Oleksii Liskonih/iStock via Getty Images

Agnico Eagle (NYSE:AEM) and Kirkland Lake Gold (KL) recently announcedan agreement to combine in a merger of equals, creating something the gold sector has never seen: A Canadian gold mining behemoth.

But this is about much more than just the amount of gold the company will produce, as the new AEM — the amalgamation will continue under Agnico Eagle name — checks off every other box as well.

I consider the new AEM a core holding in any gold mining portfolio; it's a must-own.

Why This Version Of Agnico Eagle Will Attract Significant Investor Interest

If I were to create the ideal gold mining company, it would be hard to ask for more than what the new AEM offers. Let's review:

1. A Top 3 Gold Mining Company

AEM/KL will be the third-largest gold producer in the world, both in terms of market cap and production. It's been Newmont (NEM) and Barrick (GOLD) at the top and nobody a close third vying for investors' dollars (especially at the institutional level), but the new AEM will be a powerhouse and will generate significant investor interest. Now, it's the trio of NEM, GOLD, and AEM that dominate this market. Two side notes, the graphs below (provided by AEM/KL) don't accurately depict the fourth and fifth largest gold companies in the world, as Polyus and AngloGold (AU) were omitted. That's irrelevant to Agnico Eagle's position on the list, but I wanted to clear up any confusion. Also, Franco-Nevada (FNV) has a larger market cap, but it's a gold royalty company — that has an oil and gas segment that accounts for a portion of its value — not a producer.

(Source: Agnico Eagle)

The new AEM is also forecasting gold production to increase to just under 3.5 million ounces in 2022 and then hit 3.6 million ounces in 2023, which will close the gap more with Barrick.

(Source: Agnico Eagle)

2. The Lowest Jurisdictional Risk Among Its Peers

While the new AEM will be the third-largest gold miner when the deal closes, it ranks as the best among the group when it comes to jurisdictional risk. 75% of production will come from Canada, with the rest from Australia, Finland, and Mexico. No company in this sector comes close to rivaling AEM's gold production capability combined with the low-risk regions where this gold is mined. ~2.5 million ounces of gold production will come from Canada, and that figure is growing. It's this heavy Canadian exposure that makes the new AEM stand out among its peers. I'm also glad to see Mexico become a smaller and smaller piece of the pie, as while the region is still pro-mining, companies are finding it tougher to operate in the country.

(Source: Agnico Eagle)

Newmont and Barrick each also mine about 2.5 million ounces of gold from their Canadian and U.S. assets, as their Nevada Gold Mines JV produces about 3.5 million ounces of gold per year, and they have other mines in the two countries. Canada has no natural jurisdictional risk advantage over the U.S., as they are considered equal (ignoring any tax advantages/disadvantages at the federal and state/province levels). However, when weighing the entire portfolio of producing assets, NEM and GOLD also have mines in Africa, the Dominican Republic, and other regions of the world that don't have the same risk profile as Canada and the U.S. It's the concentration of AEM's low-risk asset base that makes it stand head and shoulders above its larger rivals. That's something that institutional investors will likely reward.

3. Diversification Of Assets

How do you create a bulletproof company in this sector? Or at least one that's as close to that status as you can get? There are two key parts to the equation.

The first is to mine in low-risk regions.

Check.

The second is to have a well-diversified asset base with production coming from a wide range of mines.

Check again.

Mining is a tough business, and operations can underperform expectations (sometimes greatly). A well-diversified mining company can have other operations pick up the slack when one or two falter, substantially lowering any potential negative impact on production. Mining is no different than investing; diversification reduces risk in any portfolio.

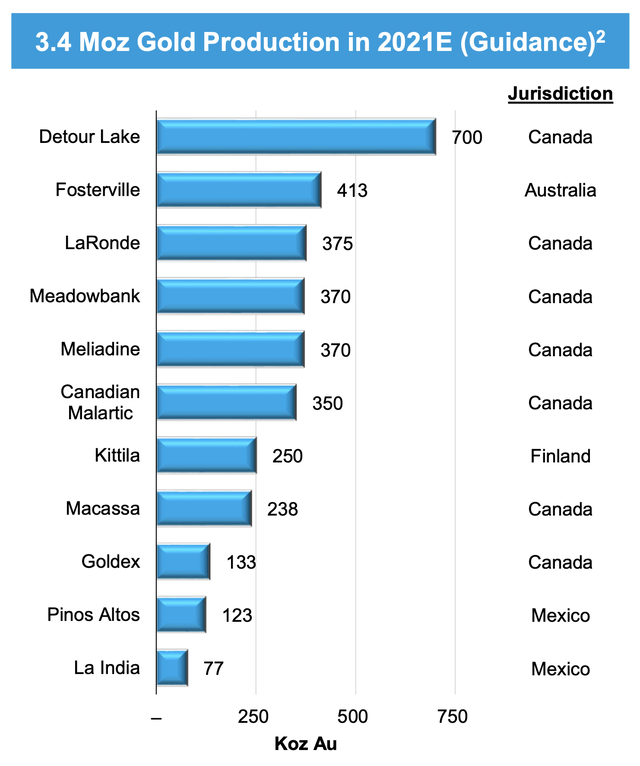

Below is a mine-by-mine breakdown of the combined company's production, along with jurisdiction. The Detour Lake mine in Canada will be the flagship operation producing 700,000 ounces in 2021 and increasing in future years, but there are a plethora of quality assets down the list that produce 350,000-400,000 ounces of gold. Fosterville's production has dropped this year as the high-grade ore is being quickly depleted, but it should remain stable at around 300,000-400,000 ounces over the next several years. Fosterville is the biggest wildcard in the portfolio, as exploration success could result in the mine reverting to a 600,000-700,000 ounce operation again, or production could continue to decline (more on this later). LaRonde (Quebec) and the Meadowbank and Meliadine assets in Nunavut, Canada, each produce 370,000-375,000 ounces of gold annually. A recent expansion at Kittila has taken production to 250,000+ ounces of gold. The mine has substantial reserves and a mine life that could take it to 2035, warranting another expansion in the future. Macassa is currently near the bottom of the list, but that operation will ramp up to 400,000 ounces over the next few years and could vault it to the #2 spot. Then, of course, there is Canadian Malartic, which produces 600,000-700,000 ounces of gold per annum. While AEM only owns 50% of Malartic, with Detour Lake in the portfolio, the company will still possess the two largest open-pit gold mines in Canada (which are also two of the largest open-pits in the world). Not shown is Agnico's newly acquired Hope Bay mine, which could ramp up to 200,000-300,000 ounces of gold.

(Source: Agnico Eagle)

While Detour Lake is ~2x the size of the other mines in the portfolio, it doesn't account for a disproportionate amount of overall production. The new AEM has a solid core group of 8 mines, each producing over 250,000 ounces of gold.

4. You want margins? We got margins.

The new AEM has some of the lowest AISC among the top producing gold miners, and a best-in-class cost structure out of all companies shown in the graph below. Only Polyus beats out Agnico Eagle on AISC when it comes to multi-million-ounce gold producers, which could be why Polyus wasn't included in the comparison. But there is no need to make AEM look better by omitting a lower-cost rival, as the operational metrics speak for themselves. The AISC comparison is also before taking into account any cost savings from the synergies created by the merger (which I will discuss later in this article). By the time Macassa ramps up to 400,000 ounces and Detour reaps the benefits of economies of scale, all assets will be fully integrated and synergies realized. I wouldn't be surprised if Agnico Eagle's average AISC was in the low to mid $800s by then. Out of all of the companies shown below, AEM has the greatest ability to lower its current cost structure even more, which would widen the cost gap between its rivals even further.

(Source: Agnico Eagle)

5. Stellar Leadership Team

Turnover at the CEO spot is common in the mining industry. Again, this gets back to the fact that "mining is a tough business," but 5-10 years ago, many gold companies made poor capital allocation decisions as the focus by the industry was on growth at any cost. Ironically, the "cost" for many of the CEOs was their jobs.

Only a few Chief Executive Officers in this industry have stood the test of time. Sean Boyd, CEO of Agnico Eagle, is one of them.

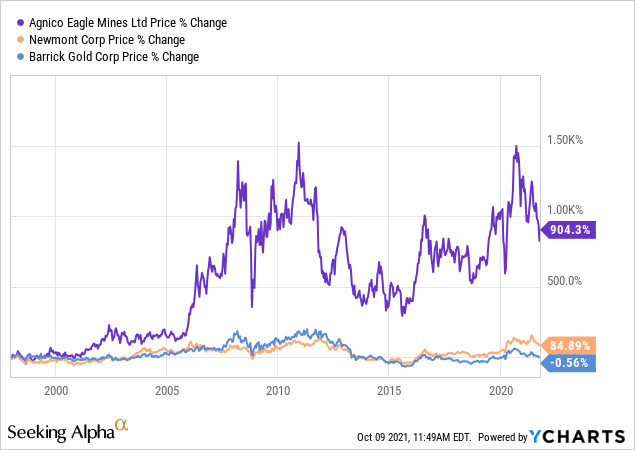

Boyd became CEO in 1998 and has taken AEM from a single asset producer to a 2 million ounce senior gold miner. Boyd's methodical approach to growing the company over the last two decades has delivered substantial shareholder value, something that NEM and GOLD have failed to do.

Data by YCharts

Data by YCharts Tony Makuch, CEO of Kirkland Lake Gold, has only been at the company's helm for the last five years, but after he came on board, KL acquired Newmarket Gold, and with it, the transformational Fosterville mine. The growth of Fosterville took Kirkland Lake to heights that few companies in this sector have obtained.

In 2019, Makuch used his very valuable currency to acquire the highly undervalued Detour Gold. As a Detour shareholder at the time, I considered this a coup. Makuch knew the value of the Detour Lake mine and what it would become one day. He had the foresight to use Fosterville's success as a springboard to create even more shareholder value. It was the right acquisition at exactly the right time.

You have two highly successful gold mining CEOs, and usually in a merger like this, one doesn't stay. But the new leadership structure of AEM will be a seamless transition that retains both leaders, as Boyd is moving to the Executive Chair position, while Makuch will become the CEO. It's the best of both worlds and a winning outcome for shareholders.

Had KL merged with Newmont or Barrick, Makuch had zero chance of becoming CEO, as Tom Palmer took over the top spot at Newmont less than two years ago, and it's highly unlikely that Mark Bristow (CEO of Barrick) would ever agree to relinquish his position, especially since it seems he is only getting started with his plans for Barrick.

By merging with Agnico Eagle, Makuch gets to lead an even larger gold mining entity and has Sean Boyd still presiding over the company's Board.

This job is Makuch's to have for a very long time, providing he executes.

Synergies Of The Merger

Other than the 5 points listed above, this merger also makes complete sense synergistically, as so many of Kirkland's and Agnico's operations in Ontario and Quebec are within close proximity to each other. You have AEM's Canadian Malartic, LaRonde, and Goldex mines on the same gold belt as KL's Macassa, Holt, and Detour Lake mines. AEM and KL are consolidating major gold camps, not unlike what Newmont and Barrick did in 2019 when they formed the Nevada Gold Mines joint venture. One of the benefits of this AEM/KL merger is the US$2 billion in pre-tax synergies expected to be realized over the next decade, the majority of which will be from operational synergies at the mines shown on the map below.

(Source: Agnico Eagle)

As for a breakdown of those synergies, the company expects to save ~$35 million a year by streamlining corporate costs, $130 million a year by the unification of mining operations and other operational synergies, and expects an additional $590 million of cash flow over the next 10 years via strategic optimization of the business.

(Source: Agnico Eagle)

I'm always a bit skeptical when I read about synergies and the expected cost savings in a merger, as typically, it's a selling point to try and get shareholders on board. Whether the actual figure is $2 billion or much less, this deal will still have substantial cost savings. Removing redundancy alone (at the corporate and operational levels) should result in far more annual cash flow.

The Biggest Risks For The New AEM

When I analyze the new AEM, I keep asking myself rhetorically: "where are the weaknesses?"

There aren't many.

The biggest risks that I see are:

1. The news flow on Detour Lake has been extremely positive lately. Case in point, Kirkland Lake Gold announced a 10 million ounce increase in the mine's resources last month.

I've been researching the mining sector for a long time, and a 10 million ounce increase in resources for a mine currently in production is an extremely rare event.

Let's break this down, though, because all ounces aren't created equal.

M&I Resources at Detour Lake have increased to 14.7 million ounces of gold, 10.1 million ounces more than the end of 2020 resource estimate. About 2.5 million of these ounces are low-grade (0.42 g/t), which would generally be counted as waste. You can see these ounces in the last several rows of the chart below. I highlighted the area to focus on, which is the M&I resources in the Main and West pits, which saw a net gain of ~7.5 million ounces of gold. The grade of the ounces in the Main pit declined to 1.07 g/t, but that's still above the reserve grade. The grade of the West pit stayed flat at 0.88 g/t, but this is below the reserve grade.

(Source: Kirkland Lake Gold)

The majority of these ounces are located within the Saddle Zone, which is between the West pit and Main pit. I'm not surprised that the company added significant ounces to the resource base — as they were drilling heavily in this area and expected to see a sizable jump given the drill results — but the amount of ounces added still greatly exceeded targets.

(Source: Kirkland Lake Gold)

However, there are many unanswered questions about these ounces and how they will impact the mine plan. For example, at what depths are the new ounces located, and what will be the strip ratio? Given the data released so far, a significant portion of the additional resources are 300+ meters below the surface and likely won't be mined anytime soon (maybe not until the next decade).

I see this resource update as having a longer-term impact (i.e., substantial mine life extension, past the current 20+ year LOM). Although, it's possible that some of these ounces could help fill in the gap in years 2027-2029, where production dips.

(Source: Kirkland Lake Gold)

It's also possible that this massive increase in resources could allow the new AEM to expand output and get Detour Lake up to 1 million ounces of gold per annum over a 10-15 year period. However, that would require additional capital, take years to implement, and depend on many factors.

There is a lot of work to be done to come up with a new mine plan.

Either way, this update is extremely bullish long-term for the mine. But I must admit, an update like this sets expectations very high for Detour Lake.

Kirkland Lake is already forecasting a drastic decline in the average AISC at Detour Lake to just $775 per ounce from 2021-2025 (the mine's AISC has been over $1,000 per ounce for the last 5 years). Then they added 10 million ounces more into the mix.

There is a risk that Detour Lake will not hit targets, and expectations are too optimistic. Even if that is the case, Detour Lake would still be a world-class mine.

2. Kirkland Lake had to throttle back production at Fosterville to buy more time on the exploration front. If they can't find more high-grade reserves (say above 15-20 g/t) over the next few years, the operation effectively hits a wall by 2024-2025. Output would drop to 100,000-200,000 ounces, and costs would soar. That would mean a ~10% dip in production post-2023, although that's a gap that could possibly be filled over the next few years.

(Source: Kirkland Lake Gold)

A Fair Deal For Both Sets Of Shareholders

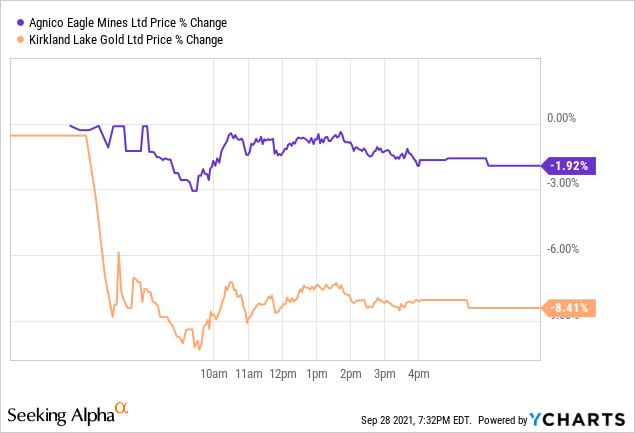

KL tanked 8% the day of the merger news, while AEM only fell 2%. That's because rumors swirled a few trading days leading up to the news, and investors bid up KL in anticipation of receiving a premium. Since this was almost a zero premium merger, the decline was simply KL getting back in line with AEM. I was surprised that investors bought KL on this rumor thinking that a substantial premium would be realized, as that hasn't been the trend in this sector over the last few years. Curiously enough, KL was still trading at about a $1 premium to the terms of the deal by the close that day.

Data by YCharts

Data by YCharts Of course, you have many Kirkland Lake shareholders complaining that they aren't getting a fair deal. My response to that is, don't listen to any investor making these complaints, as most of them said the same thing when Kirkland Lake bought Detour Gold. Ironically, the Detour Gold acquisition is what saved Kirkland's stock price from collapsing over the last 6-12 months, as the company reset expectations lower on Fosterville. I warned this would happen, and well in advance too.

As I said in December 2019, when KL tanked after it announced it was buying Detour:

The consensus opinion on this deal - and why KL was eviscerated - is that it's atrocious for Kirkland Lake, as it is a low-cost producer, and Detour's $1,100+ AISC will be a drag on margins. This is a highly flawed argument. Most "analysis" I have seen on this acquisition shows a severe lack of understanding of both of these stories.

It's actually the other way around: this deal is superb for Kirkland Lake, and KL shareholders should be thrilled. Detour Gold shareholders are the ones that should be voicing their displeasure.

The writing was on the wall. Fosterville was quickly running out of bonanza grade ore, and reserve grade and output would plummet in a matter of just 3-4 years.

Detour Lake is now the flagship operation for KL, and Fosterville is on the decline. Enough said.

My advice, trust that Makuch is making the right decision for KL shareholders; he certainly seems to know what he is doing.

I see this as a fair deal for both sets of shareholders. But you have to look at all of the moving pieces to get a complete picture. Something I don't believe many KL shareholders against the deal are doing.

You can't just look at the short-term production outlook to determine fair valuation; that was the grave mistake many KL investors made a few years ago when Fosterville was at its peak.

Agnico Eagle and Kirkland Lake Gold shareholders will own approximately 54% and 46% of the combined company, respectively. Yet AEM is bringing slightly more than 54% of the production, cash flow, and resources to the table. Looking out 3-4 years, unless there's exploration success at Fosterville, it seems likely that Agnico Eagle's assets will contribute to an even greater percentage of production and cash flow than they are today.

AEM also has a much more valuable project portfolio that includes Hope Bay, Upper Beaver, and Hammond Reef.

Where are the facts that support a premium for KL is warranted in this merger? When you weigh all of the variables, I see a fair deal for both sets of shareholders.

Investors need to look at the big picture. Both stocks trade at a premium, and combined, that premium should be even higher. Which is another reason why this deal makes sense.

I think investors will warm up to this merger because of how attractive it is and what is being created. There is nothing else like it on the market