TSX:QIPT - Post Discussion

Post by

best0be on Jun 25, 2024 8:42am

Interesting discussion on Breakout Investor

-

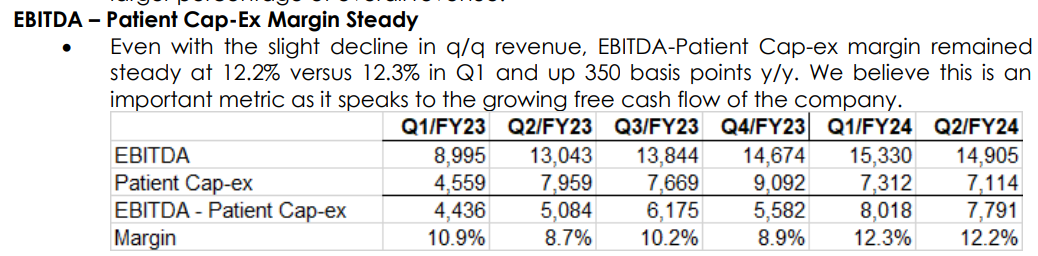

HOW TO VIEW AEBITDA

QIPT Analysts commentary: Expressing concern about its large capital expenditure spending on rental equipment business, Raymond James analyst Rahul Sarugaser lowered his recommendation for Quipt Home Medical Corp. (QIPT-Q, QIPT-T) to “underperform” from “market perform” previously. “In reviewing QIPT’s PPE schedule we note the regular transfer of inventory on its balance sheet to rental equipment (part of PPE),” he said. “We also note that this equipment has an exceptionally short average useful life of just over 12 months, and we view these rental equipment transfers effectively as Capex. QIPT finances the bulk of these purchases with equipment loans from financing partners, which are typically paid off over the life of the asset (~1 year). As such, payments on these loans are recorded as repayments of debt in the financing section of the cash flow statement, rather than as PPE purchases in the investing section. This could lead to an underestimate of the underlying Capex in the business. We do credit QIPT for now explicitly outlining its free cash flow; we further believe adj. EBITDA should also be adjusted to remove the depreciation on rental equipment from EBITDA, thus creating more alignment with the universe of cash-flowing companies, while also removing what is effectively a recurring cash charge given the short useful life of these assets.” TSX-listed shares of the Cincinnati-based home medical equipment provider plummeted 14.4 per cent ater it reported an adjusted earnings per share loss for its second quarter of 3 US cents, below the expectations of Mr. Sarugaser and the Street of profits of 2 US cents and 1 US cents, respectively. Cash on hand slid to US$14.6-million from US$18.3-million in the previous quarter. “We revise QIPT’s reported Adj. EBITDA for the amount of rental equipment depreciation in the respective period, which in turn drives a 2Q24 RJL Adj. EBITDA of $6.7-million (vs. QIPT reported Adj. EBITDA of $14.9-million),” said Mr. Sarugaser. “QIPT does not disclose rental equipment depreciation quarterly (only annually), so our deduction for the Q is an estimate. In addition, while QIPT’s new FCF disclosure now adjusts for the payments on any equipment loans used to finance equipment (QIPT’s interpretation of Capex), we believe the amount transferred from inventory is a better measure of Capex in this instance. This allows for the possibility that a portion of the inventory transfers are not financed, but rather paid for outright with cash (which we believe occurs in rare instances).” After reducing his earnings expectations, Mr. Sarugaser dropped his target for Quipt shares to US$2.50 from US$10.

-

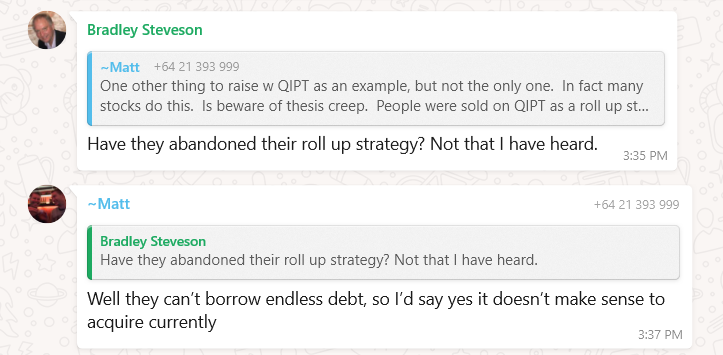

ROLLUP STRATEGY

Be the first to comment on this post