What happens when the world’s biggest miners run out of gold?

We already know.

We’ve already hit peak gold, and the only companies sitting on promising new reserves are the junior miners.

The big miners are scrambling for more gold, and merger mania has taken hold.

Large-cap miners are doing three things at record pace:

- They’re merging with other major miners (think Newmont/Goldcorp and Barrick/Randgold)

- They’re scooping up juniors sitting on the best patches of gold.

- They’re conducting a series of micro deals to gradually insert themselves in the junior-mining patch.

We know those juniors who have already been targeted for acquisition and micro deals, so we’re looking for the next prospective beneficiary.

Based on a series of recent events that includes the announcement of a formidable new CEO and a near-term production target of 50,000+ ounces of gold per year in one of the world’s hottest precious metal venues, African Gold Group (TSX.V: AGG; OTC:AGGFF) could be on a few radars. And that’s just the starting point: the company is evaluating the potential for an increase in estimated annual production to 100,000 ounces per year.

Not only is AGG sitting on a potential 2.2-million-ounce mineral resource at its Kobada Gold Project in Mali’s prolific gold-producing Birimian Greenstone Belt … but it’s also just appointed a new CEO that will turn investor heads: Legendary mining financier Stan Bharti.

Bharti has been in Mali for over a decade already. He’s proved he can turn a company around for a 20X profit.

He’s already done it once in this same venue. In 2008, Bharti’s Forbes & Manhattan acquired Avion in Mali for $20 million, turned it around and sold it to Endeavour for $500 million in 2012.

Now that Mali mine is Endeavour’s main asset.

He’s hoping to do it again with African Gold Group.

His timing is exquisite, too: Gold is experiencing the perfect setup.

Major miners are gunning for junior prospects. The world’s central banks are hoarding gold at a record pace. Talk about the Gold Standard is no longer just fluff. And major world powers are making every effort to disengage from the US dollar.

All of this has seen the world’s most precious metal make prodigious runs to multi-year highs.

But Bharti doesn’t even need this perfect setup to make good on gold: The last time he did it in Mali was in the middle of a global financial crisis.

Here are 5 reasons to keep a close eye on AGG (TSX.V: AGG; OTC:AGGFF) right now:

#1 No Fracking Way

Even supported by higher gold prices, senior miners don’t have more gold to get out the ground.

That means this is a junior game for the first time in recent history, and the African Gold Group (TSX.V: AGG; OTC:AGGFF) news flow is putting the company in a very strong position.

Junior gold-mining ETFs are blowing things out of the water. The VanEck Vectors Junior Gold Miners ETF is up over 36% year to date.

Last year, Goldcorp Inc. Chairman Ian Tefler called peak gold, saying production had finally peaked after four decades of uninterrupted growth. Going forward, it’s extended decline for the big miners.

And while fracking led to an unexpected surge in oil and gas supplies for the fossil fuels industry, there's practically zero prospect of any unconventional methods or technologies to boost our gold reserves becoming economically viable in our lifetimes.

To add new gold to their portfolios, the big gold miners are entering into a phase of merger mania.

The first mega-merger was Barrick Gold’s $18.3-billion acquisition of Randgold last year.

That was followed this April by Newmont Mining’s $10-billion acquisition of Goldcorp, right after Tefler called “Peak Gold”.

The micro deals are also lining up, quickly.

There’s even more to this picture than peak gold and merger mania.

The once fantastical idea of returning to the Gold Standard is now being voiced publicly by Trump, who thinks there’s “something very nice about the gold standard”, and by economist Judy Sheldon.

Switching back to a gold standard would mean the US central bank would have to purchase massive amounts of the metal to backstop every dollar.

And central banks the world over are embarking on massive gold-buying sprees already as equity markets cool and as Russia, China and others are stockpiling the precious metal in a de-dollarization frenzy.

Gold stocks are outperforming the equities market, and it’s never been a better time to buy gold.

Stan Bharti knows this well: That’s why he’s behind African Gold Group (TSX.V: AGG; OTC:AGGFF).

He also knows that not all junior gold stocks will come out of this a winner.

He’s targeting AGG for low-cost production and undervalued assets that are likely to yield higher returns.

And he knows Africa better than most …

#2 Low-Cost Production, World-Class Venue

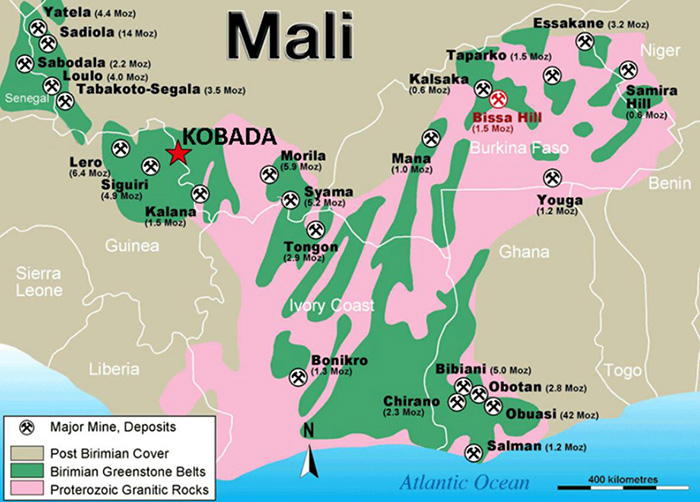

Mali is the third-largest producer of gold in all of Africa, and the Birimian Greenstone Belt—the home of Africa Gold Group’s Kobada Project—is the motherlode of African gold with a long history of mining that dates back to the 19th Century.

It’s a massive belt the spans 350,000 square kilometers of world-class gold deposits stretching across Burkina Faso, Ghana, Guinea, Mali, Niger, Senegal and Côte d’Ivoire.

African Gold Group (TSX.V: AGG; OTC:AGGFF) is right in the middle of this belt:

The brilliant part here is that the mine holds a total resource of a whopping 2.2 million ounces.

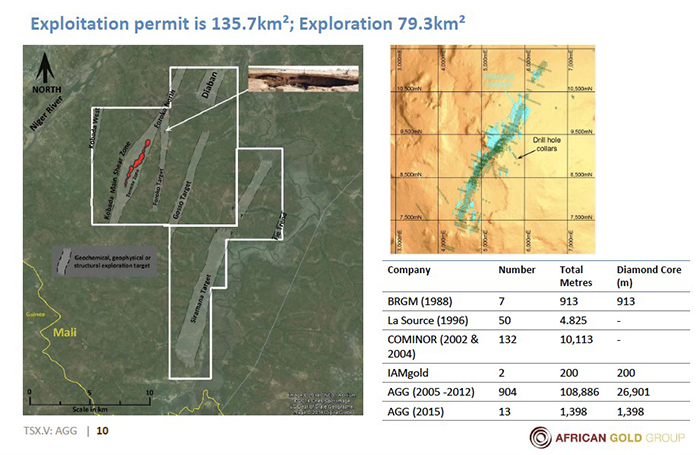

Even more brilliant: The Kobada project is a huge part of this. It’s 4 kilometers long and 12 kilometers wide and African Gold Group owns the entire license.

From a geological perspective, AGG could end up tripling its resource here.

It’s got three zones right nearby the already proven-up 2.2 million ounces in mineral resources—and it’s all easy to drill because it’s all right near the surface.

The deepest hole AGG’s had to drill so far has been only 300 meters.

A 2016 feasibility study has already demonstrated that Kobada is simple to mine on a technical level, and that’s music to investor ears.

This is an open pit operation with gravity separation and leach. That means it will be a low-cost, scalable, free dig.

AGG puts average LOM cash operating costs at $557/Oz Au, exclusive of royalties, and all-in LOM sustaining cash operating costs at $788/Oz Au.

#3 Payback Time

The economics are just what large-cap miners, and investors, are looking for: high early cash flows from starter pits and a post-tax IRR of 43%, based on $1200 gold, or 55% based on $1400 gold.

With a planned $45.4-million pre-production capital cost, African Gold Group is targeting a 1.5-year payback from the start of commercial production, and full payback in only 2.5 years.

The 2016 feasibility study shows that AGG can produce 50,000 ounces of gold a year and build that to 100,000 ounces a year …

All for under $50 million.

There are a lot of great projects out there, but many of them don’t see the light of day because they need billions in funding to get them off the ground.

That’s not the case with Kobada.

#4 The Legend Behind the Gold

When it comes to gold miner profiles, it’s hard to beat Stan Bharti, who just took the lead for African Gold Group (TSX.V: AGG; OTC:AGGFF).

On August 7th, AGG announced the Bharti had been appointed chairman of the board of directors and president & CEO.

Not only is he an engineer, international financier and seasoned entrepreneur who has brought in $3 billion in investment capital for the companies he’s worked with, but he’s also been behind dozens of turn-around success stories—including in Mali.

And the Kobada Project is the perfect setup for Bharti’s Toronto-based Forbes & Manhattan (F&M). F&M is, after all, a leading rescuer of distressed assets.

The litmus test for the ideal distressed gold asset is lots of gold in the ground, plus a substandard management team.

For Bharti and F&M, Kobada represented the next big turnaround.

Why?

- It already had a feasibility study with a resource of 2 million ounces that was going to be easy to mine.

- It was in one of the most prolific gold belts in Africa

- The previous management wasn’t able to deliver

F&M took it over and brought on a new board, including Stan Bharti as Chairman, President & CEO. Now it’s time to get to that gold.

Bharti’s track record on turnarounds speaks for itself, but there are other AGG board members and managers to be excited about here, as well:

The Honorable Peter Pettigrew is a former Canadian Foreign Minister who’s had access to the President of Mali.

Sir Sam Jonah is the former CEO of Anglo Gold Ashanti, one of the two major gold companies operating in Africa in the 1990s, and one of the most highly respected African gold veterans on the planet—and elsewhere, too: He’s been knighted by the Queen of England.

There’s also Bruce Humphrey, former COO of giant Goldcorp, the second-largest gold company in the world.

John Begeman, the CEO of Avion—the Mali-based gold company that he and Bharti built up from $20 million to $500 million.

These aren’t just board members—they’re operational legacies.

AGG also has a full local management team on the site with a very connected and powerful country manager when it comes to obtaining permits.

And now, AGG can boast another big name: Daniel Callow, a 12-year veteran for trading/mining giant Glencore’s African copper operations, whose just been made African Gold Group’s COO.

#5 Rapid-Fire News Flow

This is a company that owns a low-cost prolific gold asset with the potential to bring many times over returns, thanks to “Bharti effect”.

To recap:

We’re looking at a production starting point of 50,000 ounces per year. But that’s just the beginning. AGG is evaluating the potential for an increase in estimated annual production to 100,000 ounces per year.

Until now, the news flow was dominated by a brand new board of directors with its finger on the trigger of distressed assets sitting on massive mineral resources.

Now, the news flow may change to the gold itself because they’re targeting a completion date of December 2019 for an evaluation for 100,000 ounces per year.

This is potentially one of the best discount gold stories of recent times. AGG’s proved up resources of 2.2 million ounces alone are worth billions in revenue at today’s soaring gold prices. They’re worth billions even at yesterday’s prices.

And that 2.2 million ounces of mineral reserves is only what’s been proved up so far. This is a 4 kilometer-long and 12-kilometer wide stretch of prime gold that could contain triple the resources.

But what makes the company potentially worth even more is the fact that the big miners are on the hunt for just this type of junior they hope can replenish their declining reserves in the only way possible.

Five other companies to watch as peak gold looms:

Eldorado Gold Corp. (NYSE:EGO) (ELD.TO)

This Canadian mid-cap miner has assets in Europe and Brazil and has managed to cut cost per ounce significantly in recent years. Though its share price isn’t as high as it once was, Eldorado is well positioned to make significant advancements in the near-term.

In 2018, Eldorado produced over 349,000 ounces of gold, well above its previous expectations, and is set to boost production even further in 2019. Additionally, Eldorado is planning increased cash flow and revenue growth this year.

Eldorado’s President and CEO, George Burns, stated: “As a result of the team’s hard work in 2018, we are well positioned to grow annual gold production to over 500,000 ounces in 2020. We expect this will allow us to generate significant free cash flow and provide us with the opportunity to consider debt retirement later this year. “

Yamana Gold (NYSE:AUY) (YRI.TO)

Yamana, has recently completed its Cerro Moro project in Argentina, giving its investors something major to look out for. The company plans to ramp up its gold production by 20% through 2019 and its silver production by a whopping 200%. Investors can expect a serious increase in free cash flow if precious metal prices remain stable.

Recently, Yamana signed an agreement with Glencore and Goldcorp to develop and operate another Argentinian project, the Agua Rica. Initial analysis suggests the potential for a mine life in excess of 25 years at average annual production of approximately 236,000 tonnes (520 million pounds) of copper-equivalent metal, including the contributions of gold, molybdenum, and silver, for the first 10 years of operation.

The agreement is a major step forward for the Agua Rica region, and all of the miners working on it.

Agnico Eagle Mines Ltd (NYSE:AEM) (TSX:AEM)

Canadian based gold producer, Agnico Eagle Mines is an especially noteworthy company for investors. Why? Between 1991-2010, the company paid out dividends every year. With operations in Quebec, Mexico, and Finland, the company also is taking place in exploration activities in Europe, Latin America, and the United States.

Agnico is a company with a lot of exposure to gold, letting investors take advantage of long-term price movements.

Though the company joins a long list of gold majors that reported losses in 2018, but its cash flow deficit is largely attributed to its growth in production and new projects coming online.

Wheaton Precious Metals Corp. (NYSE:WPM) (TSX:WPM)

Wheaton is a company with its hands in operations all around the world. As one of the largest ‘streaming’ companies on the planet, Wheaton has agreements with 19 operating mines and 9 projects still in development. Its unique business model allows it to leverage price increases in the precious metals sector, as well as provide a quality dividend yield for its investors.

Recently, Wheaton sealed a deal with Hudbay Minerals Inc. relating to its Rosemont project. For an initial payment of $230 million, Wheaton is entited to 100 percent of payable gold and silver at a price of $450 per ounce and $3.90 per ounce respectively.

Randy Smallwood, Wheaton's President and Chief Executive Officer explained, "With their most recent successful construction of the Constancia mine in Peru, the Hudbay team has proven themselves to be strong and responsible mine developers, and we are excited about the same team moving this project into production. Rosemont is an ideal fit for Wheaton's portfolio of high-quality assets, and when it is in production, should add well over fifty thousand gold equivalent ounces to our already growing production profile."

Kinross Gold Corporation (NYSE:KGC) (TSX:K)

Kinross Gold Corporation is relatively new on the scene, founded in the early 90s, but it certainly isn’t lacking drive or experience. In 2015, the company received the highest ranking for of any Canadian miner in Maclean's magazine's annual assessment of socially responsible companies.

While Kinross posted a significant loss in the fourth quarter of 2018, the company is making strong moves to turn around its earnings, including the hiring of a new CFO, Andrea S. Freeborough.

“Andrea’s successful track record at Kinross and throughout her career, including accounting, international finance, M&A, and deep management experience, will be an excellent addition to our leadership team,” said Mr. Rollinson. “We have great talent at Kinross and succession planning is a key aspect of retaining that talent for the future success of our Company.”

By. Ian Jenkins

IMPORTANT NOTICE AND DISCLAIMER

PAID ADVERTISEMENT. This communication is a paid advertisement. Oilprice.com, Advanced Media Solutions Ltd, and their owners, managers, employees, and assigns (collectively “the Publisher”) is often paid by one or more of the profiled companies or a third party to disseminate these types of communications. In this case, the Publisher has been compensated by2227929 Ontario Inc. to conduct investor awareness advertising and marketing concerning African Gold Group. Inc.2227929 Ontario Inc. paid the Publisher fifty thousand US dollars to produce and disseminate this and other similar articles and certain banner ads.This compensation should be viewed as a major conflict with our ability to be unbiased.

Readers should beware that third parties, profiled companies, and/or their affiliates may liquidate shares of the profiled companies at any time, including at or near the time you receive this communication, which has the potential to hurt share prices. Frequently companies profiled in our articles experience a large increase in volume and share price during the course of investor awareness marketing, which often ends as soon as the investor awareness marketing ceases. The investor awareness marketing may be as brief as one day, after which a large decrease in volume and share price may likely occur.

This communication is not, and should not be construed to be, an offer to sell or a solicitation of an offer to buy any security. Neither this communication nor the Publisher purport to provide a complete analysis of any company or its financial position. The Publisher is not, and does not purport to be, a broker-dealer or registered investment adviser. This communication is not, and should not be construed to be, personalized investment advice directed to or appropriate for any particular investor. Any investment should be made only after consulting a professional investment advisor and only after reviewing the financial statements and other pertinent corporate information about the company. Further, readers are advised to read and carefully consider the Risk Factors identified and discussed in the advertised company’s SEC, SEDAR and/or other government filings. Investing in securities, particularly microcap securities, is speculative and carries a high degree of risk. Past performance does not guarantee future results. This communication is based on information generally available to the public, and does not contain any material, non-public information. The information on which it is based is believed to be reliable. Nevertheless, the Publisher cannot guarantee the accuracy or completeness of the information.

SHARE OWNERSHIP. The owner of Oilprice.com owns shares and/or stock options of the featured companies and therefore has an additional incentive to see the featured companies’ stock perform well. The owner of Oilprice.com has no present intention to sell any of the issuer’s securities in the near future but does not undertake any obligation to notify the market when it decides to buy or sell shares of the issuer in the market. The owner of Oilprice.com will be buying and selling shares of the featured company for its own profit. This is why we stress that you conduct extensive due diligence as well as seek the advice of your financial advisor or a registered broker-dealer before investing in any securities.

FORWARD LOOKING STATEMENTS. This publication contains forward-looking statements, including statements regarding expected continual growth of the featured companies and/or industry. The Publisher notes that statements contained herein that look forward in time, which include everything other than historical information, involve risks and uncertainties that may affect the companies’ actual results of operations. Factors that could cause actual results to differ include, but are not limited to, changing governmental laws and policies, the success of the company’s gold exploration and extraction activities, the size and growth of the market for the companies’ products and services, the companies’ ability to fund its capital requirements in the near term and long term, pricing pressures, etc.

INDEMNIFICATION/RELEASE OF LIABILITY. By reading this communication, you acknowledge that you have read and understand this disclaimer, and further that to the greatest extent permitted under law, you release the Publisher, its affiliates, assigns and successors from any and all liability, damages, and injury from this communication. You further warrant that you are solely responsible for any financial outcome that may come from your investment decisions.

TERMS OF USE. By reading this communication you agree that you have reviewed and fully agree to the Terms of Use found here http://oilprice.com/terms-and-conditionsIf you do not agree to the Terms of Use http://oilprice.com/terms-and-conditions, please contact Oilprice.com to discontinue receiving future communications.

INTELLECTUAL PROPERTY. Oilprice.com is the Publisher’s trademark. All other trademarks used in this communication are the property of their respective trademark holders. The Publisher is not affiliated, connected, or associated with, and is not sponsored, approved, or originated by, the trademark holders unless otherwise stated. No claim is made by the Publisher to any rights in any third-party trademarks.