Teaser: The outbreak of COVID-19 has brutally reminded people of the risk of a pandemic. However, investors should never panic but look to history as a guide. We invite you thus to read our today’s article, which provides an important analysis of the history of pandemics and their effects on the gold market. Read it and learn what investment conclusions for the current epidemic we can draw.

Pandemics and Gold: Part 2

In the first part, we analyzed the HIV/AIDS

pandemic, as the most deadly pandemic since the 1971, and the SARS pandemic, as the most similar to the current COVID-19 pandemic. However, we have witnessed several other pandemics in the recent decades. Let’s investigate them now and

draw conclusions for the global economy and the gold market.

Let’s start with the

epidemic of

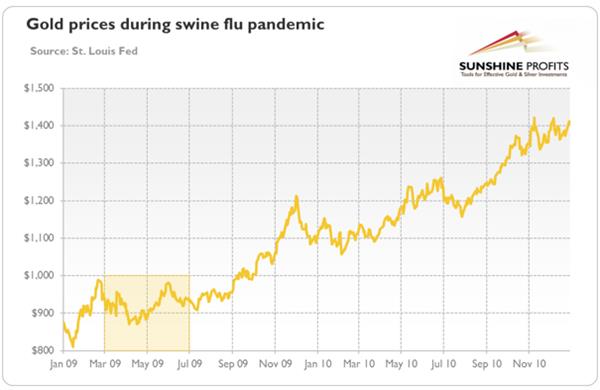

2009 A/H1N1 flu, called also the swine flu. It originated in pigs from central Mexico and lasted from early 2009 to late 2010. It was highly contagious, as around 1.66 billion of people, or

24 percent of the then global population, contracted the illness. Luckily, the case-fatality rate was very small, around 0.001-0.0035 percent, which resulted in an estimated range of deaths from between 151,700 and 575,400 people, around 10 times higher than the first estimates based on the number of cases confirmed by lab tests. The peak of interest in the swine flu occurred in April 2009, while the number of cases peaked in June 2009. As one can see in the chart below,

the price of gold did not rally to the hysteria about the swine flu. It is true that gold started in mid-2009 its great

bull market, but the

rally came after the peak in the swine flu outbreak, so it seems that it was rather a reaction to the

Great Recession and the Fed’s

quantitative easing.

Chart 1: Gold prices during swine flu pandemic (London P.M. Fix, in $).

The next

pandemic originated in 2012 in the Middle East, so it was named

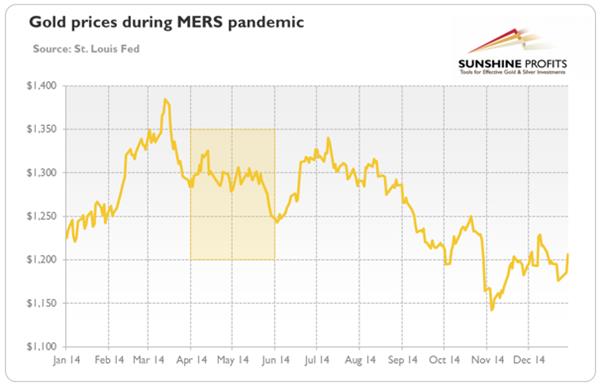

Middle East Respiratory Syndrome (MERS). Just like the

COVID-19 and SARS, the MERS was caused by the virus from the coronavirus group. It was likely transmitted to humans through camels and was much more dangerous than the swine flu, as its fatality rate was 34 percent. However, only 2,506 cases and 862 deaths

were reported from 2012 to January 15, 2020. The peak of infection and the peak of interest occurred in April – May 2014. As the chart below shows,

gold prices actually declined during the peak of MERS pandemic, which was probably caused by the limited geographical scope – the majority of cases were reported from Saudi Arabia and other countries in the Eastern Mediterranean.

Chart 2: Gold prices during MERS pandemic (London P.M. Fix, in $).

Another recent

pandemic was the

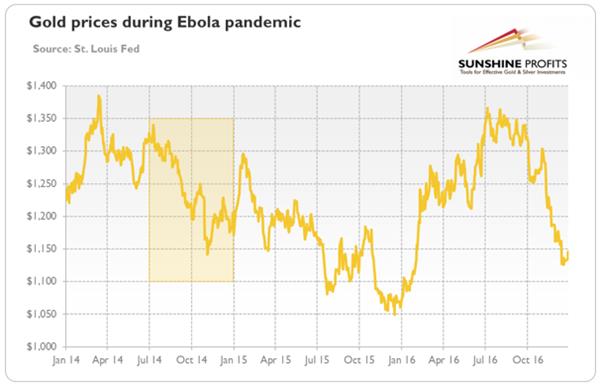

West African Ebola virus. It originated in December 2013 in Guinea and lasted until 2016. According to the

official data, there were a total of 28,646 suspected, probable and confirmed cases and 11,323 deaths (case-fatality rate of 39.5 percent), but the WHO suspects that the true number may be higher. The interest in Ebola virus started to rally in summer 2014 and remained elevated through the whole year, with the culmination in October. But as the chart below shows,

gold prices decreased in that period. The probable reason of the gold’s bearish reaction is the fact that the pandemic was contained to, as the name suggests, West Africa (mainly in Guinea, Liberia, and Sierra Leone), which is neither the major financial center nor the industrial center, like China is.

Chart 3: Gold prices during Ebola pandemic (London P.M. Fix, in $).

The next pandemic was the Zika fever

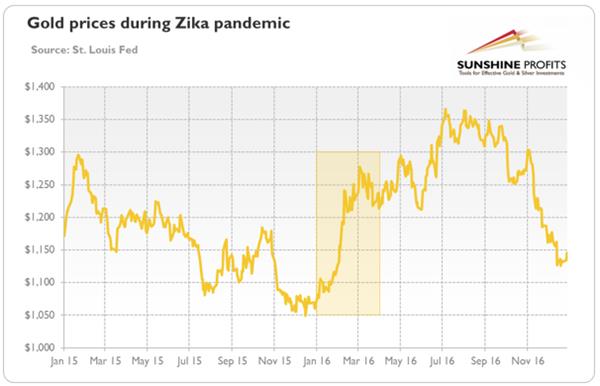

The next pandemic was the Zika fever caused by Zika virus in Brazil that started in March 2015. In November 2016, the WHO announced that Zika is no longer a public health emergency of international concern. It was estimated that 1.5 million people were infected by Zika in Brazil, with over 3,500 cases of microcephaly reported between October 2015 and January 2016. The interest in Zika virus started to rally in January 2016 and remained elevated through the whole year, with peaks in February and then again albeit lower in August.

The price of gold also started to rally in January 2016, as the chart below shows. However, it’s rather a coincidence as the more detailed analysis

does not show the positive correlation between the gold prices and the interest in the Zika virus. For example, the latter plunged in March, but gold prices did not – there was a correction, but not a plunge. And despite the downward trend in the number of cases and the interest in the Zika virus, the price of gold generally was going upwards until September

hawkishFOMC meeting. Gold’s performance was driven more by the macroeconomic evens such as the introduction of the

NIRP by the

Bank of Japan in January 2016.

Chart 4: Gold prices during Zika pandemic (London P.M. Fix, in $).

Summing up,

gold does not always react positively to pandemics. In some cases (MERS and Ebola), the price of the yellow metal even declined! It confirms our view that in the long-run,

geopolitical drivers and all sorts of natural disasters are less important to the gold market than macroeconomic or fundamental factors. Gold is especially unmoved when the

epidemic is geographically contained and it does not affect significantly the developed countries and the world’s economy. As we often repeat, geopolitical events move the gold market the most significantly when they affect directly the US or the global economy.

Thus, our historical analysis implies that the current outbreak of

COVID-19does not have to provide a sustained rally in the gold prices. Of course, this time may be different. This is because the new coronavirus originated in

China, which is now an important part of the global economy and a major industrial center strongly linked through the supply chains with the US and European companies. But investors should not give in to fear – although in previous

pandemics the

stock market always plunged initially, it quickly gave way to a recovery and significant gains. It implies that the recent shift towards the

safe-havens assets such as gold may reverse later in the future… unless the

Fed chickens out and eases its

monetary policy, which – given the recent spread of the coronavirus to the Europe and the US – has become more likely.

If you enjoyed the above analysis and would you like to know more about the links between the coronavirus epidemic and the gold market, we invite you to read the March

Market Overview report. If you’re interested in the detailed price analysis and price projections with targets, we invite you to sign up for our

Gold & Silver Trading Alerts. If you’re not ready to subscribe yet and are not on our gold mailing list yet, we urge you to sign up. It’s free and if you don’t like it, you can easily unsubscribe.

Sign up today!

Thank you.

Arkadiusz Sieron, PhD

Sunshine Profits – Effective Investments Through Diligence and Care

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Trading Alerts.