Falcor

We're nearly halfway through the Q1 Earnings Season for the Gold Miners Index (GDX) and one of the most recent companies to report its results was Equinox Gold (NYSE:EQX). While the headline results were not pretty with a moderate increase in output and sales volumes offset by a 5% increase in all-in sustaining costs [AISC], the company made meaningful progress on ensuring it can fund Greenstone without further share dilution, securing $140 million from a gold forward sale and prepay agreement, and additional proceeds from reducing its equity investments in i-80 Gold (IAUX) and Solaris Resources (OTCQB:SLSSF).

And although Equinox finished the quarter with one of the weakest balance sheets sector-wide and investors can continue to expect significant cash outflows until 2025 when Greenstone ramps up to commercial production, they can breathe a sigh of relief with ~$410 million in liquidity (excluding equity investments). Plus, Greenstone is tracking on budget and schedule, and its ability to deliver close to budget is aided by an all-star construction team in G Mining, a dip in fuel prices, and continued softness in the Canadian Dollar. That said, with the stock hugging resistance and no longer attractively, I see this rally to US$5.80 as an opportunity to book some profits.

Los Filos Operations (Company Website)

Q1 Production & Sales

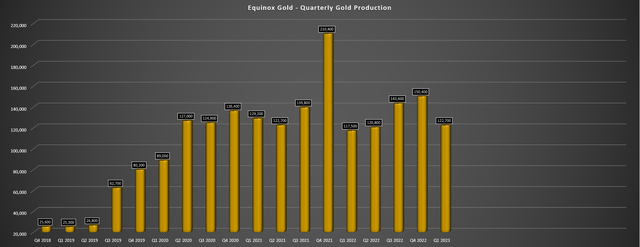

Equinox Gold released its Q1 results this week, reporting quarterly production of ~122,500 ounces of gold and sales of ~123,300 ounces. This translated to a 4% increase in output and sales vs. the year-ago period, and the company benefited from a higher average realized gold price of $1,895/oz, resulting in a 5% increase in revenue to $234.1 million. A better quarter from Los Filos, Aurizona, and Fazenda helped to drive the increase in production, with a further benefit from Santa Luz, a new mine in Brazil that did not contribute in the year-ago period. And with progressively higher production as the year progresses plus a higher gold price, we should see a further improvement in financial results sequentially.

Equinox - Quarterly Gold Production (Company Filings, Author's Chart)

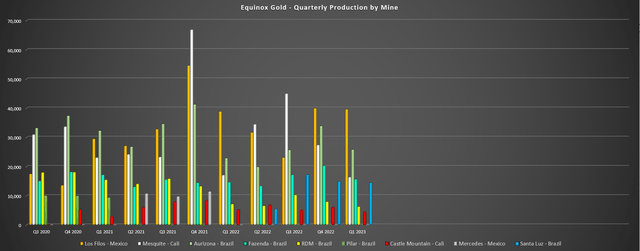

Looking at the chart of mine by mine production below, the best performers were Los Filos (~39,600 ounces), Aurizona (~25,800 ounces), and Fazenda (~15,700 ounces), though Aurizona's improved year-over-year performance was mostly related to easy year-over-year comps with just ~22,900 ounces produced in the year-ago period. Unfortunately, the higher production from these three mines combined with ~14,500 ounces from Santa Luz was offset by its lower-grade mines, Mesquite and Castle Mountain, which combined for just ~20,900 ounces in the period. This was down from ~22,300 ounces combined in Q1 2022, and RDM also had a rough quarter, with limited access to low-grade stockpiles due to permit delays, resulting in production of just ~6,400 ounces at all-in sustaining costs of $2,348/oz.

Equinox Gold - Quarterly Production by Mine (Company Filings, Author's Chart)

Although the overall production figure wasn't anything to write home about for a company with seven mines and Equinox continues to be spread quite thin, the company's 60% owned Greenstone Project will dramatically change its production profile, and output should improve at existing assets as the year progresses. This will include more normalized production at RDM following a production stoppage in January, slightly higher production at Castle Mountain which looks more likely to deliver into the low end of guidance (25,000 ounces vs. 30,000 ounces), and slightly higher production from Los Filos with a more delayed leach cycle because of higher copper content in the ore which impacted recoveries.

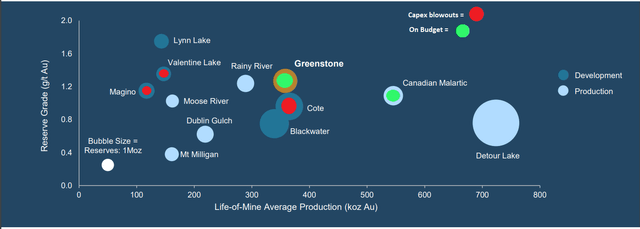

And as for Greenstone, Equinox reaffirmed the very positive news that the project remains on budget and schedule, a massive deviation from what we've seen at other Ontario greenfields projects which saw considerable capex blowouts, like Cote Gold and Magino. The combination of construction costs tracking towards budget with bolstered liquidity (gold prepay/forward sales and sale of equity investments) has significantly improved Equinox's financial position, as has the higher gold price, which is improving its cash flow generation despite its ~$1,600/oz cost profile in 2023/2024, partially offsetting the significant growth capital heading out the door that's being spent at Greenstone.

Open Pit Mines in Canada (Production/Construction/Development) (Company Presentation, Author's Notes)

As of quarter-end, Equinox had ~$410 million in liquidity between cash and remaining capital on its revolving credit facility with $400 million in financial, operating and capital commitments in the next twelve months. However, this doesn't include ~$130 million of marketable securities and the company has additional on its At-The-Market Equity Program. The good news is that while Equinox was forced to use its ATM to improve its financial position and this led to ~1.2% share dilution (fully diluted basis) with ~4.4 million shares sold at US$3.88, the higher gold price should save it from having to make any additional share sales, and it's also able to keep its portfolio intact vs. IAMGOLD (IAG) that dumped multiple assets to ensure it could complete its share of Cote Gold construction.

Costs & Margins

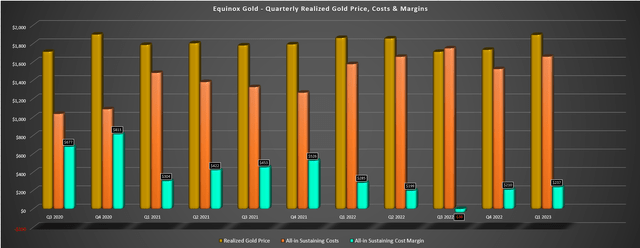

Moving over to costs and margins, we saw another quarter of meaningful cost increases, with cash costs up over 10% to $1,376/oz (Q1 2022: $1,237/oz), and AISC soaring to $1,658/oz, up over 5% year-over-year. And this was despite a slight tailwind from 12% lower sustaining capital in the period vs. Q1 2022 levels. That said, the company should benefit from slightly lower unit costs as the year progresses with a slight increase in sustaining capital spend being offset by higher production and sales volumes. So, while AISC have continued to climb and it would shock me to see Equinox's AISC come in below the guidance midpoint of $1,635/oz, the worst looks to be over from a margin compression standpoint.

Equinox Gold - Quarterly Realized Price, Costs & AISC Margins (Company Filings, Author's Chart)

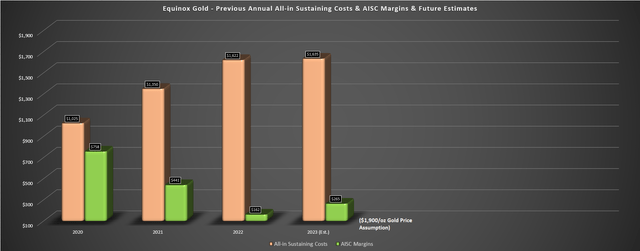

The good news is that while costs have risen and remain at some of the worst levels sector-wide, Equinox saw limited help from the gold price in Q1 2023 ($1,895/oz), resulting in AISC margins declining to $237/oz vs. $285/oz in Q1 2022. However, Equinox should benefit from an average realized gold price above $1,925/oz for the rest of the year when including the impact of hedges. And if we assume an average realized gold price of $1,900/oz for FY2023 to be conservative and give Equinox the benefit of the doubt and assume AISC of $1,635/oz, we would see an improvement in AISC margins year-over-year despite higher costs, with Equinox getting bailed out by the higher gold price.

Equinox Gold - Annual AISC, AISC Margins & Forward Estimates (Company Filings, Author's Chart & Guidance Midpoint)

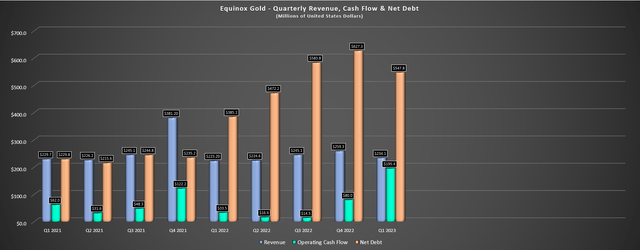

Finally, if we look at the company's financial results, cash flow improved to $195.4 million in the period, though this was because of the one-time benefit of a $139.5 million cash payment from its Gold Prepay arrangement. And while net debt was lower than I expected helped by better margins related to the higher gold price, it still stands at ~$548 million, up from ~$385 million in Q1 2022. That said, and as discussed above, while Equinox remains more leveraged than its peer group, the potential funding gap appears to be solved with recent actions taken to improve its liquidity position and solid performance by the construction team at Greenstone.

Equinox Gold - Quarterly Revenue, Cash Flow & Net Debt (Company Filings, Author's Chart)

While this is positive news and the recent move above $2,000/oz for the gold price should help Equinox to have a much better remainder of the year, the company will still see significant cash outflows over the next two years as it builds Greenstone. So, while this will be a cash cow for the company starting in 2025, it's possible that Equinox continues to underperform as it bleeds cash during Greenstone construction, even with the benefit of a $1,900/oz gold price. So, with several other producers returning capital to shareholders which boosts their total returns and generating significant free cash flow, I continue to see more attractive opportunities elsewhere in the sector. Let's look at Equinox's updated valuation:

Valuation & Technical Picture

Based on ~366 million fully diluted shares and a share price of US$5.65, Equinox is trading at a market cap of ~$2.07 billion, and an enterprise value of ~$2.62 billion. And while this might appear to be a reasonable valuation compared to other mid-tier and intermediate producers in the sector like Lundin Gold (OTCQX:LUGDF) and Alamos Gold (AGI) given the company's higher production profile (post-Greenstone), Equinox differs because it has a much higher operating cost profile, a much weaker balance sheet, and its only world-class asset is Greenstone, of which it owns 60%, while the other two companies have full ownership of world-class assets (Island Gold, Fruta Del Norte).

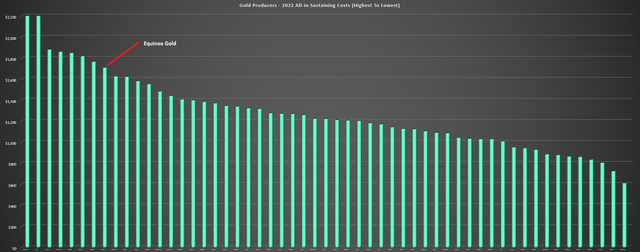

Gold Producers - 2022 AISC Ranked (Company Filings, Author's Chart)

Finally, although Equinox trades at a lower enterprise value relative to these two companies, both Alamos Gold and Lundin Gold are trading at what I would argue to be lofty valuations after doubling off their lows. So, from a relative value standpoint, it's difficult to compare Equinox to most other producers and I believe a discount is justified given its industry-lagging margins (even post Greenstone - $1,350/oz or higher). As for its valuation relative to net asset value, I continue to see Greenstone as fully valued from a P/NAV standpoint, with an estimated net asset value of ~$1.86 billion after subtracting out net debt and estimated future corporate G&A. This leaves the stock trading at a slight premium to net asset value currently, and I've found no value in paying a premium to net asset value for sector laggards and or high-cost producers.

Equinox Gold - Annual Revenue, Operating Expenses, Corporate G&A (Company Filings)

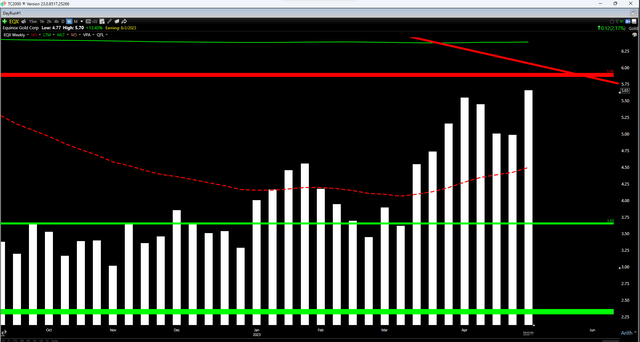

Finally, if we look at the technical picture, Equinox has rallied into a potentially strong resistance area and has no strong support until US$3.65. If we measure from a current share price of US$5.70, this translates to a reward/risk ratio of less than 0.10 to 1.0, a very unfavorable reward/risk ratio short-term. Obviously, a rising tide (gold price) could continue to lift all boats, and this would certainly benefit a lower-margin producer like Equinox. However, the time to buy to bet on a turnaround was below US$3.25, not after the stock has soared 130% off its lows.

EQX Weekly Chart (TC2000.com)

Summary

Equinox Gold has seen an improvement in its financial position thanks to recent sales of equity investments and a stronger gold price, and it's positioned to generate meaningful free cash flow in FY2025 once Greenstone is in commercial production if gold prices remain above $2,050/oz. That said, the stock looks to be fully valued here short-term, we're still over two years away from meaningful free cash flow generation as Greenstone will have a ramp-up period and the stock is now heading into a resistance area where it could become more vulnerable to a sharp correction. Hence, I would view any further strength in the stock above US$5.80 as an opportunity to book some profits.