With due deference to the greatness of William Shakespeare, the opening line of Hamlet is one that has been found not only in literature, but in film, music and politics, and is a question that has been asked for centuries as to whether the pain we endure in life is preferable to the calm found in the "sleep of death." Likewise, whether the agony of nervous elation we have been experiencing on the long side of the precious metals markets is preferable to the safety of the profit-taken sidelines is yet another question of Shakespearean magnitude as gold and silver are now in areas of extreme synonymous with tops in 2011 and 2016.

As I wrote about in June, "when conditions change, I change," and just as it appeared as though the commercial cretins at the bullion banks were about to reject gold's probe above the six-year resistance at $1,350–1,375, a level rejected five times in six years, the U.S. dollar price for gold exploded northward and despite shockingly high and persistent RSI (relative strength index) and MACD (moving average convergence/divergence) readings, dragging the miners to multiyear highs with silver finally catching that all-too-elusive bid not seen in decade. During this past three-month orgy of golden worship, I have slowly been paring positions, building cash, tightening stops and reducing risk with the full knowledge that I would be leaving some of the profits on the table, a discipline so difficult that enforcing it requires massive medications and libational stress relief, both of which are in copious quantity in the MJB trading cockpit. Not an easy task when Led Zeppelin's "When the Levee Breaks" drowns out the sputtering squawks of CNBC's clueless anchors.

As the title of this missive imbues, "to be or not to be" an "all-in" gold and silver bull is a question that begs to be asked, because after forty years of covering the precious metals in one form or another, the wheels and axles on the gold and silver bandwagon are now straining and creaking under the weight of a deluge of newly anointed gold "experts," all of whom are clamoring for recognition that they were "THE FIRST" to "call the turn." With the Daily Sentiment Index (of gold bulls) now scraping 95% and Barron's and the WSJ running gold-and-silver-friendly stories recently, all that is left in order to cement the short-term top in the precious metals is a brand new sidebar similar to the one in late 2017 offering viewers a running Bitcoin price update, which I noted in this publication in December 2017 as one of the key "topping indicators" for the BTC mania. Well, we aren't quite there yet but CNBC has been forced, kicking and screaming, into having gold and silver "guest commentators" as more frequent fixtures in the CNBC daily landscape. Mind you, the CNBC reporters are just that—reporters—not market mavens as some might imagine, so if ratings can be goosed by some mutt plugging gold, on he or she comes and the circle of cable news life goes on.

As a boater slave to the whims of the weather, I have learned to trust the direction of the barometer over the clouds on the horizon because clear skies and calm seas at daybreak can be transformed into 3-meter waves and 40-knot winds in an afternoon. The arrival of storms usually follows a sharp directional change in barometric pressure not unlike the role of the gold DSI (Daily Sentiment Index) in gauging just how crowded the gold trade has become. Short-term momentum gauges like RSI and MACD can be misleading but when combined with sharp and unusual increases in media coverage (with special attention to the blogosphere), it appears to me that barometric pressure for gold is dropping sharply with silver only marginally so. This favors my Trade of the Year, long silver and short gold whereby in early July, I effectively shorted the gold-silver ratio (GSR) at around 93, setting the likelihood of a winning trade at 98%. Today, the GSR resides at 81.72 for a 12.09% gain paid for with profits from the leveraged trades that I exited in late-June/early-July when gold first touched $1,375 and RSI spiked above 75. It should be noted that I DID go long a massive position in the SLV August $14 calls, which tripled and were legged out to the October $15.50 calls (@ $0.47) where half were sold at $1.80 (3.75-bagger) with the balance sold this morning at $2.31. (Needless to say, this was my BEST trade for the year thus far.)

The gold market today looks more vulnerable to a correction than does the silver market but please don't confuse the GSR with directional probability for the precious metals complex. We could see a 3–5% drop in gold accompanied by a 1–2% drop in silver, elongating the drop in the GSR while taking prices in real terms lower. As of this morning, I am once again flat the leveraged silver trade (SLV calls) but still short the GSR from 93. I have not touched (nor will I EVER) my physical gold and silver but remain 50% long GDXJ (from $30.22) and 50% long GDX (from $21.09) having reduced both positions around where they are this morning. I am considering a sale of the last of these holdings into any further strength. (To do so may require shattering the locks on both liquor cabinet and medicine chest in order to bolster resolve, a quality sorely lacking from years of excess…)

The gold market today looks more vulnerable to a correction than does the silver market but please don't confuse the GSR with directional probability for the precious metals complex. We could see a 3–5% drop in gold accompanied by a 1–2% drop in silver, elongating the drop in the GSR while taking prices in real terms lower. As of this morning, I am once again flat the leveraged silver trade (SLV calls) but still short the GSR from 93. I have not touched (nor will I EVER) my physical gold and silver but remain 50% long GDXJ (from $30.22) and 50% long GDX (from $21.09) having reduced both positions around where they are this morning. I am considering a sale of the last of these holdings into any further strength. (To do so may require shattering the locks on both liquor cabinet and medicine chest in order to bolster resolve, a quality sorely lacking from years of excess…)

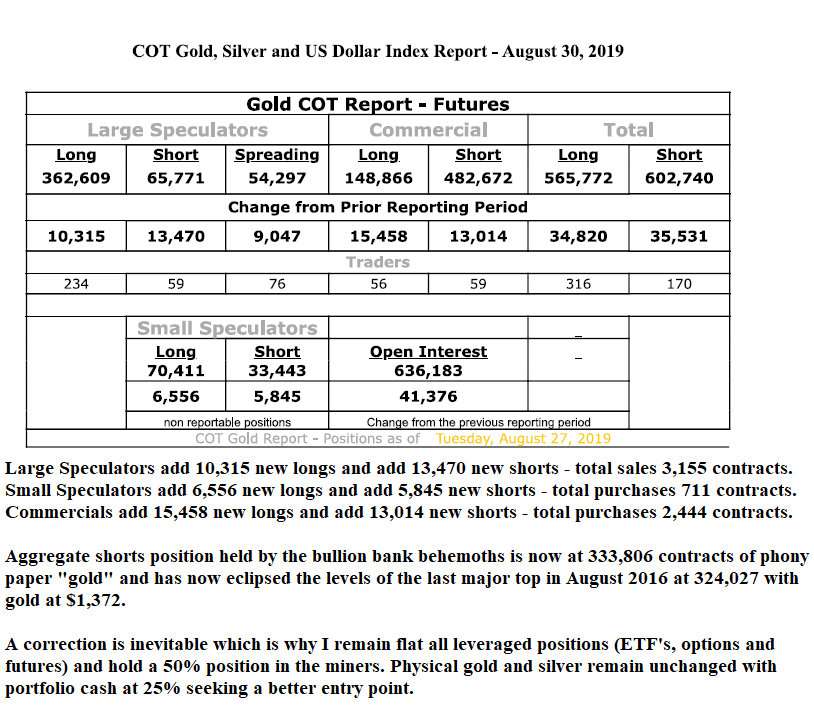

The Commitment of Traders report has been largely ineffective in calling a top for this particular move, unlike the 2016–2019 period whereby exaggerated moves in the aggregate short position held by Commercials allowed me to scurry to the sidelines avoiding what was about $400/ounce in drawdowns during that period. After the $1,375 breakout in June, the Commercials have certainly ceded control of the gold market to the newly minted bulls but have been steadily adding to short interest such that as of this weekend, a record 333,806 contracts of counterfeit "gold" representing 33,380,600 ounces worth over $51 billion U.S. dollars are now short. History has proven that when the bullion banks get this short, a correction (or perhaps an intermediate top) is looming.

If the "new paradigm" that everyone now uses as the reason to ignore all of the historical warnings proves itself out, then taking profits on positions (put on last January when everyone hated the precious metals) will be either early or outright wrong. However, my gut is telling me that the powers that be are going to pull out all the stops to keep the global stock rally marching on and WITHOUT competition from the precious metals markets. And it is times like this when everyone laughs you out of the room for being a Cassandra that vengeance is drawn. So, if I wind up with only physical gold and silver and a portfolio up 65% YTD (excluding trading profits in the leveraged positions), I will remain a satisfied investor with a ton of cash to deploy when and if the correction arrives.

To be or not to be an investor in gold was NOT the question on most people's minds last summer with gold below $1,200; I took out massive positions in the metals and the miners back when they were both universally hated by the mainstream. I leave you with one final chart that depicts this sudden and newfound love affair within which the mainstream is now embroiled. Taking positions in gold and gold miners after this kind of advance is NOT the "no-brainer" it was in August 2018. For this simple reason, I urge caution and the removal of a significant portion of the chips you have on the table, a table located in the precisely in the middle of a criminally rigged casino called the Comex. I am still trading but doing so with approximately one quarter of the significant profits locked in and banked, never to resurface under the covetous, ravenous, watchful eye of the bullion bank cartel. Trading with "house money" is at once both delightful and effective, but it carries a hidden danger because the cartel will let out just enough line to try to lure you back with your banked profits. They want THEIR money back and nothing drives a bullion bank into a mindless rage more than an investor trading with funds lifted from their greed-stained trousers. The permabulls will tell you that the bullion banks and their Treasury Department conspirators have lost all power in this "new paradigm" and we should relax and refrain from worry. I tend to disagree because wounded animals are the singular most dangerous of all creatures on this debt-ravaged planet and with gold at $1,552, these cartel cretins are now wounded, angry and very desperate animals.

A rose by any other color. . .

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger's adherence to the concept of "Hard Assets" allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

Disclosure:

1) Statements and opinions expressed are the opinions of Michael Ballanger and not of Streetwise Reports or its officers. Michael Ballanger is wholly responsible for the validity of the statements. Streetwise Reports was not involved in any aspect of the article preparation. Michael Ballanger was not paid by Streetwise Reports LLC for this article. Streetwise Reports was not paid by the author to publish or syndicate this article.

2) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

3) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Charts provided by the author.

Michael Ballanger Disclaimer:

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.