Oselote

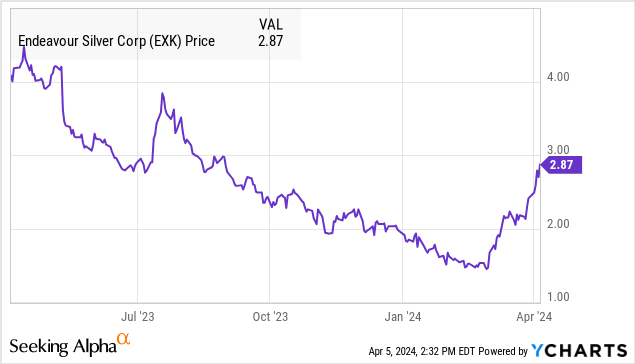

Endeavour Silver Corp (NYSE:EXK) (TSX:EDR:CA) has emerged as one of the best-performing precious metals miners this year amid the ongoing surge in the price of gold and silver. Shares have more than doubled from their Q1 low, rebounding sharply compared to the volatile and challenging 2023.

We see room for the momentum to continue with several catalysts to propel EXK higher. Notably, the expectation of the company's new "Terronera" mine to come online later this year is set to drive significant growth. In our view, EXK is a must-own stock in the silver mining space.

Data by YCharts

Data by YCharts EXK Financials Recap

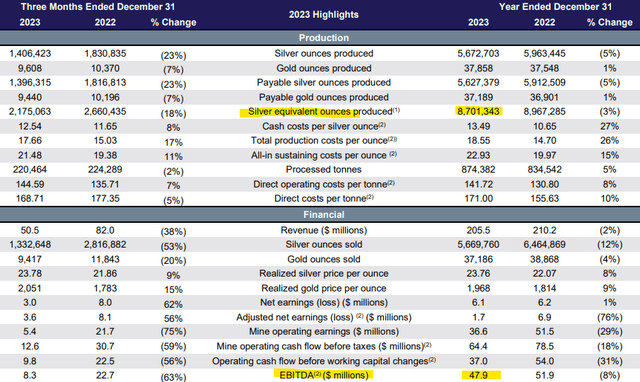

EXK reported its Q4 earnings in March with adjusted EPS of $0.02, down from $0.04 in the period last year in what can be described as a transitional quarter. Endeavour's 2023 output was impacted by some planned maintenance at its flagship Guanacevi Mine.

Even as the 2.2 million in silver equivalent ((AgEq)) ounces produced was down by -18% y/y, there was a 16% sequential rebound compared to Q3. For the full year 2023, total AgEq production was down a modest -3% y/y, with a similar -2% drop in total full-year revenue of $206 million.

A theme for the company that explains the large selloff in shares going back to 2021 has been inflationary cost pressures impacting margins. 2023 EBITDA of $47.9 million was down by -8% from $51.9 million in 2022. That said, Q4 saw an improvement in the all-in AgEq sustaining cost per ounce to $21.48, below the full-year average of $22.93.

source: company IR

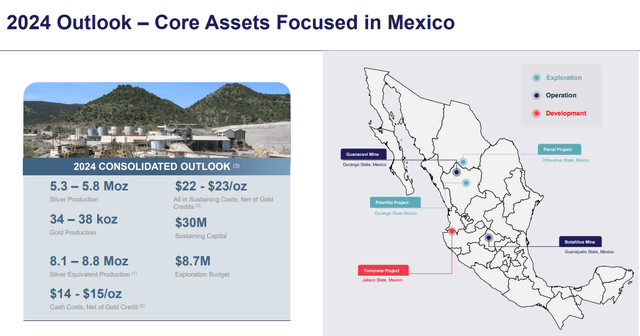

Management notes that its core operation has seen some productivity improvements into the early part of the new year working into its updated guidance.

Management expects 8.1 to 8.8 million ounces of AgEq production for 2024 which is in the range of 8.7 million results for 2023. The target for an all-in sustaining cost between $22 and $23 per AgEq ounce represents a favorable decline at the midpoint compared to $22.93 last year.

source: company IR

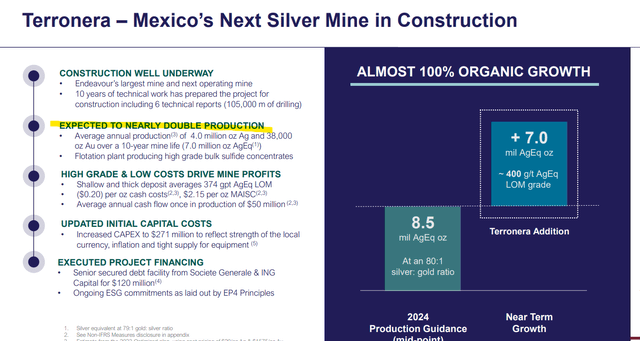

Terronera Set to Begin Production By Q4 2024

The bigger story here is the anticipation for the initial production of Endeavour's newest "Terronera" expected by Q4 this year. The latest update is a 43% construction completion with a larger portion of the $170 million capital commitment already spent in what has been a 10-year planning process.

In our view, the project represents a game-changer for the company, expected to nearly double the current production by adding 7 million AgEq ounces in annual output. Keep in mind that the company has other assets in development with future growth potential.

source: company IR

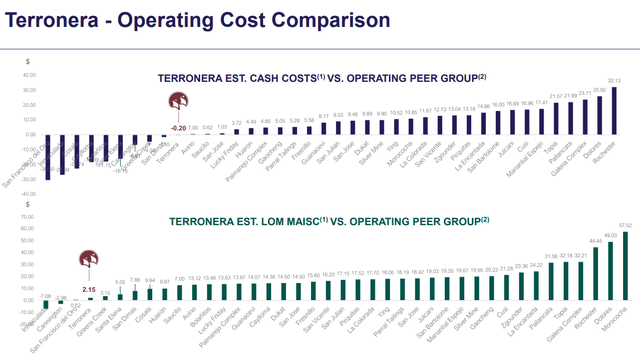

The other dynamic here is that Terronera at capacity is set to deliver exceptionally low cash cost of production relative to Endeavour's global silver miners peer group. The life-of-mine site all-in-sustaining costs "LOM MAISC" is estimated to be $2.15 per ounce, highlighting the significant profitability impact that can be expected into 2025 and beyond.

source: company IR

What's Next For EXK?

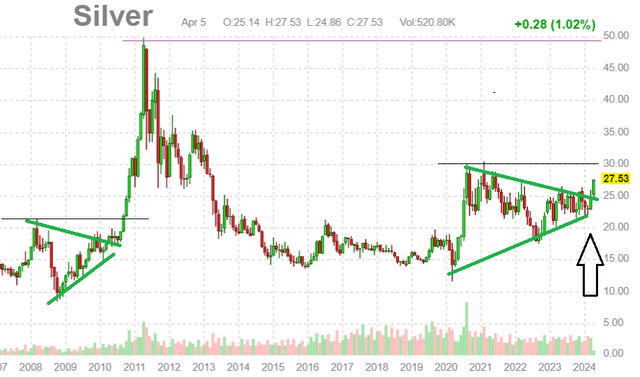

EXK is in a good spot considering its planned production growth precisely as the prices for silver and gold are breaking out higher. Gold above $2,300/oz is at its highest level on record and silver currently trading above $27.50 is at a three-year high.

From a technical perspective, we believe the $30/oz milestone is on the table for silver this year which could kickstart a bigger wave of momentum retesting levels going back to its run in 2011.

According to the "Silver Institute" industry group, the forecast is for a global supply deficit to extend for its fourth consecutive year through 2024 as a fundamental tailwind for higher prices.

We can point to recently stronger economic data including from out of China as adding to the demand side of the equation while silver continues to play an important role in high-tech and industrial applications as a demand driver.

There is also a component here related to macro uncertainty between the direction of inflation and the next steps in Fed policy. In many ways, the current action in silver reflects its traditional role as a store of wealth or as a flight to safety asset.

source: finviz

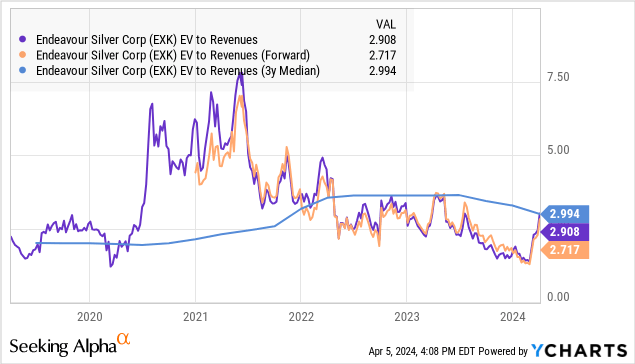

Naturally, Endeavour Silver is well-positioned to benefit with higher prices directly driving its revenue and earnings potential. Notably, shares trading at a 3x EV to sales multiple is at a discount compared to the 3-year average for the valuation multiple.

Data by YCharts

Data by YCharts This metric reached as high as 7.5x back in 2021 highlighting the upside potential assuming the rally in precious metals continues. We'd also say that the EV to EBITDA multiple closer to 13x on a forward basis is compelling considering the production ramp-up expected by next year.

From the stock price chart, EXK traded as high as $4.50 in Q2 2023 which we believe can work as an upside target reflecting a strong metals pricing environment.

Seeking Alpha

Final Thoughts

We rate EXK as a buy, with industry-leading exposure to silver. The company appears to be moving beyond some of its operational and financial challenges faced in 2023 with a positive outlook for strong production growth.

In terms of risks, beyond what would be a disappointing reversal in metals prices, it will be important for Endeavour Silver to deliver on its guidance. Monitoring points over the next few quarters include performance metrics like quarterly gold and silver output, cost levels, cash flows, and profitability margins. We also want to see favorable progress toward the completion of Terronera.