Prices are in US$. GLTA

Up front, I got The Stars Group (TSG) wrong. I passed on the stock at $14+ back in August (and $16+ earlier this year). Worries about execution, worldwide poker growth, and a Sky Bet acquisition that increasingly looked like an overpay all contributed to my (somewhat moderate) skepticism toward the stock.

TSG now is above $20 - and at the risk of sounding cavalier, I'm not terribly surprised. The enormous leverage on the balance sheet, combined with regulatory uncertainty surrounding iGaming in the United Kingdom and sports betting in the U.S., made pinning down fair value of the equity difficult. I wrote in August that the stock was cheap - and noted the path to extraordinary upside if the company could deliver from an operational standpoint.

All that said, at no point did I see the path to upside coming from a merger. Yet that's exactly what's happened, as Flutter Entertainment (OTC:PDYPF) (OTCPK:PDYPY) and Stars Group are merging in an all-stock deal. And it's a deal that, on its face, makes a ton of sense. It's the pinnacle of the consolidation that has marked the UK market, in particular, for the past few years. It fixes Stars' balance sheet problem. Flutter management has been top-notch, mitigating some of the concerns about Stars management in recent quarters. And it provides some needed diversification for Flutter, whose profits have been hit over the past six quarters by regulatory and tax changes in the UK and Australia.

Indeed, the market sees the deal as a smart one. TSG shares have soared, owing to a premium built into the stock consideration. But Flutter stock also has gained about 7% since the merger was announced, continuing a nice bounce from multi-year lows reached earlier this year.

What's interesting about the acquisition is that the bull case for Flutter (which trades on the London exchange as well, symbol FLTR) seems quite similar to that of TSG before the deal. The pillars of the case - deleveraging, US sports betting, diversification away from poker - are the same, if the importance has somewhat changed. And so even after the 35% gain for TSG shares in the last four sessions, the underlying story isn't all that different. Investors who loved TSG at $15 still should love it at $20 - and those of us who were skeptical likely will remain on the sidelines.

Why The Deal Makes Sense

The Flutter-Stars deal is the apotheosis of the trend in online gambling over the past few years. Consolidation has been rampant since the UK's point of consumption tax was announced back in 2014. Indeed, both companies already had made significant acquisitions. What was then Paddy Power acquired exchange operator Betfair in early 2016, and a majority stake in U.S. daily fantasy sports operator FanDuel last year. The Stars Group picked up the UK's Sky Betting & Gaming last year in a $4.7 billion deal, only a few months after buying William Hill's (OTCPK:WIMHF) (OTCPK:WIMHY) Australian operations.

Other operators, too, raced to build scale to manage the impact of higher taxes. GVC Holdings (OTCPK:GMVHF) bought bwin.party Digital Entertainment and Ladbrokes (the latter of which had merged with Gala Coral). Kindred acquired 32Red. William Hill bought Mr Green.

Obviously, none of these deals was anything like this one, which creates the world's largest iGaming operator. But in the context of the race for size, the tie-up makes sense. Broader trends aside, there's still an obvious logic here. Fundamentally, the merger makes a great deal of sense relative to the respective capital structures.

Flutter's relatively clean balance sheet - net debt was 0.8x trailing twelve-month EBITDA as of Q2, according to the company's interim results - can take on Stars' $5.2 billion in gross debt. Stars with 5x+ leveraged even on a net basis; the combined company should have a net leverage ratio closer to 3.5x, with plans to get that figure into Flutter's targeted range of 1-2x in the mid-term.

On the acquisition call, management cited the ability to lower finance costs, a potentially material benefit: Stars guided for $280-$290 million in cash interest expense in 2019 in its Q2 release. Most of that expense is coming from a ~$3.5 billion term loan and $1 billion in senior notes which have weighted average interest rate above 6%. The combined company certainly can lower that rate. £140 million ($172 million) in annual cost synergies, due to be realized in full by year three, should further help free cash flow and deleveraging.

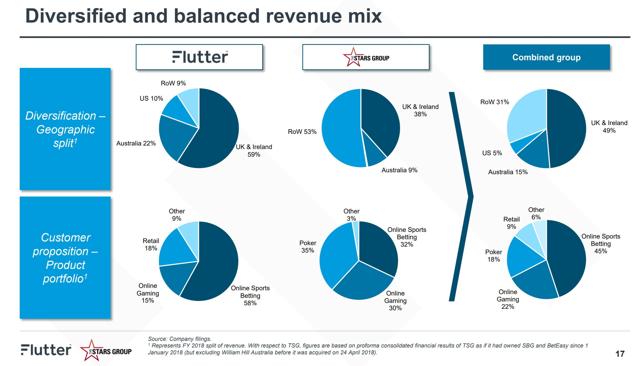

Strategically, too, there's a logic to the deal. Indeed, the logic is much like those made by Stars itself. The Sky deal, in particular, diversified Stars away from the stagnant poker business. Combined with Flutter, poker drops to ~18% of revenue:

source: Flutter acquisition presentation

source: Flutter acquisition presentation

In other words, poker becomes a stable profit center and a customer acquisition channel - not the growth driver it simply can't be anymore.

Like the Stars-Sky tie-up, there are cross-selling opportunities here. Stars can help Betfair expand out of its primarily UK/Ireland base. And of course, the combination creates the undisputed leader in the burgeoning U.S. sports betting market. FanDuel had 50% market share in New Jersey in the first half of 2019, according to Flutter's interim report. Stars is a bit late to that state, but its FOX Bet joint venture with Fox (FOX) (FOXA) is now live and partnerships with Eldorado Resorts (ERI) gives Stars access to additional states as they bring sports betting on board.

As a UK analyst told the Financial Times, there are basically four companies at the head of U.S. sports betting right now: FOX Bet, FanDuel, William Hill, and 365Bet. Flutter will own two of them - and keep both going, given its multi-brand strategy worldwide. (Minority owners also will have a say: Flutter is giving reciprocal ownership in both FOX Bet and FanDuel to its partners. As Flutter CEO Peter Jackson put it on the call, this was done to avoid potential "favorite child" complaints from either side.)

The combined company will be a leader in the UK & Ireland, a significant competitor in Australia to the large incumbent, a "podium position" operator elsewhere, and the lead dog in U.S. sports betting. That's a hugely attractive proposition strategically, while the interest expense and synergy potential suggest further benefits from a fundamental standpoint. So it's not hard to see why the market has reacted well to the acquisition.

Does The Deal Go Through?

That said, it's worth noting that the merger isn't guaranteed to go through. Indeed, a reasonably hefty spread remains. The exchange ratio of 0.2253 Flutter shares per TSG share suggests TSG would be worth, based on the current Flutter price in London, $22.60. Monday's close of $20.60 leaves a hefty spread near 10%, even considering Flutter expects to deal to close in Q2/Q3 2020.

There are some potential stumbling blocks. Half of Flutter shareholders need to approve the deal, which admittedly seems likely given the initial market reaction. Two-thirds of Stars shareholders similarly have to vote in favor - which could be a bit trickier, given the stock traded at $35+ last year. Still, the nearly 50% ownership of the combined company, and the logic of the acquisition, suggests that shareholder approval is likely.

The bigger challenge could be on the antitrust front, particularly in the UK and Australia. It's worth noting that in both countries, unlike the U.S., the impact on competitors, not just consumers, is a major factor in antitrust review: indeed, the regulatory agencies in both countries have the word 'competition' in their title. As Bloomberg noted, the deal is a bet against antitrust regulation. The combined company would have ~35% market share in online sports betting in the UK, according to an analyst on the acquisition call, and would be a clear second to Tabcorp (OTCPK:TACBY) in Australia.

That said, the deal should be able to go through. Lawyers in the UK believe the deal will be approved, according to Gambling Compliance. It's hard to imagine U.S. authorities denying the deal, given the inability (at the moment) to prove deleterious effects on consumers, and the wealth of options available in existing markets like New Jersey. Flutter might have to divest one of the Australian assets in a worst-case scenario, but it does seem at the moment like the deal is likely to go through. (In fact, though it's outside of my comfort zone, long TSG/short FLTR trade is somewhat intriguing, particularly because the post-deal response to FLTR suggests its shares, too, would fall if the deal broke.)

Valuation and the Echo of TSG

Assuming the deal is completed, it's interesting to note that the case for FLTR will be quite similar to that for TSG. There's a deleveraging component: TSG planned to get from 5x+ to under 4x, while Flutter is aiming for sub-2x against the pro forma ~3.5x. Obviously, the US sports betting opportunity is a bigger part of the FLTR case, albeit against a larger equity valuation (~$14.4 billion pro forma, at the moment). Stars saw great success in cross-selling casino and sports betting products to its existing player base; Flutter will do the same, even if it has no plans to market across brands, according to commentary on the acquisition call.

That said, the risks aren't necessarily all that different, either. The combined company, thanks to Stars' ownership of Sky Bet, will have almost half its revenue coming from the UK & Ireland, and another 15% from Australia. UK and Australia tax hikes already have pressured earnings for both companies: Flutter's Underlying (i.e., adjusted) EBITDA was flat last year and down 10% in the first half of 2019 thanks largely due to increased taxes in both markets. (Those figures exclude initial losses behind the US opportunity.) Stars Group saw similar cost pressure, and the midpoint of its 2019 guidance actually suggests a modest decline in profitability as well.

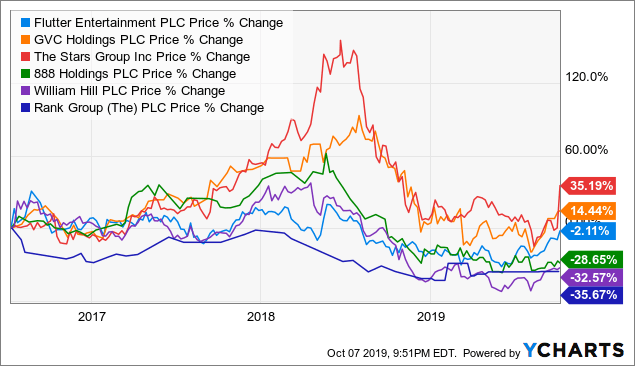

And there's always the risk in M&A of a deal performing worse in practice than it looks on paper. That's particularly true in iGaming. While it's been the case that the PoC regulations in the UK spurred M&A, that M&A hasn't done all that much for the acquirers:

Data by YCharts

Data by YCharts

Acquisitions so far have proven at best to be defensive: minimizing the effects of further tax and regulatory pressure, instead of actually driving value through cost and revenue synergies. With almost two-thirds of revenue coming from the UK, Ireland, and Australia, and another 18% from unregulated (or 'grey') markets, there's an obvious risk that pattern will play out again.

Meanwhile, the combined company isn't cheap. Pro forma EV/EBITDA sits at 13.7x, based on the companies' respective 2019 EBITDA outlooks. Even incorporating synergies (and the cost of implementing those synergies), the multiple only gets to ~12.6x. That's a hefty premium to other players in the space. GVC Holdings (OTCPK:GMVHF) trades at just under 10x EBITDA, based on 2019 guidance. 888 Holdings (OTCPK:EIHDF), which mostly has been left out of the M&A trend, is at 7x+. William Hill is at 8x.

Investors right now are paying a significant premium for Flutter. To be fair, on its face, that's not a bad idea. Flutter, particularly in its Paddy Power days, historically received the highest EV/EBITDA multiple in the space (often above 15x). And, again, the 14x current and 12x+ pro forma multiples incorporate zero contribution from the U.S., an opportunity which has real value.

But that brings us back to the idea that FLTR looks an awful lot like TSG did. Much of the case for the stock, particularly after the recent gains (and assuming the acquisition goes through) is based on the U.S. opportunity. And I'm not yet convinced that opportunity is what Flutter/Stars bulls - or management - quite believe.

Admittedly, states have moved faster than I thought they would when I expressed my skepticism toward the industry last year. But we've still seen high tax rates in states like Illinois and Pennsylvania, which will significantly limit profitability. Take rates for sports betting are much lower than for other forms of gambling. Competition is going to be intense, and profits will be shared with land-based operators like Eldorado and back-end technology operators as well.

But other investors may well - and do - see it differently. And at the moment, TSG is probably the best play on the thesis that sports betting is going to drive billions of dollars in annual profits. The tie-up makes sense. Flutter is going to be the leader in the space, at least in the early going, in a market that is going to have only a few leaders and where it's going to be close to impossible to catch up.

And so the price change in TSG doesn't really change the case all that much: the story is still much the same. The market cap might double in the deal; but with the addition of FanDuel, so has exposure to U.S. sports betting. The risks in the UK are amplified, but that's offset by a lower exposure to a poker business that has turned negative in recent quarters. Rewards probably are somewhat lower: I wrote in August that TSG potentially could quadruple in a blue-sky scenario. But that upside came in part due to hefty balance sheet leverage: spreading that debt across incremental EBITDA also de-risks the story as well.

I personally am not confident enough in the U.S. opportunity to offset concerns about U.K. regulatory activity (and the near-term effects of Brexit) plus a reasonably hefty valuation. But it's worth repeating: other investors might well see it differently. For those investors, TSG was probably the most attractive direct play on U.S. sports betting. After the merger, it still is.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.