $824,000 in the first quarter. Also contributing to the improvement, net interest income is $70,000 higher than in the linked quarter. Additionally, noninterest income increased by $644,000 to just under $3.0 million in the second quarter and noninterest expenses declined by $275,000. Due to the improved results, income tax expense increased by $472,000.

Net income increased by $2.8 million or $0.79 per share from the $241,000 or $0.07 per share reported for second quarter 2023. Return on average assets increased by 0.85% and return on average equity increased by 14.26%. The improved results reflect an increase of $422,000 in net interest income, a decrease of $997,000 in the provision for credit losses, an increase of $79,000 in noninterest income and a reduction of $2.2 million in noninterest expenses. Results for second quarter 2023 included a pre-tax severance accrual of $773,000 which lowered net income by $611,000.

Net Interest Income and Net Interest Margin

For second quarter 2024, net interest income totaled $8.2 million, an increase of $70,000 from first quarter 2024, as a $143,000 increase in interest income outpaced a $73,000 increase in interest expense. Net interest margin for the quarter was 2.72%, up eight basis points on a linked quarter basis. Higher loan balances and repricing of adjustable-rate loans contributed to a $142,000 increase in loan interest income, which comprised most of the increase in interest income and increased the earning asset yield by twelve basis points to 5.19%. Cost of funds increased by six basis points to 2.51%. Total interest expense increased by $73,000, a combination of a $614,000 increase in interest expense on deposits and a $542,000 decrease on interest expense on short-term debt. The increase in interest expense on deposits resulted from growth in time deposit balances and higher rates paid on new time deposits. This was partially offset by the decrease in interest expense on short-term debt as Federal Home Loan Bank advances declined from $60.0 million on March 31, 2024, to $20.0 million on June 30, 2024.

Compared to second quarter 2023, net interest margin increased by seven basis points as the earning asset mix shifted from cash and investments to loans. Loans as a percentage of earning assets increased to 68% in second quarter 2024 from 65% in second quarter 2023. Interest income increased $2.1 million, and the earning asset yield increased by 0.55% due to higher average balances and interest rates on loans, federal funds sold and interest-bearing cash balances. Interest expense grew by $1.7 million due to growth in both the average balances of and rates paid on time deposits causing the cost of funds to increase by 0.76%.

Provision for (Recovery of) Credit Losses

During second quarter 2024, the Bank recorded a $458,000 recovery of credit losses compared to an $823,000 provision for credit losses in first quarter 2024 and a $539,000 provision in second quarter 2023. The current quarter recovery was the result of the release of $608,000 in reserves related to the improvement in the collateral value on a $4.2 million individually evaluated loan relationship, net loan charge-offs of $179,000, slower loan growth and an improvement to the experience, depth and ability of lending management qualitative factor used in the Bank's Allowance for Credit Losses on Loans ("ACLL") model. By comparison, net charge-offs were $807,000 in first quarter 2024 and $344,000 in second quarter 2023. Also, gross loans grew more during those periods, by $3.8 million in first quarter 2024 and $19.3 million in second quarter 2023. On June 30, 2024, the ACLL totaled $7.8 million or 0.95% of gross loans outstanding.

Noninterest Income

Noninterest income, which includes gains and losses, totaled $3.0 million for second quarter 2024, an increase of $644,000 from first quarter 2024. Several categories of noninterest income increased on a linked quarter basis. Service charges on deposits increased by $18,000, investment services and insurance income increased by $48,000, mortgage banking income increased by $375,000, title insurance income increased by $124,000, and ATM and check card fees increased by $75,000. The other categories of noninterest income combined to increase noninterest income by $5,000.

Compared to second quarter 2023, noninterest income increased by $79,000. The increase resulted from increases of $17,000 in service charges on deposit accounts, $272,000 in investment services and insurance income, $236,000 in mortgage banking income, and $68,000 in title insurance income. There was a decrease of $436,000 in income from bank owned life insurance due to a gain received upon the death of a retired bank officer in 2023. Also, other operating income declined by $90,000. Smaller year-over-year changes in other categories netted to increase noninterest income by another $12,000.

Noninterest Expenses

Noninterest expenses totaled $8.2 million for second quarter 2024, compared to $8.4 million in first quarter 2024 a decrease of $275,000. During second quarter 2024, the Bank recognized $577,000 in gains from lump sum pension distributions, which drove a decrease in employee benefits expense of $514,000. There were decreases of $69,000 in ATM and check card fees, and $12,000 in legal and professional fees. These decreases offset increases of $65,000 in salary expense, $27,000 in occupancy expenses, $33,000 in equipment expense, $21,000 in other real estate owned expenses, $19,000 in telecommunications and data processing expenses, $24,000 in directors' fees and $126,000 in other operating expenses. There were other changes in noninterest expense categories that combined to increase total noninterest expenses by $5,000.

Compared to the same quarter in 2023, noninterest expenses declined $2.2 million. As a result of the voluntary early exit plan that was implemented in 2023, salary expense declined by $1.2 million. Employee benefits expense declined by $684,000 due to the combination of the voluntary early exit plan and gains received from pension lump sum distributions. There were decreases of $46,000 in equipment expense, $141,000 in advertising expense, $71,000 in legal and professional fees, $88,000 in ATM and check card fees, and $144,000 in other operating expenses. Offsetting these decreases were increases of $88,000 in occupancy expense, $89,000 in FDIC insurance expense, and $41,000 in bank franchise tax expense. The remaining categories combined to increase noninterest expenses by $8,000.

YEAR-TO-DATE INCOME STATEMENT COMPARISON

Overview

Net income for the six months ended June 30, 2024 was $4.2 million or $1.21 per share, compared to $1.3 million or $0.37 per share for the same period in 2023, an increase of $2.9 million or $0.84 per share. Return on average assets was 0.65% and return on average equity was 10.96% for the first half of 2024. Both ratios are higher than those reported for the first six months of 2023. The improvement in net income is attributed primarily to lower noninterest expenses, which declined by $2.8 million to $16.6 million. Net interest income and noninterest income also improved by $709,000 and $231,000, respectively. The year-to-date provision for credit losses decreased from $539,000 in 2023 to $366,000 in 2024.

Net Interest Income and Net Interest Margin

In the first half of 2024, net interest income totaled $16.3 million, an increase of $709,000 from 2023, as a $4.7 million increase in interest income outpaced a $4.0 million increase in interest expense. Net interest margin was 2.71%, up two basis points from the 2.69% reported for the first half of 2023. Higher loan balances and repricing of adjustable-rate loans contributed to a $4.5 million increase in loan interest income, which comprised most of the increase in interest income and increased the earning asset yield by sixty-one basis points to 5.18%. Cost of funds increased by fifty-eight basis points to 2.49%. Total interest expense increased by $4.0 million, due to growth in both the average balances of and rates paid on time deposits.

Provision for Credit Losses

During the first six months of 2024, the Bank recorded a $366,000 provision for credit losses compared to a $539,000 provision for credit losses in the same period in 2023. The provision was the result of $986,000 in net charge-offs, which were partially offset by the release of $608,000 in reserves related to improvement in the collateral value of a $4.2 million individually evaluated loan relationship.

Noninterest Income

Noninterest income, which includes gains and losses, totaled $5.3 million for the first half of 2024, an increase of $231,000 from the first half of 2023. Several categories of noninterest income increased on a year-over-year basis. Service charges on deposit accounts increased by $66,000, investment services and insurance income increased by $345,000, mortgage banking income increased by $92,000, title insurance income increased by $136,000, and ATM and check card fees increased by $39,000. Income on bank owned life insurance declined by $434,000 due to the gains received in 2023. Other categories of noninterest income combined to decrease noninterest income by $13,000.

Noninterest Expenses

Noninterest expenses totaled $16.6 million for first six months of 2024, compared to $19.4 million for the same period of 2023, a decrease of $2.8 million. Salary expense declined by $1.7 million due to cost savings associated with a voluntary early exit plan implemented in fourth quarter 2023. Employee benefits expense declined by $919,000 due to a combination of the voluntary early exit plan, $577,000 in gains from lump sum pension distributions, and a refund of $162,000 received in March 2024 due to better than projected group health insurance claims in 2023. There were declines of $228,000 in advertising expense, $145,000 in other operating expense, $80,000 in ATM and check card fees, and $62,000 in directors' fees. There were increases of $132,000 in occupancy expenses, $201,000 in FDIC insurance expense and $63,000 in bank franchise tax expense. There were other changes in noninterest expense categories that combined to decrease total noninterest expenses by $3,000.

BALANCE SHEET REVIEW

On June 30, 2024, assets totaled $1.31 billion, an increase of $15.0 million over December 31, 2023. Total loans increased by $4.2 million to $826.3 million, including increases of $8.3 million in residential mortgage loans, $10.3 million in other construction and land development loans, $8.9 million in commercial and industrial loans, and $2.8 million in multifamily loans. These increases were offset by decreases of $6.2 million in automobile loans, $6.0 million in residential construction loans, $1.3 million in credit card and other consumer loans, and $12.0 million in commercial real estate loans.

Investment securities decreased by $23.6 million due to paydowns on U.S. Agency mortgage-backed securities and expected bond maturities, combined with a decrease of $907,000 in unrealized loss on the bond portfolio. On June 30, 2024, the unrealized loss was $39.3 million compared to $40.2 million on December 31, 2023.

Total deposits on June 30, 2024, were $1.19 billion, an increase of $52.0 million from the end of 2023, due to growth of $46.0 million in interest bearing deposits, specifically time deposits, and an increase of $6.0 million in noninterest bearing deposits. On June 30, 2024, 11.34% of the Bank's total deposits were uninsured.

Shareholders' equity increased by $3.3 million to $81.6 million due to net income of $4.2 million, a decrease in accumulated other comprehensive loss of $717,000, and $102,000 in shares issued. These increases were offset by $1.8 million in dividends paid to shareholders. Tangible book value per common share has increased to $22.621 from $21.551 on December 31, 2023. Tangible book value per common share is a non-GAAP financial measure. Further information can be found under the heading "Non-GAAP Financial Measures" and in the footnotes to the table accompanying this release.

LIQUIDITY

The Company's on-balance sheet asset liquidity includes cash and cash equivalents, unpledged investment securities, and loans held for sale, which totaled $200.1 million on June 30, 2024, up from $178.0 million on December 31, 2023.

The Bank had access to off-balance sheet liquidity through unsecured Federal funds lines totaling $90.0 million on June 30, 2024, and December 31, 2023. The Bank has a secured line of credit with the Federal Home Loan Bank (FHLB) with available credit of $150.0 million as of June 30, 2024, and $90.1 million as of December 31, 2023. The FHLB line of credit is secured by a blanket lien on qualifying loans in the residential, commercial, agricultural real estate, and home equity portfolios. The Bank also pledged $206.6 million in securities to the Federal Reserve discount window which may be used for overnight borrowings.

The Bank is scheduled to receive $74.6 million from bond paydowns and maturities by the end of 2024 which can be used to fund future loan growth and for other purposes.

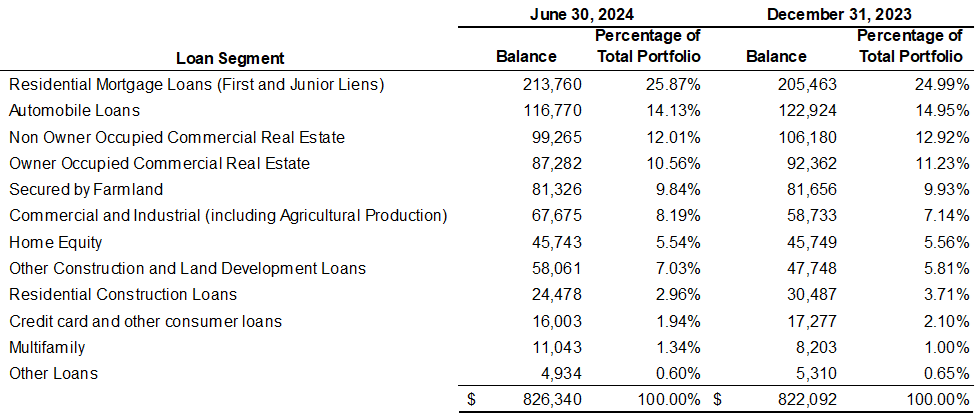

LOAN PORTFOLIO

The Company's loan portfolio is diversified with its largest segment being residential mortgage loans originated through its subsidiary F&M Mortgage that represents 25.87% of total loans. Total commercial real estate loans, both owner and non-owner occupied constitute $186.5 million or 22.57% of the loan portfolio. Automobile loans originated by its dealer finance division total $116.8 million and 14.13% of the portfolio. Following is a breakdown of the loan portfolio composition as of June 30, 2024, and December 31, 2023 (dollars in thousands):

ASSET QUALITY AND ALLOWANCE FOR CREDIT LOSSES

Nonperforming loans (NPLs) as a percentage of total assets were 0.58% on June 30, 2024, compared to 0.50% on December 31, 2023. Net charge-offs as a percentage of average loans were 0.09% for the quarter ended June 30, 2024, down 0.30% from the linked quarter March 31, 2024, and down 0.09% from second quarter 2023. Year-to-date net charge-offs for 2024 were 0.24% compared to 0.14% for the first six months of 2023.

The current quarter recovery was the result of the release of $608,000 in reserves related to improvement in the collateral value of a $4.2 million individually evaluated loan relationship, net loan charge-offs of $179,000, slower loan growth, and an improvement to the experience, depth and ability of lending management qualitative factor used in the Bank's ACLL model. By comparison, net charge-offs were $807,000 in first quarter 2024 and $344,000 in second quarter 2023. Gross loans grew by $500,000 in second quarter 2024 and $4.2 million in first quarter 2024. On June 30, 2024, the ACLL totaled $7.8 million or 0.95% of gross loans outstanding compared to $8.3 million or 1.01% of gross loans outstanding at December 31, 2023.

The reserve for unfunded commitments decreased from $690,000 at December 31, 2023, to $575,000 at June 30, 2024, due to decreases in loan commitments of $10.3 million in commercial and industrial loans and $3.6 million in construction and land loans, which were offset by an increase of $2.1 million in commitments for 1-4 family residential construction and $3.1 million in owner-occupied commercial real estate.

DIVIDEND DECLARATION

On July 18, 2024, our Board of Directors declared a second quarter dividend of $0.26 per share to common shareholders. Based on our most recent trade price of $17.25 per share, this constitutes a 6.03% yield on an annualized basis. The dividend will be paid on August 29, 2024, to shareholders of record as of August 14, 2024.

###

ABOUT US

F&M Bank Corp. is an independent, locally owned, financial holding company offering a full range of financial services through our subsidiary, Farmers & Merchants Bank's (F&M Bank) fourteen banking offices in Rockingham, Shenandoah, and Augusta counties, Virginia, and the cities of Winchester and Waynesboro, Virginia. The Company also owns F&M Mortgage, a mortgage lending subsidiary, and VSTitle, a title company subsidiary. Founded in 1908 as a community venture to serve the farmers and merchants of the Shenandoah Valley, where both the Company and the Bank are headquartered, F&M Bank remains more committed than ever to the success of the agricultural industry, small business ventures, and the nonprofit sector.F&M's values, which are gregarious, resolute, original, and wholehearted (G.R.O.W.), combined with our brand pillars of sustenance, security, and enrichment, shape the Company's decision-making, philanthropy, and volunteerism. The only publicly traded organization based in Rockingham County, we offer a diverse suite of financial products and services and a strong team dedicated to living our mission of being the financial partner of choice in the Shenandoah Valley, both today and tomorrow, as we have been since 1908. Additional information may be found by visiting our website, fmbankva.com.

NON-GAAP FINANCIAL MEASURES

The accounting and reporting policies of the Company conform to U.S. generally accepted accounting principles ("GAAP") and prevailing practices in the banking industry. However, management uses certain non-GAAP measures, including tangible book value per share, to supplement the evaluation of the Company's financial condition and performance. Management believes presentation of these non-GAAP financial measures provides useful supplemental information that is essential to a proper understanding of the Company's operating results. These non-GAAP disclosures should not be viewed as a substitute for operating results determined in accordance with GAAP, nor are they necessarily comparable to non-GAAP performance measures that may be presented by other companies. A definition of GAAP to non-GAAP measures is included in the footnotes to the table accompanying this release.

FORWARD-LOOKING STATEMENTS

This press release may contain "forward-looking statements" as defined by federal securities laws, which are subject to significant risks and uncertainties. These include statements regarding future plans, strategies, results, or expectations that are not historical facts, and are generally identified by the use of words such as "believe," "expect," "intend," "anticipate," "will," "estimate," "project" or similar expressions. These statements are based on estimates and assumptions, and our ability to predict results, or the actual effect of future plans or strategies, is inherently uncertain. Our actual results could differ materially from those contemplated by these forward-looking statements. Factors that could have a material adverse effect on our operations and future prospects include, but are not limited to, changes in local and national economies or market conditions; changes in interest rates; regulations and accounting principles; changes in policies or guidelines; loan demand and asset quality, including values of real estate and other collateral; deposit flow; the impact of competition from traditional or new sources; and other factors. Readers should consider these risks and uncertainties in evaluating forward-looking statements and should not place undue reliance on such statements. We undertake no obligation to update these statements following the date of this press release.

F&M Bank Corp.

Summary Consolidated Financial Data (unaudited)

Dollars in Thousands, except for per share data

|

|

|

Quarter to Date

|

|

|

Year-to-Date

|

|

|

|

|

6/30/2024

|

|

|

3/31/2024

|

|

|

12/31/2023 (3)

|

|

|

9/30/2023 (3)

|

|

|

6/30/2023 (3)

|

|

|

6/30/2024

|

|

|

6/30/2023 (3)

|

|

|

Condensed Balance Sheet

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Cash and cash equivalents

|

|

$

|

50,459

|

|

|

$

|

52,486

|

|

|

$

|

23,717

|

|

|

$

|

22,159

|

|

|

$

|

36,505

|

|

|

$

|

50,459

|

|

|

$

|

36,505

|

|

|

Investment securities

|

|

|

355,930

|

|

|

|

369,744

|

|

|

|

379,557

|

|

|

|

383,502

|

|

|

|

394,868

|

|

|

|

355,930

|

|

|

|

394,868

|

|

|

Loans held for sale

|

|

|

3,958

|

|

|

|

1,385

|

|

|

|

1,119

|

|

|

|

2,028

|

|

|

|

881

|

|

|

|

3,958

|

|

|

|

881

|

|

|

Gross loans

|

|

|

826,340

|

|

|

|

825,872

|

|

|

|

822,092

|

|

|

|

805,602

|

|

|

|

776,260

|

|

|

|

826,340

|

|

|

|

776,260

|

|

|

Allowance for credit losses

|

|

|

(7,815

|

)

|

|

|

(8,408

|

)

|

|

|

(8,321

|

)

|

|

|

(9,166

|

)

|

|

|

(8,769

|

)

|

|

|

(7,815

|

)

|

|

|

(8,769

|

)

|

|

Goodwill

|

|

|

3,082

|

|

|

|

3,082

|

|

|

|

3,082

|

|

|

|

3,082

|

|

|

|

3,082

|

|

|

|

3,082

|

|

|

|

3,082

|

|

|

Other assets

|

|

|

77,691

|

|

|

|

72,053

|

|

|

|

73,350

|

|

|

|

75,212

|

|

|

|

75,543

|

|

|

|

77,691

|

|

|

|

75,543

|

|

|

Total Assets

|

|

$

|

1,309,645

|

|

|

$

|

1,316,214

|

|

|

$

|

1,294,596

|

|

|

$

|

1,282,419

|

|

|

$

|

1,278,370

|

|

|

$

|

1,309,645

|

|

|

$

|

1,278,370

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Noninterest bearing deposits

|

|

$

|

270,246

|

|

|

$

|

267,106

|

|

|

$

|

264,254

|

|

|

$

|

277,219

|

|

|

$

|

277,578

|

|

|

$

|

270,246

|

|

|

$

|

277,578

|

|

|

Interest bearing deposits

|

|

|

915,011

|

|

|

|

889,237

|

|

|

|

868,982

|

|

|

|

856,691

|

|

|

|

859,534

|

|

|

|

915,011

|

|

|

|

859,534

|

|

|

Total Deposits

|

|

|

1,185,257

|

|

|

|

1,156,343

|

|

|

|

1,133,236

|

|

|

|

1,133,910

|

|

|

|

1,137,112

|

|

|

|

1,185,257

|

|

|

|

1,137,112

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Short-term debt

|

|

|

20,000

|

|

|

|

60,000

|

|

|

|

60,000

|

|

|

|

60,000

|

|

|

|

47,000

|

|

|

|

20,000

|

|

|

|

47,000

|

|

|

Long-term debt

|

|

|

6,954

|

|

|

|

6,943

|

|

|

|

6,932

|

|

|

|

6,922

|

|

|

|

6,911

|

|

|

|

6,954

|

|

|

|

6,911

|

|

|

Other liabilities

|

|

|

15,818

|

|

|

|

15,194

|

|

|

|

16,105

|

|

|

|

14,567

|

|

|

|

15,153

|

|

|

|

15,818

|

|

|

|

15,153

|

|

|

Total Liabilities

|

|

|

1,228,029

|

|

|

|

1,238,480

|

|

|

|

1,216,273

|

|

|

|

1,215,399

|

|

|

|

1,206,176

|

|

|

|

1,228,029

|

|

|

|

1,206,176

|

|

|

Shareholders' equity

|

|

|

81,616

|

|

|

|

77,734

|

|

|

|

78,323

|

|

|

|

67,020

|

|

|

|

72,194

|

|

|

|

81,616

|

|

|

|

72,194

|

|

|

Total Liabilities and Shareholders' Equity

|

|

$

|

1,309,645

|

|

|

$

|

1,316,214

|

|

|

$

|

1,294,596

|

|

|

$

|

1,282,419

|

|

|

$

|

1,278,370

|

|

|

$

|

1,309,645

|

|

|

$

|

1,278,370

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Condensed Income Statement

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest income and fees on loans

|

|

$

|

13,494

|

|

|

$

|

13,352

|

|

|

$

|

13,061

|

|

|

$

|

12,525

|

|

|

$

|

11,517

|

|

|

$

|

26,846

|

|

|

$

|

22,371

|

|

|

Interest income and fees on loans held for sale

|

|

|

46

|

|

|

|

18

|

|

|

|

22

|

|

|

|

19

|

|

|

|

25

|

|

|

|

64

|

|

|

|

47

|

|

|

Income on cash and securities

|

|

|

2,180

|

|

|

|

2,207

|

|

|

|

2,074

|

|

|

|

2,028

|

|

|

|

2,092

|

|

|

|

4,387

|

|

|

|

4,198

|

|

|

Total Interest Income

|

|

|

15,720

|

|

|

|

15,577

|

|

|

|

15,157

|

|

|

|

14,572

|

|

|

|

13,634

|

|

|

|

31,297

|

|

|

|

26,616

|

|

|

Interest expense on deposits

|

|

|

6,951

|

|

|

|

6,337

|

|

|

|

6,108

|

|

|

|

5,811

|

|

|

|

5,218

|

|

|

|

13,288

|

|

|

|

9,255

|

|

|

Interest expense on short-term debt

|

|

|

454

|

|

|

|

996

|

|

|

|

812

|

|

|

|

702

|

|

|

|

523

|

|

|

|

1,450

|

|

|

|

1,514

|

|

|

Interest expense on long-term debt

|

|

|

116

|

|

|

|

115

|

|

|

|

116

|

|

|

|

115

|

|

|

|

116

|

|

|

|

231

|

|

|

|

228

|

|

|

Total Interest Expense

|

|

|

7,521

|

|

|

|

7,448

|

|

|

|

7,036

|

|

|

|

6,628

|

|

|

|

5,857

|

|

|

|

14,969

|

|

|

|

10,997

|

|

|

Net Interest Income

|

|

|

8,199

|

|

|

|

8,129

|

|

|

|

8,121

|

|

|

|

7,944

|

|

|

|

7,777

|

|

|

|

16,328

|

|

|

|

15,619

|

|

|

Provision for (recovery of) credit losses

|

|

|

(458

|

)

|

|

|

824

|

|

|

|

(134

|

)

|

|

|

620

|

|

|

|

539

|

|

|

|

366

|

|

|

|

539

|

|

|

Noninterest income

|

|

|

2,986

|

|

|

|

2,342

|

|

|

|

2,464

|

|

|

|

2,572

|

|

|

|

2,907

|

|

|

|

5,328

|

|

|

|

5,097

|

|

|

Noninterest expense

|

|

|

8,156

|

|

|

|

8,431

|

|

|

|

10,482

|

|

|

|

8,922

|

|

|

|

10,335

|

|

|

|

16,587

|

|

|

|

19,364

|

|

|

Income tax expense (benefit)

|

|

|

471

|

|

|

|

(1

|

)

|

|

|

(220

|

)

|

|

|

(44

|

)

|

|

|

(431

|

)

|

|

|

470

|

|

|

|

(483

|

)

|

|

Net Income

|

|

$

|

3,016

|

|

|

$

|

1,217

|

|

|

$

|

457

|

|

|

$

|

1,018

|

|

|

$

|

241

|

|

|

$

|

4,233

|

|

|

$

|

1,296

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Per Share Data

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Earnings per common share - basic

|

|

$

|

0.86

|

|

|

$

|

0.35

|

|

|

$

|

0.13

|

|

|

$

|

0.29

|

|

|

$

|

0.07

|

|

|

$

|

1.21

|

|

|

$

|

0.37

|

|

|

Book Value per Share

|

|

|

23.54

|

|

|

|

22.11

|

|

|

|

22.47

|

|

|

|

19.43

|

|

|

|

20.75

|

|

|

|

23.54

|

|

|

|

20.75

|

|

|

Tangible Book Value per Share (1)

|

|

|

22.62

|

|

|

|

21.20

|

|

|

|

21.55

|

|

|

|

18.50

|

|

|

|

19.82

|

|

|

|

22.62

|

|

|

|

19.82

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Key Performance Ratios

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Return on Average Assets

|

|

|

0.93

|

%

|

|

|

0.37

|

%

|

|

|

0.14

|

%

|

|

|

0.32

|

%

|

|

|

0.08

|

%

|

|

|

0.65

|

%

|

|

|

0.20

|

%

|

|

Return on Average Equity

|

|

|

15.59

|

%

|

|

|

6.25

|

%

|

|

|

2.49

|

%

|

|

|

5.80

|

%

|

|

|

1.33

|

%

|

|

|

10.96

|

%

|

|

|

3.62

|

%

|

|

Noninterest Income / Average Assets

|

|

|

0.92

|

%

|

|

|

0.71

|

%

|

|

|

0.76

|

%

|

|

|

0.80

|

%

|

|

|

0.92

|

%

|

|

|

0.82

|

%

|

|

|

0.80

|

%

|

|

Noninterest Expense / Average Assets

|

|

|

2.52

|

%

|

|

|

2.54

|

%

|

|

|

3.23

|

%

|

|

|

2.76

|

%

|

|

|

3.28

|

%

|

|

|

2.56

|

%

|

|

|

3.05

|

%

|

|

Efficiency Ratio (2)

|

|

|

71.23

|

%

|

|

|

78.67

|

%

|

|

|

96.79

|

%

|

|

|

82.81

|

%

|

|

|

94.35

|

%

|

|

|

74.77

|

%

|

|

|

91.14

|

%

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net Interest Margin

|

|

|

2.72

|

%

|

|

|

2.64

|

%

|

|

|

2.66

|

%

|

|

|

2.67

|

%

|

|

|

2.65

|

%

|

|

|

2.71

|

%

|

|

|

2.69

|

%

|

|

Earning Asset Yield

|

|

|

5.19

|

%

|

|

|

5.07

|

%

|

|

|

4.96

|

%

|

|

|

4.87

|

%

|

|

|

4.64

|

%

|

|

|

5.18

|

%

|

|

|

4.57

|

%

|

|

Cost of Interest Bearing Liabilities

|

|

|

3.21

|

%

|

|

|

3.14

|

%

|

|

|

3.00

|

%

|

|

|

2.87

|

%

|

|

|

2.61

|

%

|

|

|

3.17

|

%

|

|

|

2.51

|

%

|

|

Cost of Funds

|

|

|

2.51

|

%

|

|

|

2.45

|

%

|

|

|

2.37

|

%

|

|

|

2.26

|

%

|

|

|

1.75

|

%

|

|

|

2.49

|

%

|

|

|

1.91

|

%

|

|

Net Interest Spread

|

|

|

2.68

|

%

|

|

|

2.62

|

%

|

|

|

2.59

|

%

|

|

|

2.61

|

%

|

|

|

2.89

|

%

|

|

|

2.69

|

%

|

|

|

2.66

|

%

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net Charge-offs

|

|

$

|

179

|

|

|

$

|

807

|

|

|

$

|

770

|

|

|

$

|

193

|

|

|

$

|

344

|

|

|

$

|

986

|

|

|

$

|

510

|

|

|

Net Charge-offs as a % of Avg Loans

|

|

|

0.09

|

%

|

|

|

0.39

|

%

|

|

|

0.38

|

%

|

|

|

0.10

|

%

|

|

|

0.18

|

%

|

|

|

0.24

|

%

|

|

|

0.14

|

%

|

|

Non-Performing Loans

|

|

$

|

7,586

|

|

|

$

|

6,246

|

|

|

$

|

6,469

|

|

|

$

|

3,586

|

|

|

$

|

1,997

|

|

|

$

|

7,586

|

|

|

$

|

1,997

|

|

|

Non-Performing Loans to Total Assets

|

|

|

0.58

|

%

|

|

|

0.47

|

%

|

|

|

0.50

|

%

|

|

|

0.28

|

%

|

|

|

0.16

|

%

|

|

|

0.58

|

%

|

|

|

0.16

|

%

|

|

Non-Performing Assets

|

|

$

|

7,586

|

|

|

$

|

6,246

|

|

|

$

|

6,524

|

|

|

$

|

3,586

|

|

|

$

|

1,997

|

|

|

$

|

7,586

|

|

|

$

|

1,997

|

|

|

Non-Performing Assets to Total Assets

|

|

|

0.58

|

%

|

|

|

0.47

|

%

|

|

|

0.50

|

%

|

|

|

0.28

|

%

|

|

|

0.16

|

%

|

|

|

0.58

|

%

|

|

|

0.16

|

%

|

|

ACLL as a % of Total Loans

|

|

|

0.95

|

%

|

|

|

1.02

|

%

|

|

|

1.01

|

%

|

|

|

1.14

|

%

|

|

|

1.13

|

%

|

|

|

0.95

|

%

|

|

|

1.13

|

%

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Loans to Deposits

|

|

|

69.72

|

%

|

|

|

71.42

|

%

|

|

|

72.54

|

%

|

|

|

71.05

|

%

|

|

|

68.27

|

%

|

|

|

69.72

|

%

|

|

|

68.27

|

%

|

(1) Tangible book value per share is calculated by subtracting goodwill and other intangibles from total shareholders' equity and dividing the result by the common shares outstanding. Tangible book value per share is a non-GAAP financial measure that management believes provides investors with important information that may be related to the valuation of common stock.

(2) The Efficiency Ratio equals noninterest expenses divided by the sum of tax equivalent net interest income and noninterest income. Noninterest income excludes gains (losses) on securities transactions and low-income housing partnership losses. Noninterest expense excludes amortization of intangibles.

(3) Certain reclassifications have been made in the 2023 financial information to conform to reporting for the 2024. These reclassifications are not considered material and had no impact on prior year's net income, balance sheet or shareholders' equity.

FOR MORE INFORMATION, CONTACT

Lisa F. Campbell | EVP | Chief Financial Officer

540-896-1705

fmbankva.com

SOURCE: F&M Bank Corp

View the original

press release on accesswire.com