How good was 2019 for the precious metals market? It definitely brought quite some excitement to the arena. In today’s article, you’ll learn more about the most important gold price drivers in 2019. This analysis will help you better understand the gold market, and draw the right

investment conclusions for 2020.

Another year has passed! And we gave another accurate prediction. In the January 2019 edition of the

Market Overview, we wrote:

All these factors make us to believe that 2019 fundamental outlook for the gold market is better than one year ago (…) Hence, we should see better price performance next year.

Fast forward to January 2020 – we line now in the twenties! – it turned out that

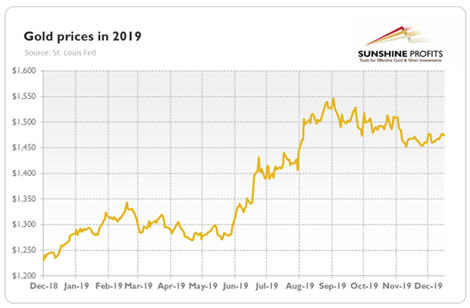

we were right again. Just look at the chart below, which paints the gold prices over the last year. The yellow metal entered 2019 quoted at $1279, and finished the year at $1474 (as of December 18).

Chart 1: Gold prices (London P.M Fix, in $) from December 2018 to December 2019.

So,

gold rose more than 15 percent last year (as of December 20), which was perfectly in line with my fundamental expectations! I did not expect a massive

rally (“we are not saying that bullion will start to

rally. What we are saying is that fundamental factors should become (…) more friendly toward gold”). And indeed, a 15-percent jump is impressive, but the yellow metal did not enter the full-blown

bull market. Nevertheless,

2019 was definitely better for gold prices than 2018, when the yellow metal dropped slightly.

We can distinguish four phases in the gold market in 2019:

- the bullish phase that lasted until mid-February, the price of gold increased from $1,279 to $1,344, or 5 percent;

- the bearish period that ended at the end of May, when gold prices declined to $,1271, or more than 5 percent, erasing all previous gains;

- the super bullish phase that lasted until early September, when the price of gold reached its peak of $1,546, soaring 21.6 percent in just three months; and

- the bearish remainder of the year, during which the yellow metal declined to $1474, or 4.7 percent.

What were the drivers behind gold’s behavior during these phases?

One important factor was the monetary policy. Gold started to go up at the very end of November 2018, when

Powell delivered speech considered as

dovish. But the February minutes were perceived as more

hawkish than expected, which sent gold prices down. Moreover, the

ECB adopted a more dovish stance later, which strengthened the U.S. dollar, while weakening both the

euro and gold.

However, in May,

the yield curve has become even more inverted, which triggered recessionary fears and pushed investors to expect a more dovish actions from the Fed. And indeed, the U.S. central bank started to signal more accommodative stance and even cut the

federal funds rate three times. But precious metals investors bought the rumor and sold the fact, as the price of the yellow metal started to decline since early September, amid the interest rates cuts. They could have also hoped for the lengthy cutting cycle, but the Fed decided to deliver only “mid-cycle adjustment” instead.

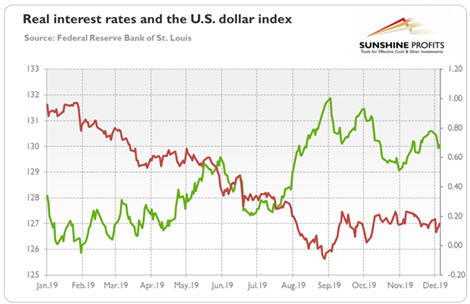

Let’s not forget about the

greenback and the U.S.

real interest rates –

two of the most important drivers of the gold prices. As one can see in the chart below, the dollar index, which measures the strength of the American currency against its peers, reached a local peak at the end of May, when gold started its

rally.

Chart 2: The U.S. real interest rates (red line, right axis, yields on 10-year Treasury Inflation-Indexed Security) and the U.S. dollar index (green line, left axis, Trade Weighted Broad U.S. Dollar Index) in 2019.

The real

yields were also important, as they bottomed out around the beginning of September, when the price of the yellow metal reached its 2019 peak. What is interesting is that

gold peaked together with the U.S. dollar, which suggests that both were considered as

safe havens during elevated worries about

recession. The increase in the interest rates since then pushed gold prices lower, despite the depreciation of the U.S. dollar.

And what about 2020 – will gold soar even more, shifting up a gear, or will it decelerate, after a good year? Well, nobody knows this for sure. But what we know is that – unless the next

economic crisis arrives – the U.S. central banks is likely to remain neutral (or to slash interest rates once, according to the

CME FedWatch Tool). Given the Fed cut interest rates three times in 2019, it implies that

the monetary policy will be less supportive for gold prices. Moreover, the

federal deficit is going to increase, which should lift the Treasury yields, putting downward pressure on the yellow metal. Last but not least, the reached “phase one” trade deal and the triumph of Conservatives in the British parliamentary elections mean that the uncertainty over the

trade wars and

Brexit should diminish.

So,

unless anything ugly happens, the macroeconomic environment could be less supportive for gold than in 2019. However, bad things do happen, and, according to Murphy’s law, anything that can go wrong will go wrong. Hence,

the gold fundamentals may turn out to be more positive for gold over the year. After all, the yield curve has inverted last year and we are already observing some recessionary trends, especially in the manufacturing sector and among the small-sized companies. So, from the fundamental point of view,

the first half of the year may be not the best for gold, but we could possibly see an improvement later.

If you enjoyed the above analysis and would you like to know more about the fundamentals of the gold market, we invite you to read the January

Market Overview report. If you’re interested in the detailed price analysis and price projections with targets, we invite you to sign up for our

Gold & Silver Trading Alerts. If you’re not ready to subscribe yet and are not on our gold mailing list yet, we urge you to sign up. It’s free and if you don’t like it, you can easily unsubscribe.

Sign up today!

Thank you.

Arkadiusz Sieron, PhD

Sunshine Profits – Effective Investments Through Diligence and Care

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Trading Alerts.