Toronto City Skyline at Night in Canada

Deejpilot/E+ via Getty Images

Note: All values are in CAD

The REIT

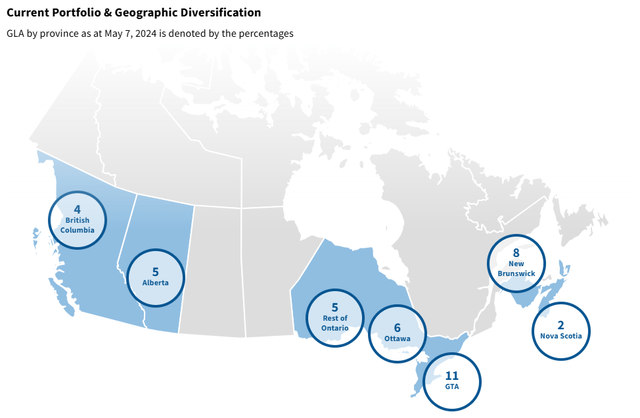

True North Commercial Real Estate Investment Trust (OTC:TUERF)(TSX:TNT.UN:CA) holds a portfolio of 41 office properties. These are located across Canada, in the provinces of British Columbia, Alberta, Ontario, New Brunswick and Nova Scotia.

True North REIT

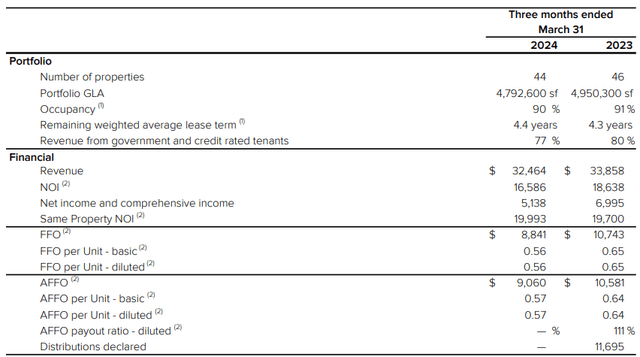

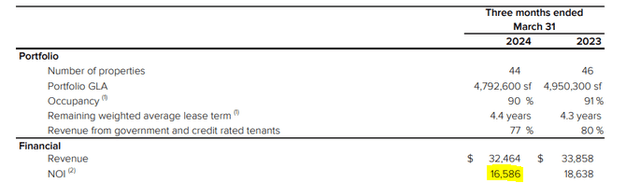

At the end of Q1, True North had 44 properties, 3 (Ontario) of which have been sold since then. Cumulatively, the properties enjoy a 90% occupancy and are predominantly occupied by government and credit rated tenants. This REIT's portfolio currently spans 4.7 million square feet in gross leasable area and is valued at around $1.3 billion.

True North REIT

Prior Coverage

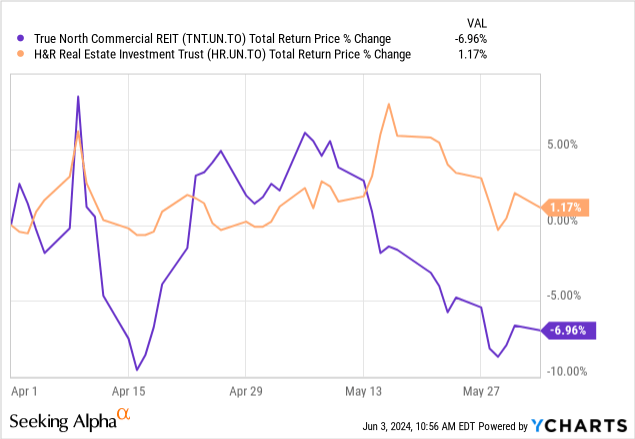

We covered the Q4 2024 results fairly recently and gave this REIT a neutral rating. The downward trending occupancy and adjusted funds from operations, or AFFO, astronomical leverage, rising interest costs and narrowing coverage, all played a hand in our outlook for True North at the time.

This business had just lost a major tenant in Calgary, Alberta, and we expected a 12X debt to EBITDA sooner rather than later. True North was selling assets to mitigate this, but we felt that the risks would outpace the deleveraging measures, and stayed on the sidelines. We noted that H&R REIT (OTCPK:HRUFF)(HR.UN:CA) was our REIT of choice for those interesting in playing the office rebound. While it has not made its unit holders rich, H&R has held up well versus our protagonist since then.

Data by YCharts

Data by YCharts

Today we will review the Q1 results and see if the metrics are travelling in the direction we had envisioned.

Q1 2024

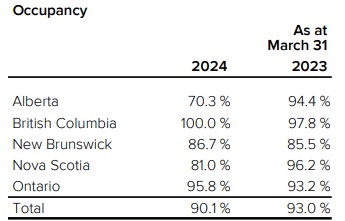

The best part of the transition from Q4-2023 to Q1-2024 was that the occupancy levels did not deteriorate further. At the end of the quarter we were at 90.1%, and that was a shade higher than the 89.2% we saw at the year-end of 2023.

Q1-2024 MD&A

One thing to keep in mind, though, is that there is a lot of asset turnover happening and those can distort the delta in occupancy levels. We actually had some more sales post Q1-2024 as well.

True North Commercial Real Estate Investment Trust (the "REIT") is pleased to announce it has completed the sale of two office properties for an aggregate sale price of $18.0 million (excluding transaction costs) totaling 70,700 square feet located at 251 Arvin Avenue, Hamilton, Ontario (the “Arvin Property”) and 6865 Century Avenue, Mississauga, Ontario (the “Century Property”). In addition, to the previously announced unconditional sale of 135 Hunter Street East, Hamilton, Ontario (the “Hunter Property”) for a sale price of $6.4 million that is expected to close on or about April 22, 2024, the REIT has entered into an unconditional agreement of purchase and sale to dispose of 9200 Glenlyon Parkway, Burnaby, British Columbia (the “Glenlyon Property”) for a sale price of $37.0 million that is expected to close on or about June 27, 2024. The four dispositions are being sold for an aggregate sale price of $61.4 million and is above its initial aggregate price of $56.8 million and above IFRS value as at December 31, 2023. The sales will generate estimated net proceeds of approximately $19.1 million which the REIT intends to use to repay existing indebtedness on its credit facility.

Source: True North.

As wonderful as that sounds, it does nothing to change the core thesis. The REIT will sell what it can in today's markets. It is not necessarily a reflection of where the rest of the portfolio would sell. Selling the best properties will also move the funds from operations ("FFO") meaningfully lower over time. You could see this in the total net operating income ("NOI") and FFO and adjusted FFO for Q1-2024. The latter two measures were down double digits.

Q1-2024 MD&A

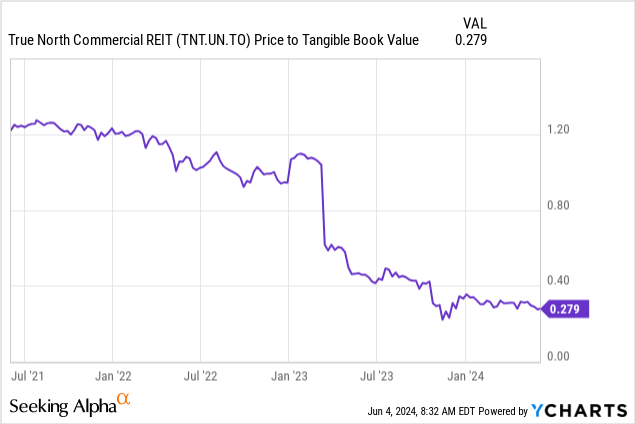

The REIT continued to use buybacks versus distributions, as the stock trades at a big discount to IFRS NAV.

Outlook

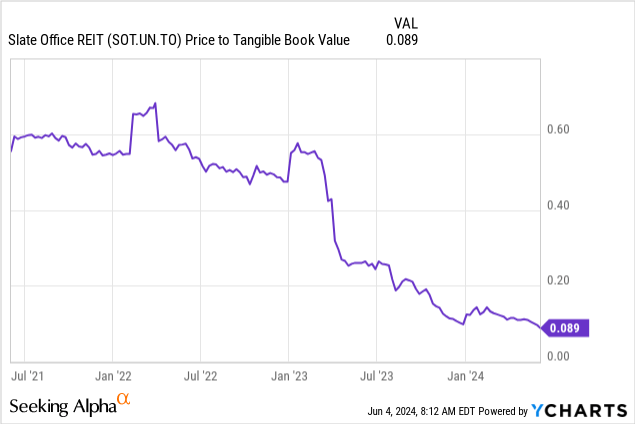

Let's start with Slate Office REIT (OTC:SLTTF)(SOT.UN:CA). We got some pushback when we said it was headed to zero, and the biggest argument was, well, the discount to NAV. If you loved it at 60% of NAV, you should be getting a second mortgage to buy this today.

Data by YCharts

Data by YCharts

That was, of course, a joke. That company is still destined for zero in our view and likely won't make it through the next 12 months.

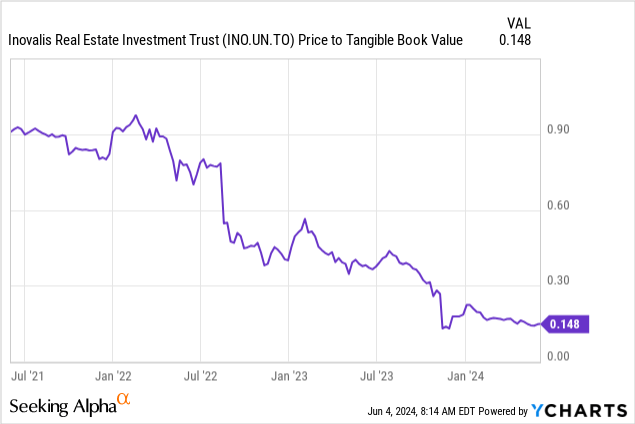

Inovalis REIT (OTC:IVREF)(INO.UN:CA) is another, though there is a slightly better chance that that one may get a little left for equity holders.

Data by YCharts

Data by YCharts

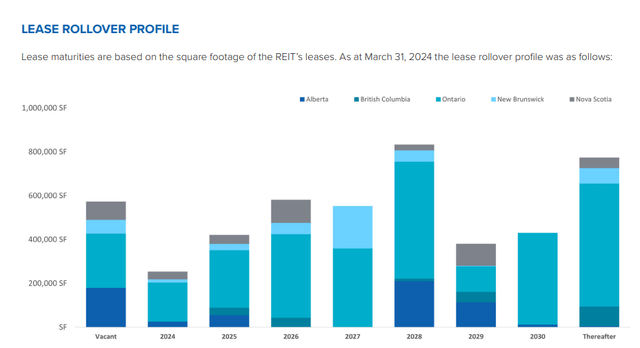

True North is no doubt miles ahead of the other two in some aspects. The occupancy levels are the critical differentiator. Both Slate and Inovalis saw the occupancy levels really tank in 2023. To the extent True North can hold this above 85% there is a fighting chance. It will be a tough battle with a weighted average lease length of 4.4 years.

Q1-2024 MD&A

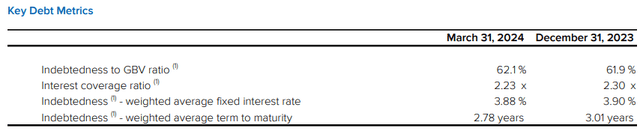

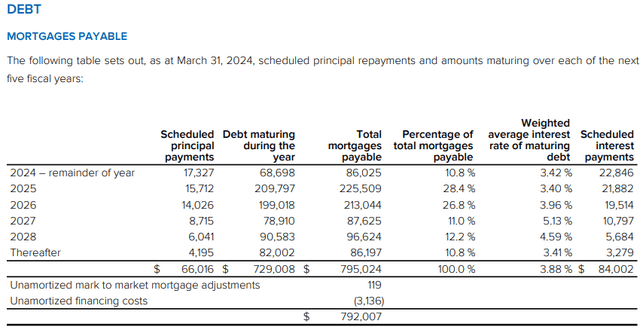

That of course does not mean that there are big returns to be had, even if True North succeeds. The other critical metrics are deep into the orange, if not the red, zone. Debt to gross book value is at 62.1%. This is despite so many asset sales. Interest coverage fell further this quarter. Weighted average term to maturity is just 2.78 years.

Q1-2024 MD&A

Just put side your bullish views and read the refinancing rate the REIT got this quarter (emphasis added).

During the quarter, the REIT refinanced $12,946 of mortgages with a weighted average fixed interest rate of 7.41% for a one year term which represents approximately 16% of mortgages maturing during the year with the majority of the remaining debt maturities occurring towards the end of 2024 on loans with large Canadian financial institutions with whom the REIT and Starlight have strong relationships.

Source: True North Financials.

There is close to $300 million coming due in the next 1.75 years (measured from end of March 2024).

Q1-2024 MD&A

Those mortgages are at the rock-bottom rate of 3.4%. Assuming we see similar rates of refinancing, you should see FFO drop about 30-40% just based on this. This would happen even if occupancy stayed flat, something we doubt.

Verdict

It does look cheap based on that IFRS NAV.

Data by YCharts

Data by YCharts

We don't believe that those properties as a whole can be unloaded anywhere near that price. We did not believe it for Slate, and we did not believe it for Inovalis. Likewise, we don't believe it for Dream Office (OTC:DRETF)(D.UN:CA) either. Alongside that, you have a NOI of about $66 million (16.58 million X 4).

Q1-2024 MD&A

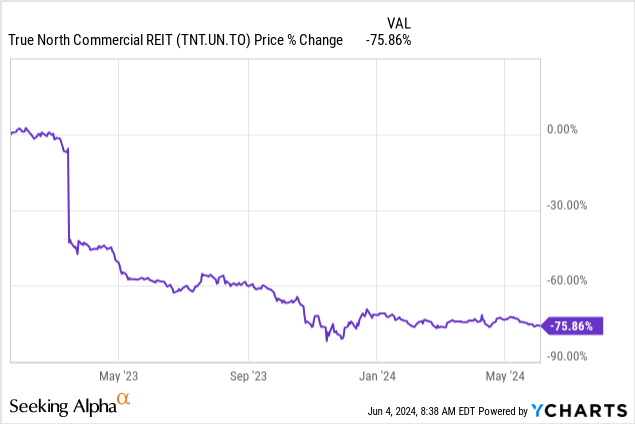

That supports the debt of close to $800 million. You generally don't want to be dancing with 12.5X debt to EBITDA levels in a distressed asset class. They seldom work out. Both Slate and Inovalis reached similar levels before going down. Dream Office is flirting with 11X. We remain skeptical that there is value in True North Commercial Real Estate Investment Trust and, so far, since our warning on the dividend, in January 2023, the stock is down 76%.

Data by YCharts

Data by YCharts

We owned three out of these four at one point and exited all in 2021. We haven't looked back. There are many beaten down REITs which are not suffering the same headwinds. We would look at them for value and stay out of True North.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.