AlexSava

Many investors are expecting the economy to be hit by a recession soon. Even the FED is implying that an economic downturn is possible in the second half of the year. Picking winners in such an environment is a challenging task. Obviously, some sectors are going to be hit harder than others and investors will be looking for safety. For that reason, I’ll generally avoid consumer discretionary industries. At the same time, the geopolitical environment is quite hostile with the dollar’s status as a reserve currency beginning to be challenged. This naturally puts my focus towards precious metals – in such environment their demand should go up. Within that space, I prefer gold, as it’s still considered a monetary metal and unlike silver its industrial use is more limited. However, within the gold sector, company characteristics matter. Any company that is short of funds and is looking for financing is not an optimal choice, as in a recession access to capital is more difficult. Free cash flow generating assets are a must, as internally generated funds are the best source of capital. A near-term production growth and significant exploration/development upside are the cherry on top. Obviously, valuation is an important factor, so ideally the company should be trading at considerable discount. Last but not least, having an experienced management team with skin in the game is also very valuable. Considering these criteria, I think that Aris Mining (OTCQX:TPRFF) should do especially well in a recession. I previously covered this company in Oct 2022.

The macro picture

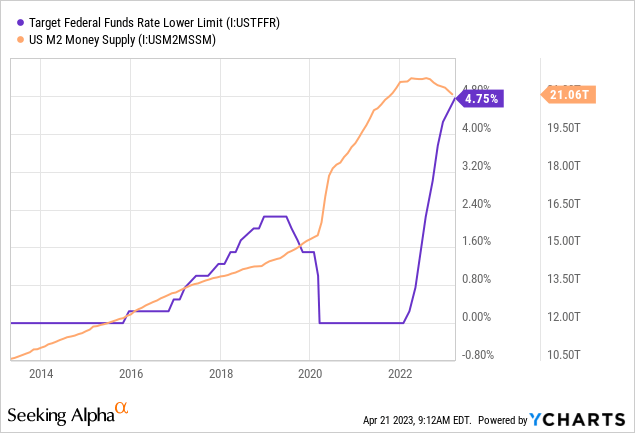

2022 has been an extraordinary year in many ways. Coming out of the pandemic-related lockdowns, the world was faced with raging inflation, which forced central banks to start increasing interest rates in a rapid manner. At the same time, the FED began shrinking its balance sheet. The M2 dynamic is also very telling of the tighter monetary conditions.

Data by YCharts

Data by YCharts

Rapidly raising interest rates resulted in eroding bond prices, which hit the balance sheets of financial institutions. As a result, many companies from the sector are recording losses and some had even worse faith, like the Silicon Valley Bank, which collapsed. Not surprisingly, lending activities slowed down.

On the geopolitical front, the Russian invasion in Ukraine raised the geopolitical tensions to unprecedented levels for the 21st century. The subsequent US-led sanctions, including exclusion of Russia from the SWIFT system, demonstrated that the dollar could be weaponized. In light of this, some countries are looking to reduce their dependence on the dollar. For example, Saudi Arabia signaled readiness to trade oil in currencies other than the dollar, breaking the USD multi-decade monopoly.

Gold is shaping as a winner

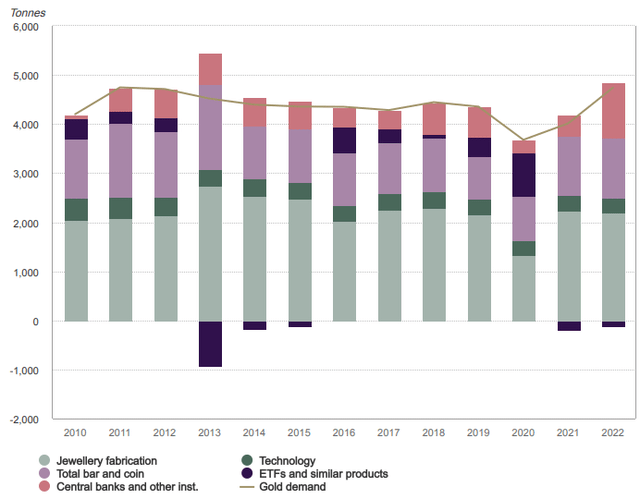

Gold demand (Metals Focus, Refinitiv GFMS, World Gold Council)

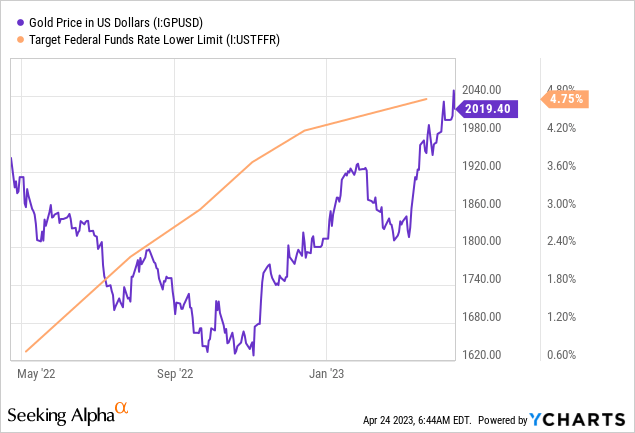

It’s no surprise that given the macro and geopolitical environment, central banks are looking to diversify their reserves. As a result, 2022 marked the highest amount of gold added to the central banks’ balance sheets on record – 1,136 tonnes (+152.4% YoY). In addition, investment demand was also quite strong, as market participants were looking for safety. Overall, gold demand reached 4,742 tonnes in 2022 (+18.2% YoY). This allowed gold to trend higher, despite the rapid raise of interest rates and break the usual inverse relationship.

Data by YCharts

Data by YCharts

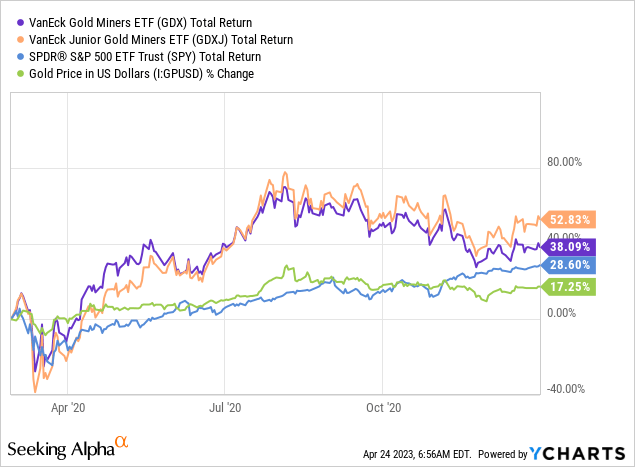

Miners could be a bigger winner

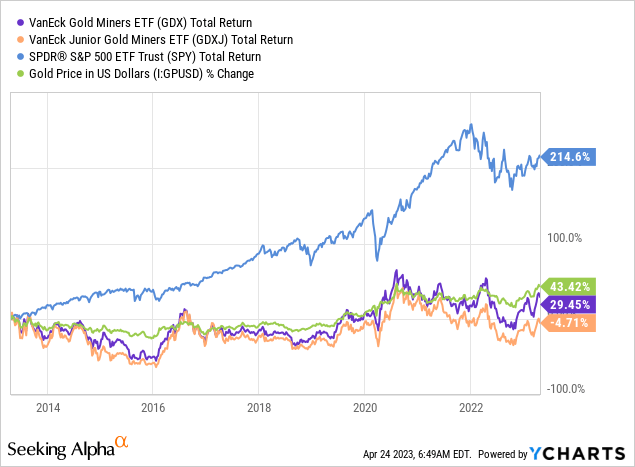

Commodity producers often offer leverage on the price of the commodity. In the case of gold, over a long-term, the miners represented by the VanEck Vectors Gold Miners ETF (GDX) and the VanEck Junior Gold Miners ETF (GDXJ) have both underperformed the return that the metal itself offers as well as the broad market, represented by the SPDR® S&P 500 Trust ETF (SPY).

Data by YCharts

Data by YCharts

However, in gold bull markets, things were exactly the opposite. The latest event of high uncertainty and increased recession risk – March 2020 demonstrates how things may unfold – while everything dropped initially, gold and especially the miners very quickly recovered and broke new highs.

Data by YCharts

Data by YCharts

Why Aris Mining?

One has to remember that not all companies within the gold mining space will benefit equally. So I considered some important factors on a micro-level and based on them, Aris Mining seemed to be a very good bet. Here are the factors:

Balance between production and exploration/development

When it comes to commodity producers, I like them to have some cash flow generating assets, but also having the potential to increase their production considerably on a relative basis. Giving an example, a 1Moz producer, putting 200koz project into operation will only increase its revenue by 20%, all else held equal. However, a 200koz producer adding the same project will double its production.

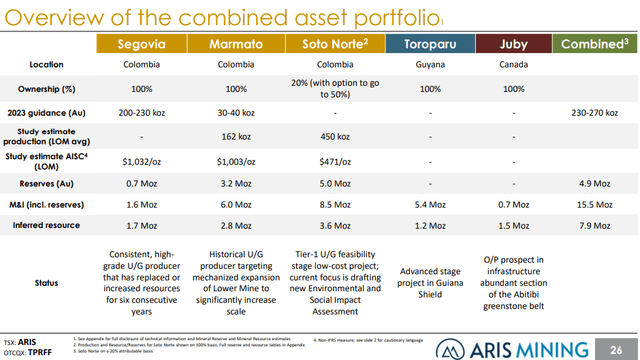

Asset portfolio (Aris Mining)

The portfolio of Aris Mining offers this balance, as the flagship operating project – Segovia produces slightly more than 210koz, while the company is currently expanding the other producing asset – Marmato from 30-40koz/year to 162koz LOM average production, by opening up the lower portion of the mine. On top of that, Aris holds interest in the prolific Soto Norte project and Toroparu in Guyana with both of which, total production may approach the 800koz level.

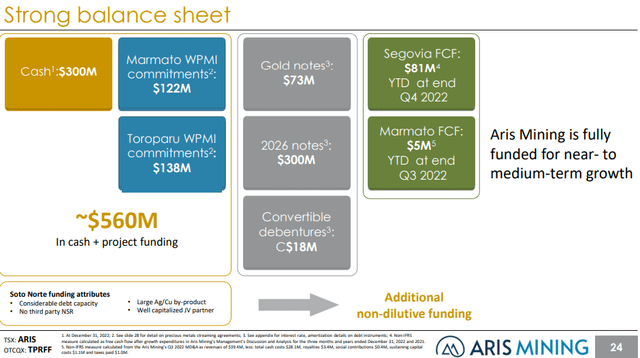

Strong financial position

In the current economic environment, capital is becoming more expensive and scarce. For that reason, any company that has to tap the financial markets in the near future will face challenges.

Financial position (Aris Mining)

In the case of Aris Mining, the company is well funded to complete the expansion of Marmato as only the cash available (US$300M) covers the estimated initial capital of the project (US$280M). On top of that, the Segovia mine is generating considerable free-cash flow (US$81M in 2022). Aris also has US$122M financing commitment from the royalty giant Wheaton Precious Metals (WPM), related to Marmato and US$138M for Toroparu.

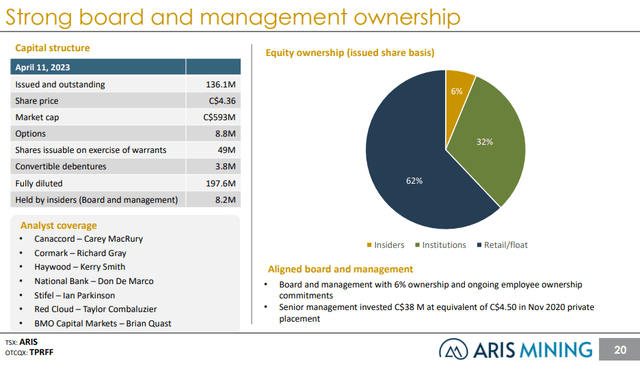

Experienced management with skin in the game

Ownership structure (Aris Mining)

Aris is led by a team of experienced mine-builders with multi-decade experience. The CEO – Neil Woodyer is a founder and former CEO of Endeavour Mining (OTCQX:EDVMF), while Ian Telfer, the former Chairman of Goldcorp, is on the Board of Directors. Insider ownership is at 6%, which is quite decent, especially if the fact that the majority of it was acquired in 2020 in a private placement at CAD$4.50/share and not received as bonuses.

Attractive valuation

Currently, the enterprise value of Aris Mining stands at around US$535M. At the same time, looking at the projects’ economics, the implied EV is more than 3x.

| Project | Assumed gold price (US$/oz) | after-tax NPV (US$M) | discount rate | Source |

| Segovia | 1800 | 241.6 | 5% | 2022 PFS |

| Marmato | 1800 | 533 | 5% | 2022 PFS |

| Toroparu | 1500 | 794 | 5% | 2021 PEA |

| Soto Norte | 200* | | |

| Implied EV | 1 768.6 | | |

* The Soto Norte valuation is based on the call option Aris Mining has

Even discarding the development stage Toroparu and Soto Norte, the company is still undervalued, especially as current gold prices are above the ones used in the technical reports. Also, I consider the estimated NPV of Segovia to be greatly underestimated as the resources of the mine, while looking low have been consistently replaced throughout the years.

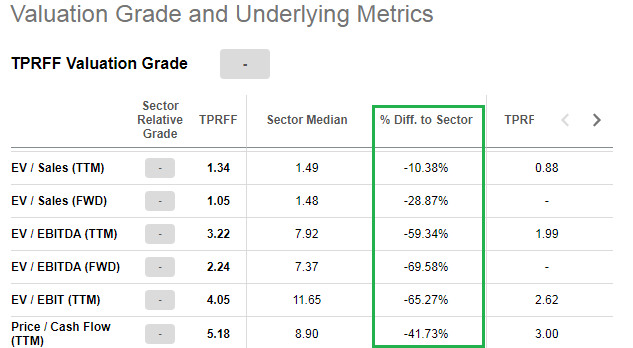

Aris Vs. the sector (Seeking Alpha)

Looking at some multiples, compared to the sector, Aris Mining also appears to trade at a discount, despite its great growth prospects, which are not reflected in current financials.

Risks

Political risk

Political risk is quite relevant for miners and Aris doesn’t make an exception. 3 out of the 4 main projects are in Colombia, where the new government was planning to tax gold exports. Fortunately, the idea was subsequently abandoned, but the bad taste of even entertaining it remains. However, the government also intends to unveil stricter environmental element in the mine permitting process, which may hurt miners. The Colombian president – Gustavo Petro has been against gold mining in the Pramo de Santurbn area, very close to which is located the Soto Norte project. So Aris may not be able to move forward in the project, has the stance of the current administration remains unchanged.

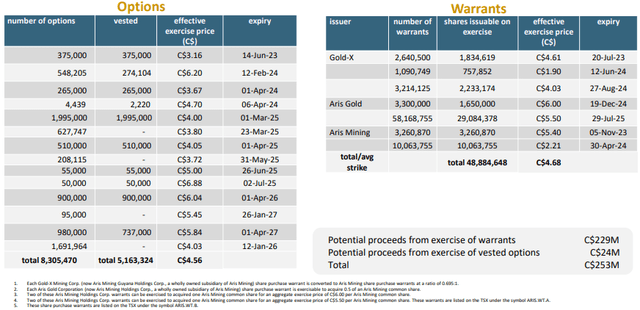

Dilution risk

While Aris Mining has a strong financial position and raising capital is quite unlikely, there are dilutive instruments as part of the capital structure.

Dilutive instruments (Aris Mining)

The good thing is that most of the warrants and options are exercisable at prices which are considerably above the current market price.

Conclusion

I expect gold demand to be not only unaffected, but to possibly increase even in recession scenario, given the geopolitical and macro environment. Gold miners could be a natural beneficiary of this and Aris Mining stands out of the herd. The company has cash flow producing assets and great development prospects within its portfolio. Aris is led by an experienced management team with considerable skin in the game. At the same time, currently Aris appears to be trading at a big discount to the indicated value of its projects and below the median multiples of the sector.

Editor's Note: This article was submitted as part of Seeking Alpha's Best Investment Idea For A Potential Recession competition, which runs through April 28. This competition is open to all users and contributors; click here to find out more and submit your article today!

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.