Part I of this series presented readers with a general survey of metals markets, with the promise that subsequent installments would provide a Top-3 ranking of metals markets for the upcoming year. Part II started that ranking (in reverse order) by presenting the #3 metal for 2017: gold.

Part III continues by presenting the #2 metal in this year’s ranking: silver. Obviously there are similar arguments to make on behalf of silver as were made previously for gold. Like gold, silver is also a monetary metal and thus a store of wealth. Where the silver market and the gold market differ greatly is seen with the gold/silver price ratio.

For over 4,000 years; this price ratio averaged roughly 15:1. Then, approximately 100 years ago, this ratio began to become extremely skewed. The price of silver plunged to a 600-year low (in real dollars). Concurrently, the gold/silver price ratio exploded, reaching extremes exceeding 100:1.

(click to enlarge)

In the Earth’s crust, gold and silver occur naturally at about a 17:1 ratio. Given that for 4,000+ years the price ratio averaged 15:1, this indicates that relative to the supply of each metal that humanity has always had a slight preference for silver. This should not surprise lovers of jewelry. Silver is a more-brilliant metal than gold, one of the reasons why it is a superior material from which to make mirrors. The solar mirrors used in the generation of solar energy are coated with silver to enhance their reflective properties.

In addition to the historical preference of humanity for silver; there has been an explosion in the number of uses for silver, while silver continues to remain popular as jewelry and/or money (outside of the Western world). Given the historical preference for silver and its increasing uses in industry and commerce, this collapse in price cannot be easily explained.

Silver is humanity’s most-versatile metal, with more hi- and low-tech applications than any other metal. In addition to silver’s importance in the solar power industry, it has also emerged as the key ingredient in a long list of next-generation anti-microbial products. Silver-based applications are far superior to antibiotics in killing micro-organisms in two respects: the technology is more effective, and (unlike antibiotics) microbial organisms cannot develop resistance to silver-based anti-microbial products.

Silver is another metal which is used in hi-tech batteries because of its very high energy-to-weight ratio, and thus it is in high demand for military applications which require superior performance. It is also used in the manufacturing of high-performance bearings (jet engines), as a chemical catalyst, and in brazing/soldering and electronics. Meanwhile silver continues to be widely used in jewelry and silverware.

Silver is still a precious metal, just ask the 1.25 billion residents of India. In 2013; after the government of India slapped a temporary embargo on imports of gold into India, the people of India responded to reduced access (and higher prices) for gold by immediately setting a new, all-time record for silver imports into that nation.

What do the Indian people do with the fruits of their labours? They don’t leave it sitting in the paper currency of India – rupees. They convert their savings to silver or gold and thus don’t have to fear rapidly losing that wealth to “inflation”, as noted in a famous quotation.

In the absence of the gold standard, there is no way to protect savings from confiscation through inflation.

Because silver was dramatically under-priced, it was over-consumed. The chart below shows the collapse in global silver inventories which occurred when the price was driven to its 600-year low.

(click to enlarge)

As reported by silver commentator, Steve St. Angelo, the Silver Institute is now acknowledging that the silver market has remained in continuous supply deficit for the last 13 years, as well. This extends the supply deficit in the silver market back to before 1990, when the collapse in silver inventories began.

However, the collapse in the total supply of silver dates back even farther. Noted silver researcher Ted Butler has concluded that over 90% of the world’s stockpiles of silver have been consumed, with the destruction of these stockpiles dating back as far as the 1950’s.

How can a metal be consumed? Simple. Because silver is extremely potent in both chemical and metallurgical terms, in many of its industrial applications it is used in only tiny quantities. Because the price of silver has been so low, it has been uneconomical to recycle the silver used in these products. Thus most of humanity’s stockpiles of silver, accumulated over 4,000 years, are gone – strewn across the world’s landfills in minute concentrations.

Similarly, decades of under-pricing have decimated the world’s silver mining industry. More than 90% of the world’s primary silver mines have been bankrupted. As a result, for the first time in history humanity must obtain the vast majority of silver as the byproduct of other metals production.

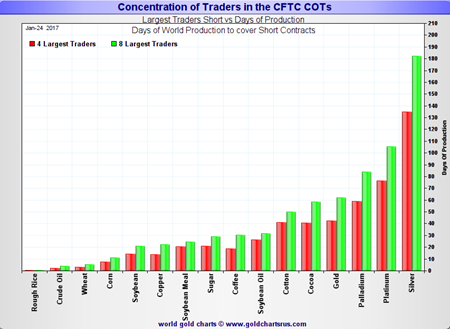

Despite the decimation of silver inventories and stockpiles, despite the collapse of the silver mining industry, and despite a permanent supply deficit in this market, Western bullion banks have maintained a gigantic, permanent short position in the silver market which continues to apply downward pressure on prices.

(click to enlarge)

Because the silver mining industry has largely vanished and most of our silver supply now comes from the byproducts of other mining, this makes the supply of silver (and the silver market itself) extremely inelastic. What this means is that even large increases in the price of silver will result in very little additional supply coming to the market.

The silver market is in (permanent) deficit. Inventories are exhausted. Stockpiles are gone. Default is imminent. When this happens, with a commodity which is of vital importance in numerous industries, the silver market will experience a massive price-spike as silver-users compete for minimal mine supply. The only reason why silver does not make it to the top of the 2017 metals ranking is that because of the lack of transparency in this market, it is impossible to specify how soon this price-spike will take place.

Meanwhile, silver mining remains a business, for the relative handful of mining companies which are still able to mine humanity’s most-versatile metal at a profit. Stockhouse had the opportunity to speak with the CEO’s of a couple of the planet’s most-rare corporations: primary silver miners. The CEO of Endeavour Silver, Bradford Cooke, drew attention to the unique parameters of the silver market.

“The backdrop for silver which is different than gold is falling mine supply. The reason for that is that silver is one of the very few commodities that is primarily a byproduct of other mining. It’s a byproduct of copper, a byproduct of lead, a byproduct of zinc, and those mines didn’t get built in the last five years. So we’re going to see quite a considerable reduction in byproduct silver over the next three years, maybe a 50 – 75 million ounce reduction in mine supply.”

Despite these extremely bullish supply/demand parameters, the seasoned management teams of these silver mining companies know better than to plan for immediately rising prices. Cooke spelled out that prudent strategy.

“We’re using $17/oz (USD) silver and $1190/oz (USD) gold for our outlook this year. We’ve modeled $16 - $19/oz silver, but with at least one ‘accident’ to $24 and back. We call this year the ‘wildcard’, namely Mr. Trump or Brexit, or who knows what the next surprise will be. If you talk about a 3 – 5 year [price] outlook, it’s actually gotten considerably more bullish.”

Even with the unique market issues which are present in the silver mining industry, Endeavour has managed to steadily move forward in its operations. In its early years; the Company set a goal for itself of becoming a “top-5 primary producer of silver” in the world. CEO Cooke was asked to comment on that long-term goal.

“We’ve got one of the most exciting new greenfields discoveries in the last 10 years with our Terronera Project. That will become one of our next new mines. We’re building three new mines in the next three years to expand production by 50%. This business plan will accomplish that goal [becoming a top-5 producer].”

With Mexico being the world’s leading silver-producer, it’s not surprising that Great Panther Silver also has its operations based in Mexico. Robert Archer, CEO for Great Panther, also wanted to draw attention to the U.S. election of Donald Trump, but Archer was more focused on the indirect effect which Trump has already had on Great Panther’s operations.

“I don’t see the election as having a great impact on the silver market, per se. Where it has had an obvious impact already is in the exchange rate – the dollar/Mexican peso exchange rate –going in favor of the dollar and to the peso’s detriment. But that has been very, very good for us. Most of our costs are in pesos and revenues are in dollars, so from a cost perspective it has been terrific for our operations.”

As a silver mining executive, Archer is naturally bullish on silver over the longer term. However, like Bradford Cooke at Endeavour, Great Panther is also careful not to allow that outlook to cloud its thinking as it plans its present operations.

“We’re working with prices that are very close to current levels [in internal budgeting]. We may think and hope that prices will go higher, but it’s always better to budget at a more conservative level, and if it does go higher then that’s just gravy.”

Like Endeavour, Great Panther has also managed to grow its operations and increase production, even through the last five, difficult years in the mining sector. Unlike Endeavour, Great Panther is now looking to expand operations into one of the world’s other leading silver-producers: Peru.

“The move into Peru is really to try and replicate what we’ve done in Mexico. We’ve looked at a lot of different projects, but the Coricancha Mine is one that we had an option agreement on. We did a fair bit of work on it and it gave us a chance to really become comfortable with the asset. It’s going to take about 18 months to get the mine back to a production level. We hope to have an updated resource estimate out in the second quarter, and hope to have a PEA completed by Q4. We have a strong balance sheet with over $54 million (US) in cash, so we’re fully funded to take the project into production.”

Investors looking to capitalize on the re-pricing of silver have two choices. They can invest in the rare collection of primary silver miners which still remain. Alternately, because silver is a precious metal, they can buy and hold the metal directly.

Buy low; sell high. This is the maxim of how investors make money. These words of wisdom are especially appropriate when it comes to investing in silver.

FULL DISCLOSURE: I hold shares in Great Panther Silver as well as physical silver.