After a record day for the Dow Jones Industrial Average ($DJI) yesterday, we’ll see what stocks can do for an encore. Futures

markets point toward strength following overnight gains in Europe.

A little more optimism opened up Wednesday surrounding Italy’s budget talks, with Italian media reporting that the government

might seek lower deficit targets in 2020 and 2021. That seemed to calm things a bit and put some vigor into the euro after it sank

earlier this week. That, along with what many investors read as market-friendly comments from Fed Chair Jerome Powell on Tuesday,

could help explain the sunny feelings on Wall Street this morning. A handful of Fed speakers are on tap today, so the central bank

might continue to influence stocks.

Market action early this week presents a pretty stark contrast to the overriding pattern seen much of the year. Instead of small

caps and the Nasdaq (COMP) leading while the Dow Jones Industrial Average ($DJI) lagged behind, the opposite occurred. Tuesday saw

more of that, with the $DJI recording a new record high close while both COMP and the Russell 2000 (RUT) small-cap index lost

ground. In fact, the $DJI now leads the RUT in year-to-date gains.

From the headlines, you might think Tuesday was a great day. The emphasis seemed to be mainly on the $DJI rising 100 points.

Multinational companies continued to rally in the after-effects of Monday’s new North American trade deal. Looking at the broader

market beyond those 30 high-profile DJIA stocks, however, the plot thickens.

Warning Sign From Small Caps?

Small caps continue to sag as some investors apparently unwind long positions they took earlier this year in hopes of possible

protection from trade headwinds. Earlier this week, RUT fell below its 50-day moving average (see Fig. 1 below). That could get a

bearish read from technical traders.

It also could look bearish if you take the historic view that small caps tend to lead rallies. While that isn’t always the case,

it did seem that way earlier this year as the overall market went up and the RUT posted one high after another. The recent RUT

struggles, however, might be seen as a warning sign. There’s no need to sound any alarm bells, but if RUT continues to lag

it’s possible the rest of the market might miss its leadership. On the positive side, small-caps have historically done well in

rate-hike environments, and the futures market puts high odds on another hike before the end of the year.

One thing to consider is that small caps might be more vulnerable than large caps if the economy starts to slow, simply because

many small-cap companies do a lot of business serving one or two large-cap clients. If bigger companies see weakening demand, that

could potentially have an exponential impact on small-caps that depend on business from larger firms.

Tuesday also continued a recent pattern of both the $DJI and the S&P 500 Index (SPX) giving back some of their early gains

to finish off of session highs. It happened Monday, too, and the SPX couldn’t hold onto Tuesday’s slight midday gains. This remains

a pattern to watch, because it could indicate potential tired trade where investors aren’t eager to chase the market higher when

stocks are already at or near all-time peaks.

Companies Raise Red Flags

What might be driving some of this action—besides the fact that the SPX is trading at a high level of around 18 times projected

forward earnings—is a handful of companies putting up warning flags. We saw that last week when Nike Inc. (NYSE:

NKE) executives, in the company’s quarterly earnings call,

cited “global trade uncertainty” and “dollar strengthening” as potential risks. Then on Tuesday, PepsiCo, Inc.

(NASDAQ: PEP) also warned of currency headwinds and referred

to higher transportation and aluminium costs.

Those two companies, both of which derive a good chunk of business from overseas, could be canaries in the coal mine as the rest

of earnings season looms. If this is the vanguard of an earnings season where company executives keep expressing concerns about

trade wars, higher costs, and the strong dollar, that could play into investors’ expectations for Q4 and full-year results. It also

could raise questions about the potential strength of 2019 earnings, with the market arguably priced for solid year-over-year

profit gains once again.

The Powell Factor

Fed Chairman Jerome Powell spoke yesterday and he painted a promising picture of an economy that’s charging along with solid

growth and low inflation. Though he reiterated that the Fed would “act with authority” to address inflation if it starts rising, he

also suggested that the Phillips Curve—a concept that says lower unemployment can cause higher wages as employers compete for

labor, potentially leading to inflation—might be less of an issue now. “Many factors, including better conduct of monetary policy

over the past few decades, have greatly reduced, but not eliminated, the effects that tight labor markets have on inflation,”

Powell said.

However, Powell doesn’t see a lot of “slack” in the job market, and notes that many business owners are having trouble finding

qualified employees. That leaves the possibility of more price increases, Powell said, but he also noted that a similar situation

in the late 1990’s didn’t bring higher prices. As long as inflation expectations remain “anchored,” a modest steepening of the

Phillips curve wouldn’t be likely to cause a significant rise in inflation or “demand a disruptive policy tightening,” Powell

noted.

Judging from his speech, Powell (though not necessarily the Fed as a whole) seems less worried by growth in wages and not too

eager to press the brakes if a little inflation does start to surface. In other words, he appears to be taking a dovish view. That

might be something to consider Friday when investors eye wage data in the September payrolls report. Earlier this year,

higher-than-expected wage increases spooked the market as inflation fears ignited. Maybe higher wages now won’t have the same

impact. We’ll have to wait and see.

As of Tuesday, consensus among analysts for September jobs growth stood at 184,000, according to Briefing.com. That’s down

slightly from 201,000 in August. Average hourly earnings are expected to rise 0.3 percent, down from August’s 0.4

percent.

Commodities (Except Oil) Get a Boost

That old saying, “what goes up must come down” hasn’t seemed to apply lately to the crude oil market, up significantly from

summer lows near $64 a barrel for U.S. oil to above $75 earlier this week amid supply concerns. However, a brief pause hit the

market Tuesday, maybe a sign of some profit taking. There’s a lot of concern among oil analysts about whether increased output from

Russia and Saudi Arabia can make up for potential losses from Iran due to sanctions. In addition, some wonder if Saudi Arabia is

even technically capable of raising production much more from already very high levels. Today’s U.S. stockpiles data might be worth

a look to see if U.S. demand has started to decline, as “driving season” is long over.

Other commodity prices climbed Tuesday, with gold, copper, and natural gas among the gainers. Somewhat surprisingly, this all

happened even as the dollar index advanced. Often, a stronger dollar hurts commodity values, but in this case the dollar seemed to

be partly reflecting weakness in the euro, which has struggled this week amid Italian budget concerns.

FAANG stocks had a rough go lately, especially Facebook, Inc. (NASDAQ: FB). Shares of FB are down nearly 6 percent since it announced last week it had

found a “security issue.” Away from the Internet economy, auto sales data out Tuesday looked pretty disappointing. General

Motors Company (NYSE: GM) reported an 11.1 percent

drop in Q3 domestic new vehicle deliveries while Ford (F) saw year-over-year U.S. sales decline 11.1 percent in September.

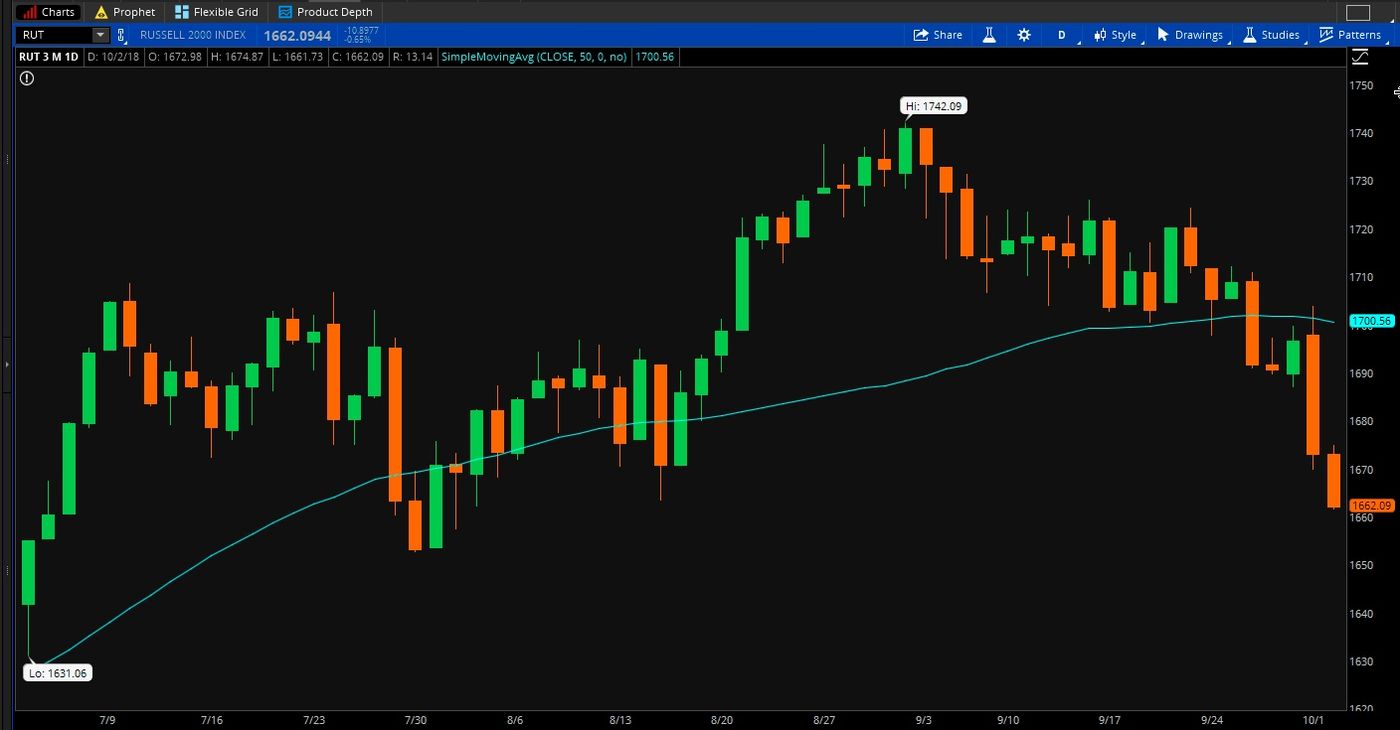

Figure 1: Trade Gap: The Russell

2000 (RUT) index of small-cap stocks dropped below its 50-day moving average (blue line) this week as investors appeared to be

removing some bullish bets built up on hopes that small stocks might be less prone to bearish trade winds. The RUT is down sharply

from its all-time high set Aug. 31. Data Source: FTSE Russell. Chart source: The thinkorswim® platform from TD

Ameritrade. For illustrative purposes only. Past performance does not guarantee future results.

Figure 1: Trade Gap: The Russell

2000 (RUT) index of small-cap stocks dropped below its 50-day moving average (blue line) this week as investors appeared to be

removing some bullish bets built up on hopes that small stocks might be less prone to bearish trade winds. The RUT is down sharply

from its all-time high set Aug. 31. Data Source: FTSE Russell. Chart source: The thinkorswim® platform from TD

Ameritrade. For illustrative purposes only. Past performance does not guarantee future results.

Three’s a Crowd

Those “3” signs are likely beginning to crop up at a gas station near you. That is, gas for $3 or more a gallon. It’s even hit

$4 at some West Coast stations. Average gas prices last week around the country reached $2.84 a gallon, up 26 cents from a year

ago, according to the Energy Information Administration (EIA). This comes as consumer confidence recently hit an 18-year high.

However, over the course of history, one thing that’s often corroded consumer confidence is high gas prices. And these rising costs

are hitting right ahead of holiday shopping season, potentially a barrier for consumer discretionary companies like

Amazon.com, Inc. (NASDAQ: AMZN) and

Target Corporation (NYSE: TGT), both of which

suffered sharp losses Tuesday (though some analysts said AMZN’s losses might have something to do with the company raising its

minimum wage to $15 an hour), though it’s hard to draw a direct line between pressure on retailers yesterday and that specific news

item.

It could be interesting to watch that sector in coming weeks to see if there’s any impact from people holding back on

discretionary purchases so they can fill their tanks. While wages are up nearly 3 percent over the last year and gasoline

represents only a small portion of the average person’s budget, the psychological factor of seeing a new digit can sometimes make

people want to get more frugal.

Bank Sector Sputtering Into Earnings

Financial earnings season starts late next week with the sector slumping. Since hitting a six-month high on Sept. 20, the

S&P financial sector has dropped 4.3 percent. The easy explanation would seem to be 10-year Treasury note yields, which at

least through Tuesday haven’t shown much sign of moving to push through the May highs. Thirty-year yields have also leveled off.

The Fed’s meeting last week received a mostly dovish reading from analysts, with long-term Fed rate expectations not moving much

from where they’d been. While there have been a lot of positives for the financial sector this year, some analysts are starting to

question how long the economy can grow at this pace, and how long corporations and consumers can maintain demand for loans. The

August construction spending report released Monday showed private construction spending down for the third-straight month, with

residential construction falling 0.7 percent. Data like that certainly wouldn’t seem positive for companies that make money in part

by lending money.

Diversity Corner

If you’re a long-term investor considering diversification, that doesn’t just mean comparing S&P 500 sectors. It could also

mean looking beyond the borders. U.S. stocks are way ahead of their overseas counterparts the last few years, but that hasn’t

always been the case. Investors who’ve overlooked international stocks to focus on U.S. names might want to consider that the

historic push and pull between foreign and domestic isn’t necessarily over. Even very recently, between 2008 and 2013, there was a

six-year stretch in which international stocks did better each year than U.S. stocks.

U.S. stocks now trade on average at higher valuations than international shares, and the U.S. market is heavily weighted toward

technology, a sector that’s been gaining by leaps and bounds. Foreign stocks, on the other hand, are weighted toward cheaply valued

industrial and financial stocks, The Wall Street Journal noted in a recent article. While emerging stocks have been getting

pummeled this year, there’s no way to know how long the current trend might continue, and that’s yet another reason why a

diversified portfolio could be worth considering.

Information from TDA is not intended to be investment advice or construed as a recommendation or endorsement of any

particular investment or investment strategy, and is for illustrative purposes only. Be sure to understand all risks involved with

each strategy, including commission costs, before attempting to place any trade.

© 2018 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.