(Image via Northern Graphite Corporation.)

(Image via Northern Graphite Corporation.)

Countries around the world are moving to target 100% sales of zero-emission vehicles in the coming years. How this will be accomplished may be uncertain, but one thing is for sure, government bodies will need a lot of help to make sure the world has enough graphite to meet projected demand from the lithium-ion battery / electric vehicle (EV), fuel cell and vanadium redox battery industries. All are large users of graphite.

Countries around the world are moving to target 100% sales of zero-emission vehicles in the coming years. How this will be accomplished may be uncertain, but one thing is for sure, government bodies will need a lot of help to make sure the world has enough graphite to meet projected demand from the lithium-ion battery / electric vehicle (EV), fuel cell and vanadium redox battery industries. All are large users of graphite.

Thanks to EVs alone, the graphite market could be worth $21.6 Billion by 2027.

Graphite is the anode material in a lithium-ion battery and there are no substitutes.

Volkswagen (ETR: VOW3) will require 300 giga watt hours (gWh) of battery production to meet its sales targets by 2025. That German auto manufacturer is not alone,

Tesla Inc. (NASDAQ: TSLA) will need 350 gWh, and

Daimler / Mercedes (ETR: DAI) wants 200 gWh, all well before the end of the decade. This only represents a fraction of the demand as other car manufacturers have big plans and China, which is the world’s biggest EV market, is targeting 25% of new car sales to be EV’s in four years’ time. This alone will require almost a 50% increase in world graphite production.

Li-ion battery sales are already a $30 billion industry growing at 20% a year. To feed this hunger, many industry analysts forecast that many new graphite mines will be essential and will require billions in investment to ensure that the EV market can meet its demand. Graphite needs the largest production increase of all the battery minerals and no substitutions will suffice.

(Share of Mineral Demand from Energy Storage source: The International Energy Agency. Click to enlarge)

(Share of Mineral Demand from Energy Storage source: The International Energy Agency. Click to enlarge)

Canada based Company

Northern Graphite Corporation (TSX-V: NGC, OTCQB: NGPHF, Forum) is pursuing the development of its 100%-owned Bissett Creek graphite project, an advanced stage project with a full Feasibility Study and a Preliminary Economic Assessment for a subsequent expansion. Permitting is well advanced and the Company is in a position to make a construction decision subject to financing.

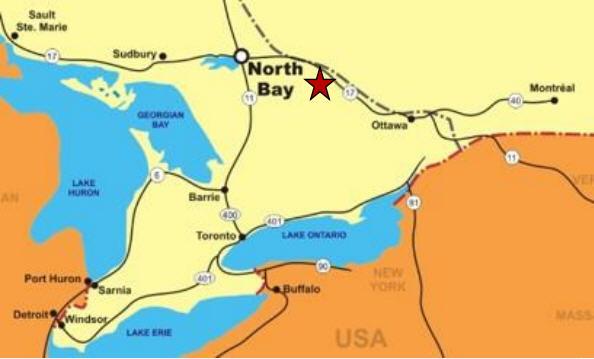

The project is located just 15 km off the Trans-Canada highway between the cities of Ottawa and North Bay, Ontario. Being situated in the southern part of Canada it has ready access to labour, supplies, a natural gas line, equipment and concentrate transportation with direct trucking to US markets and the port of Montréal only five hours away. As they say, location, location, location, and all this represents a significant competitive advantage for the Company since most its peers are operating in remote locations in northern Canada, Africa, or China.

What sets Bissett Creek production apart from most other graphite deposits is its very high percentage of L/XL/XXL size flake. This will enable the Company to initially focus on higher priced and value-added industrial markets and expand into battery markets when prices improve. And almost all is “battery grade”. The project also has a reasonable capital cost and a realistic production rate relative to the size of the current market. Production can be significantly expanded as EV demand, specifically Li-ion demand, grows based on the Project’s substantial measured and indicated resources.

Within three years, it is forecast that electric cars will achieve price parity with gasoline vehicles, according to

Bloomberg New Energy Finance. By 2025, EVs will become even cheaper as costs decline.

The price of a Li-ion battery pack has fallen 89% from more than $1,100 (USD) / kWh in 2010 to $137 / kWh in 2020, according to the latest forecast from Bloomberg NEF researchers. In about two years, the average price will hover near $100 / kWh (some are already less). It is clear that prices related to EVs are going down all the time, while the market has also exploded in the last 10 years.

A deeper look into Bisset Creek:

(Map via Northern Graphite Corporation.)

(Map via Northern Graphite Corporation.)

A recent independent study estimated that Bissett Creek will have the highest margin of any current or proposed graphite project. Permitting is well advanced and the Company is in a position to make a construction decision subject to financing.

Approval of the Company’s Mine Closure Plan (MCP) resulted in

a mining lease being granted by the Ministry of Northern Development and Mines for the Bissett Creek project. The MCP is an all-encompassing document that describes the nature of the operations that will be carried out, detailed current baseline environmental conditions, potential effects on the environment together with appropriate mitigation measures, and the Company's plan for rehabilitating the site to its natural state at the end of operations. The project also has no opposition from local communities or First Nations.

Bisset Creek will be an open pit mine with little overburden. It boasts a 0.79 waste-to-ore ratio and a simple flotation flowsheet with coarse grind and few polishing and cleaning steps. A bulk sample pilot plan test has been completed and low variability was detected throughout the deposit.

The feasibility study covers Phase 1 of the project with an initial plan of producing 25,000 tonnes of graphite concentrate per year. A preliminary economic assessment has been completed on a subsequent Phase 2 expansion to approximately 45,000tpy based on measured and indicated resources only. The deposit has additional M&I resources and inferred resources and it has not yet been closed off by drilling indicating its ultimate potential is 80-100,000tpy.

(Image via Northern Graphite Corporation. Click to enlarge.)

The importance of L / XL / XXL flake:

(Image via Northern Graphite Corporation. Click to enlarge.)

The importance of L / XL / XXL flake:

Many who track graphite (and graphene) do so because of the EV market, but there are a host of industrial applications for graphite from lubricants to pencils. The flake graphite that is unearthed by the Northern Graphite team can be pressed into sheets destined to be used as purified and micronized products for thermal management in consumer electronics, fire retardants, insulation products, conductive paint and wall coverings, fuel cells and flow batteries. Other applications include powder metallurgy, ceramics, military and nuclear applications, specialty engineered products and drilling fluids. Few other operations in this space can check so many applicable boxes which is due to the XL/XXL flake size and purity of Northern’s concentrates. Significantly, both fuel cells and vanadium redox batteries require large amounts of graphite, mainly the large flake sizes and these technologies are expected to be a big part of the green revolution.

The market needs more XL / XXL flake as production in China, specifically for flakes of this size, is declining and that industry juggernaut has been turning to imports.

World flake graphite production is approximately 850,000 tonnes. China produces and consumes 70 to 80% and produces nearly all battery anode material (BAM). Because of this dependence on China, the United States and European Union have declared graphite a

critical mineral.

China produces BAM from small flake graphite because it is plentiful and cheap. It has large resources of small flake and excess production capacity but is forecasting a large supply deficit due to EV growth. In the past few years, the flake graphite price index of Benchmark Mineral Intelligence has declined by more than a quarter due to excess production capacity in China and new supply from Africa. Prices for large flake graphite (+80 mesh) are currently in the order of $1,000 / tonne (USD) compared to the 2012 peak of over $2,500 / tonne (USD).

Growing demand will overtake supply in the near future and new western sources are needed, but in the interim it remains a very competitive market. Circling back to Northern Graphite’s resource, its large / XL flake deposit will mean that it can initially focus on high value, high margin markets (specifically in the US and Europe), which have higher prices/margins and less competition. As the chart below indicates, battery demand is not yet affecting graphite prices (or share prices for the most part). But multiple new mines are required for the promise of EVs to be realized and higher prices are the only way that can happen.

(Graphite price chart via Benchmark Mineral Intelligence. Click to enlarge.)

Northern Graphite Corporation management and board:

(Graphite price chart via Benchmark Mineral Intelligence. Click to enlarge.)

Northern Graphite Corporation management and board:

Northern Graphite is led by an experienced, well respected management team. Their concern for preserving shareholder value is evidenced by the Company’s very low level of overhead expenses and the fact that it only has 65 million shares outstanding after completing a feasibility study and receiving its major mining permit. That is very rare for an advanced stage project. Most of its graphite peers already have hundreds of millions of shares outstanding with mine financing still to come.

(Management slide via the Company.)

Investment conclusion:

(Management slide via the Company.)

Investment conclusion:

Benchmark Mineral Intelligence estimates that major automobile makers have committed more than $300 billion (USD) to the development of EVs and that there are over 100 Li-ion battery mega-factories in the pipeline. To meet this demand, multiples of current annual world graphite production are needed

Northern Graphite represents an opportunity for investors to get into the graphite market and enhance their portfolio before graphite prices take off. The Bissett Creek Project already has robust economics at current prices due to its very good flake size distribution and location. This will enable the Company to start with a smaller project that has a reasonable capital cost and a realistic production level relative to the size of the market. The very high percentage of L/XL/XXL flake will also enable the Company to initially focus on higher priced and value-added industrial markets and expand into battery markets when small flake prices improve. Unlike many graphite deposits around the globe, essentially all Bissett Creek production is “battery grade”.

This “safe” approach minimizes market and financial risk and enhances shareholder value in the process. As the market grows Northern Graphite can then expand production in unison.

To find out more about this Company, its operations and full investment proposition, visit their website

northerngraphite.com.

FULL DISCLOSURE: This is a paid article produced by Stockhouse Publishing.