- Valeo Pharma Inc. is a Canadian specialty pharmaceutical company with big pharma capabilities while retaining small company flexibilities. Valeo is a fast-growing revenue generating company with a strong product portfolio and a robust product pipeline.

Valeo Pharma Inc. (CSE: VPH) is a fully integrated specialty pharmaceutical company focused on in-licensing prescription drugs for the Canadian market. The Company acquires the Canadian rights from international drug manufacturers wanting access to the Canadian markets without the hassle. Valeo is not a developer of drugs (thus no big R&D expenditure and risk), it does everything that a big pharmaceutical company does after it develops a drug, to make it a commercial success. Valeo maintains, in-house, all the necessary capabilities and infrastructure to register and manage a drug through all stages of commercialization. Valeo focuses its efforts on commercial stage, innovative and proprietary drugs targeting three therapeutic areas; 1) Neurodegenerative diseases, 2) Oncology, and 3) Hospital Specialty Products. Valeo targets areas where it can be highly impactful marketing-wise with a limited/streamlined sales team (e.g. of the ~900 neurologists in Canada, less than 10% are the key initiators of initial prescriptions). The Company has recently added proprietary branded-products with significant growth potential that are expected to dramatically increase revenues. Its pipeline over the coming months and years should see additional robust growth as the Company's goal of becoming a dominant player in its targeted therapeutic fields is increasingly realized.

Shares of Valero Pharma Inc. trade on the Canadian Securities Exchange under the symbol

VPH (began trading in February 2019). Looking at price-to-sales ratio metrics relative to the coming pipeline, shares of VPH are expected to experience solid price appreciation as revenue projections come to fruition, and certainly higher as news develops regarding additions to the pipeline.

Valeo is set to achieve breakeven this 2020, and accelerate revenue-wise from there; revenues are projected to go from ~$10M in 2020 to near $90M within a couple years based on the existing and fast growing product pipeline with the help of two recent product additions; 1) ONSTRYV®, the 1st Parkinson's Disease treatment launched in Canada since 2006 (now approved in Canada, marketing underway with access incrementally coming online), and 2) REDESCA®, a low molecular weight heparin biosimilar used to prevent deep vein thrombosis and pulmonary embolism (scheduled for approval in Canada in Fall 2020, with marketing beginning in early 2021).

Growing Portfolio of Products

Valeo currently markets

5 products including:

•

Onstryv®:

Launched July 2019, estimated peak sales of

$8M - $12M/annum.

•

Ondansetron ODT:

Q4-2010 launch, estimated peak sales of

$2M - $3M/annum.

•

M-Eslon®:

Estimated peak sales of

$7M - $8M/annum.

Valeo expects

4 more product launches in the coming quarters:

•

AmetopTM:

Q3-2020 launch, estimated peak sales of

$1M - $2M/annum.

•

Yondelis®:

Q4-2020 launch, estimated peak sales of

$2M - $4M/annum.

•

Sodium Ethacrynate:

Q4-2020 launch, estimated peak sales of

$1M - $2M/annum.

•

Redesca®:

Q1-2021 launch, estimated peak sales of

$30M - $40M/annum.

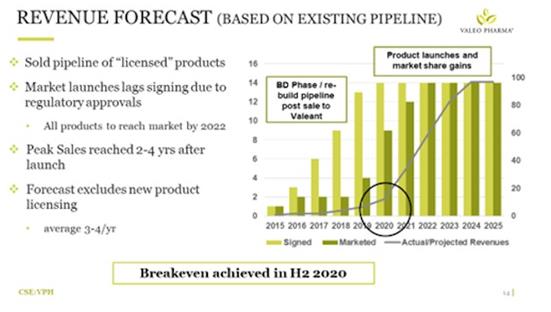

Revenue Forecast - Based on existing pipeline

Figure 1. (above) - Revenue forecast from existing pipeline

Figure 1. (above) - Revenue forecast from existing pipeline (sourced from recent Company presentation). Even thru the recent COVID-19 pandemic we expect Valeo's sales to continue rising, and manufacturers of its products to remain in production -- Valeo has extended lead times, and the sales teams are looking forward to getting back to more traditional physician interactions.

The projections seen above are presented with strong confidence; since Valeo does not have R&D (as it's m.o. is to source existing drugs developed and approved outside of Canada), it substitutes R&D for enhanced BD (Business Development), scientific research, and financial modeling to ensure its has a proper fit for access and success in the Canadian marketplace well before a deal is inked.

The clear objective is to become a $100M+ company based just upon what products Valeo already has now and in-licensing activities anticipated within the next 3 - 4 years. There are other opportunities, such as product acquisitions, that are not yet factored-in that can get Valeo there quicker and get it higher in terms of revenues. There are a lot of initiatives already underway that should make for some really good catalysts and milestones leading to stock appreciation.

Valeo is "the Little Big Pharma"; All the big pharma capabilities, with all the small company flexibilities.

- Experienced management with value creation track record.

- One of the few fully integrated specialty pharma companies.

- National sales force covering all key prescribing MDs.

- Derisked growth: Commercial stage products, no R&D risks.

- Significant insider ownership means full alignment with shareholders.

- Product Mix of BASE (non-branded products, recurring revenues) and GROWTH products (proprietary branded products with growth potential in Neurology/CNS, Oncology, Hospital Specialty).

Valeo does not take development risk, it focuses on drugs that are either approved in some jurisdictions (USA and / or EU) or have very strong clinical data that are about to be approved in these jurisdictions. Today you see Valeo Pharma Inc. much more robust in terms of product pipeline than a year ago, even 6 months ago, and if you compare again in another 6 months, Valeo will have advanced again. Valeo has an efficient internal business development team with an eye for picking the right product at the right time. The head of business development is Jeff Skinner, based in Toronto, and there is support in Montreal which comes from a team of scientific and financial analysts. Once a drug candidate is identified, the team finds out everything it can about that drug and the competition; e.g. what is filed, what is registered with the regulatory authorities (FDA, EMA, Health Canada) for clinical trials, if there any other drugs that are two or three years out, etc... all information is compiled along with a financial model to determine if Valeo can make money (ROI) selling that drug. In Canada the price of drugs are negotiated with the provincial bodies and they effectively determine what price Valeo can sell at. The modeling Valeo does is augmented with outside market access specialists and involves determining what price they believe the provincial bodies will accept, and based on that price Valeo must determine if there is any money in it given the expenses it will need to incur to in-license that drug.

As of May -2020 Valeo Pharma Inc. has 32 employees. The Company covers all aspects that a drug manufacturer is looking for in an effective pharmaceutical company to in-license within Canada; Valeo prepares all the technical binders, electronic filings, and correspondences for registration, facilitates regulatory efficacy and safety testing, negotiating access and approval for provincial government(s) reimbursement, warehousing, monitoring of reportable events, sales, and marketing to physicians.

On the sales front Valeo maintains a core team across Canada, along with a medical sales liaison. Valeo focuses on products that can be marketed to a small group of physicians and/or buyers for maximum impact. A good example of this is its Onstryv® Parkinson's Disease medication; there are only ~900 neurologists in Canada, of which ~225 specialize in Parkinson's, and with only 75 key opinion leaders responsible for initiating greater than 50% of prescriptions. The key is the initiating, because once a prescription has been 'initiated' by a specialist, the G.P. generally continues to renew the prescription afterwards. The marketing and sales team develops strong relationships with key opinion leaders and senior physicians in specific targeted therapeutic area.

Valeo's Canadian in-licensing abilities are increasingly getting noticed. Valeo's business development activities scour basically Europe, US, and Asia looking for new chemical entities or drugs that fit within its business model, often targeting the smaller and mid-size drug developers globally. There is a lot of research going on globally by smaller developers in areas that do not meet the multi-billion+ dollar financial criteria of major Pharmaceutical companies. Again, looking at ONSTRYV® for example, the overall Parkinson's Disease market in Canada is growing, its currently ~$100M, and there has been no new drug in recent times. In-fact, Valeo's ONSTRYV® is the first oral application in 14 years launched in Canada. The Valeo Business Development team vets a lot of drugs, few make the cut, either they are not a good fit, or the financial threshold does not make sense. Once Valeo zeros-in and identifies a prospect worth perusing, it has a very good chance of landing it in the end as Valeo is nimble, has a proven track record, and has all the infrastructure and elements necessary for the success of everyone involved.

------ ------ ------ ------ ------ ------

History of Valeo Pharma Inc.

2003 - 2014: Valeo Pharma Inc. 1.0

- Founded in 2003. Focused on dermatology and hospital products.

- Sold entire product portfolio to Valeant in 2014 for $26 million, a 350% return to shareholders.

2015 - 2018: Valeo Pharma Inc. 2.0

- Focused on three therapeutic areas: neurology/CNS, oncology and hospital specialty products.

2019 - 2020:

- Listed on Canadian Securities Exchange (February 2019).

- Launched ONSTRYV® for Parkinson’s Disease (July 2019). National sales force in place. Received positive recommendation for public reimbursement in Quebec.

- $5.5 million total financings secured.

- Revenues grew to $6.6M in 2019 from $4.4M in 2018, a 50% increase.

- Licensed REDESCA®, a low molecular weight heparin biosimilar used to prevent deep vein thrombosis and pulmonary embolism.

- Licensed YONDELIS® from PharmaMar for soft tissue sarcoma.

- Licensed AMETOP™ from Alliance Pharma, hospital anesthetic.

Note:Valeo Pharma Inc. 2.0 is majority owned by strong hands looking to dwarf the success of Valeo Pharma Inc. 1.0: Valeo Pharma Inc. was essentially rebooted as a new entity in 2015 after its original portfolio was sold to Valeant for C$26 million, representing a 350% return to shareholders, a ROR ROI based on the present value of shareholders investments over a period of years that works out to an after tax return in the high-30% range on an annualized basis. Some refer to Valeo Pharma Inc. 1.0 as the Company pre-2015, and Valeo Pharma Inc. 2.0 thereafter which has the same management leadership groupteam leadership. Valeo Pharma's CEO, Steve Saviuk, originally cofounded the Company with a couple of passive (retired) ex-pharma professionals. The same marketing, sales, regulatory, and commercial team that built Valeo Pharma Inc. 1.0 is the same team that is involved now. After the product line sale in 2014 to Valeant, a few of the older shareholders cashed out, and the Company brought in some new shareholders from the management team. As a result, the

management, insiders, and directors own ~75% of the company currently, making them perfectly aligned with all other shareholders.

------ ------ ------ ------ ------ ------

The Two Business Sides of Valeo Pharma Inc. -- 1) The BASE & 2) The GROWTH

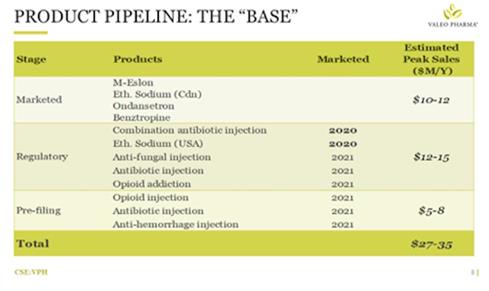

1) The BASE is characterized by non-branded products generating recurring revenues. Valeo Pharma has within its family a division that handles generic products, mostly all dedicated to hospitals, primarily injectable products. This division is almost a continuation of what the Company did under Valeo Pharma 1.0, before it sold its product line to Valeant. In 1.0 Valeo Pharma had some of these products, the Company knows how to do it, and it fits in with its business model, because in hospital environments the more products you have the more visibility you have. So having these smaller niche products keeps the Valeo name in front of the group purchasing agents. The BASE products require relatively low sales and marketing spending. This division will continue to grow, the Company plans to add two to three products a year. These are products that can do ~$500,000 to $2M - $3M each.

- Does not require “boots on the ground” sales force.

- Very limited spending to generate steady & recurring cash flows.

- Provides downside protection and risk mitigation.

Figure 2. (above) The BASE

Figure 2. (above) The BASE product line.

2) The GROWTH are proprietary branded products with significant growth potential in: Neurology/CNS, Oncology, and Hospital Specialty. The growth is where the blue sky potential is.

- Targeting innovative products with $5M to $40M peak sales.

- In licensing products that are at commercial stage.

- Greater sales potential & higher margins.

Figure 3. (above) The GROWTH

Figure 3. (above) The GROWTH product line.

Synopsis of key near-term GROWTH product revenue drivers

GROWTH:

ONSTRYV®, Launched July 10, 2019

- New oral treatment for Parkinson’s Disease ("PD").

- 1st PD launched in Canada since 2006.

- 2nd Most common chronic neurodegenerative disorder after Alzheimer.

- 100,000 Canadians diagnosed with PD (160,000 patients estimated for 2031).

- ONSTRYV® has been approved and launched in the EU and USA.

- Supported by Valeo’s National Sales Force.

- Received positive recommendation for public reimbursement in Quebec.

- 35 Movement Disorder Clinics, including 70 Key Opinion Leaders (KOLs) responsible for 75 % of scripts.

- Peak sales estimate $8M - $12M/annum, sales margin 65% - 70%.

ONSTRYV® sales should really start kicking in the second half of 2020. We note Quebec has already agreed to reimbursement of the drug.

------ ------ ------ ------ ------ ------

GROWTH:

AMETOP™, Expected launch Q3-2020

- Approved by Health Canada (DIN Transfer).

- Anesthesia of the skin prior to venepuncture or venous cannulation.

- Valeo direct sales force, leverages our expanding hospital portfolio.

- Peak sales estimate $1M - $2M, sales margin 50+%.

------ ------ ------ ------ ------ ------

GROWTH:

YONDELIS® (ORPHAN DRUG), Expected launch Q4 2020

- Approved by Health Canada (DIN Transfer).

- Soft tissue sarcoma (STS).

- Total addressable patient base < 500 annually.

- Limited physical call points, 20 30 specialized oncologists.

- Valeo direct sales force.

- Peak sales estimate $2M - $4M/annum, sales margin 55%.

Valeo is expected to start selling YONDELIS® in the late Summer-2020. Currently Valeo is doing all the regulatory tasks to switch the product over to its name from the Spanish manufacturer PharmaMar S.A.. We note the developer/manufacturer PharmaMar only deals in Oncology, and it could have gone with another Canadian agent but it has known Valeo now for 5 years on other products that were vetted and Valeo passed on. This product is licensed with J&J in the USA, however it was reallocated from the last licensee in Canada so that it can be offered better targeted attention (by Valeo).

------ ------ ------ ------ ------ ------

GROWTH:

REDESCA® (BIOSIMILAR), Expected launch Q1-2021

- Injectable Anti coagulant, initially prescribed in hospital (low molecular weight heparin biosimilar)

- First new entrant in 20 years into a $200 M market.

- Price advantage over existing products.

- Product is successfully marketed in the EU.

- Valeo’s Partner is the world largest Heparin manufacturer.

- Peak sales estimate $30M - $40M/annum, sales margin 55% - 60%.

There is a new wave/push in Canada to support biosimilars. Alberta and BC are mandating the use of biosimilars, and it is expected that Ontario and Quebec will follow suit very soon -- the cost savings are too enormous to ignore. The Provinces spend $billions on drugs every year, and biosimilars can often be ~25% - 50% cheaper. Biosimilars are the same as the biologic originals/competition, they are however created from a living organism and every lot fluctuates minutely, thus they are not identical and are treated like a new drug by Health Canada. The good part is Valeo does not have to do any clinical trials that the innovators have done, Valeo piggybacks on their trials. Valeo’s partner did perform clinical trials to show safety and efficacy; its trial involved 286 patients. REDESCA® should be approved in Fall-2020. Low molecular weight heparin is a fairly large market in Canada; it is a ~$200M+ market used in various common surgical procedures as an anticoagulant agent (e.g. hip replacements, knee replacements, cardiac procedures) and used increasingly in patients suffering from Covid-19. Valeo's REDESCA® will be the fourth player in the low molecular weight heparin market in Canada. With Valeo's REDESCA® entrance at a lower price, and biosimilar access across the spectrum of drugs being increasingly pushed by the Provinces, Valeo should capture a respectable share of the Canadian market. From a study Valeo pharma did, it estimates REDESCA® will be in the 25% - 35% range lower than the existing competition, and even in those ranges Valeo's margins will be ~50%. These are relatively inexpensive units, they are prefilled syringes, it is a volume business, we're talking the total market of ~15M/annum syringes in Canada. Valeo's manufacturer is very reliable, currently very active in Europe and Asia, it has the ability to manufacture ~400M syringes per year.

Also important to note is that the World Health Organization has as one of its guidelines for COVID-19 patient treatment the use of low molecular weight heparin to prevent complications resulting from the virus infection (

see related article here). There are also ongoing studies evaluating whether the use of low molecular weight heparin could also increase recovery time and decrease overall mortality related to COVID-19;

- The Italian Medicines Agency (AIFA) has given the green light to a new clinical study to reduce mortality from Covid-19: a group of patients will be administered the low molecular weight heparin anticoagulant in therapeutic doses (see related article here).

- Also see the following medical synopsis article entitled "Evidence is building linking anticoagulation to COVID-19 Survival"; among nearly 3000 patients with COVID-19 admitted to New York City's Mount Sinai Health System beginning in mid-March, median survival increased from 14 days to 21 days with the addition of anticoagulation low molecular weight heparin (see related article here).

For further DD on Valeo Pharma Inc. see the following URLs:

Corporate website:

https://www.valeopharma.com

Recent Technology Journal Review:

https://technologymarketwatch.com/vph.htm

##

Fredrick William, BA Ec.

Fredrick is a freelance information services professional and consultant to several financial publications, he monitors and invests in the resource, technology, consumer staples, healthcare, financial, energy, utilities, and biotechnology/pharmaceutical sectors.

***

Legal Notice / Disclaimer

This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment. The author has based this document on information obtained from sources he believes to be reliable but which has not been independently verified. The author makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of the author only and are subject to change without notice. The author assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission. Furthermore, the author assumes no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information provided within this Report.