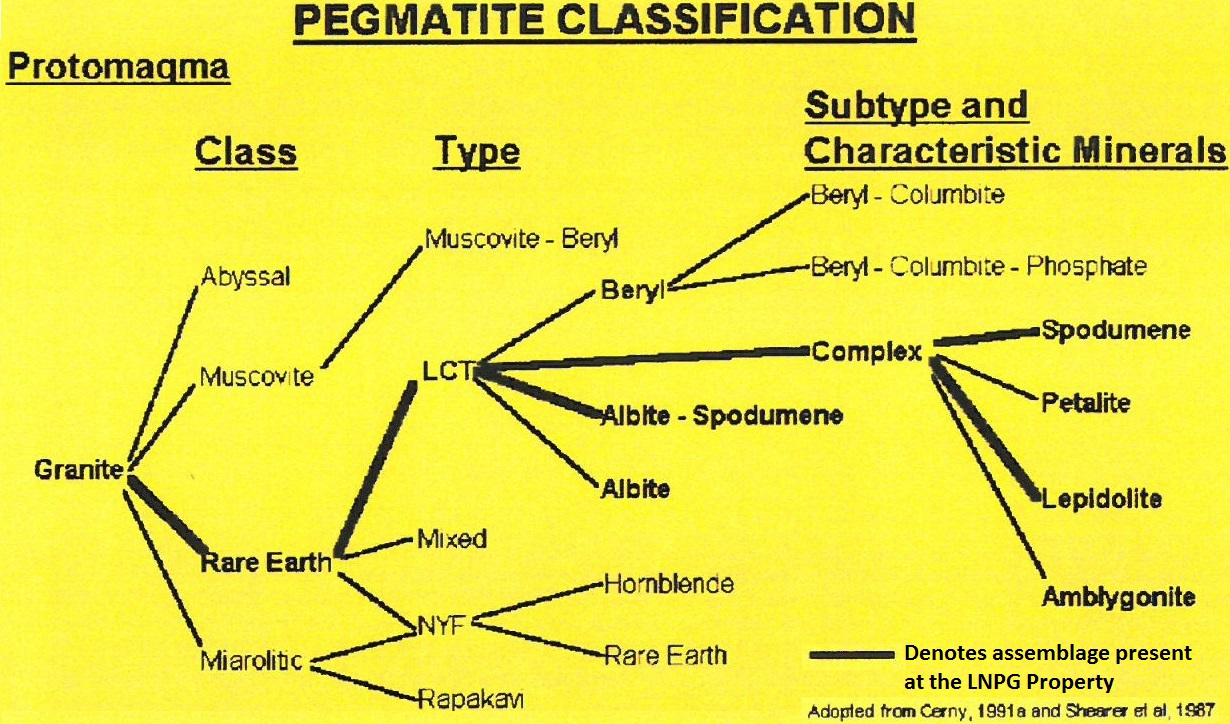

The Greenbushes pegmatites belong to the Lithium-Cesium-Tantalum (LCT) family (source)

Yesterday, Equitorial Exploration Corp. announced the acquisition of the Little Nahanni Pegmatite Group (LNPG) Lithium Project from Strategic Metals Ltd. This property hosts the rare but highly prolific pegmatite-type LCT (Lithium-Cesium-Tantalum), which the world’s largest active lithium mine, Greenbushes in Australia, is also hosting (at an average grade of 2.8% Li2O).

LNPG’s best rock samples from spodumene-bearing pegmatites assayed between 1.74% and 3.77% Li2O. Channel samples returned up to 1.59% Li2O across 10 m. Drilling in 2007 resulted in 2 significant lithium-enriched intervals including 1.2% Li2O over almost 11 m and 0.92% Li2O over 18 m. Hence, this property is already somewhat advanced with significant lithium grades demonstrated at surface with sampling and at depth with drilling.

Strategic Metals has just completed a 2-week program consisting of mapping, prospecting and channel sampling. The program was designed to evaluate grade, size and density of lithium-bearing pegmatites within 4 of the 7 known dike swarms. Results are expected shortly.

Strategic Metals’ compensation for the sale is 7.5 million shares plus 2.5 million warrants of Equitorial, along with a 2% NSR. Thus, Strategic Metals appears to be comfortable in selling this project against equity, whereas Equitorial currently has nearly 53 million shares in the market and as such may control in excess of 10% of the company.

For Android smartphones, an APP (in English) is available from Rockstone Research in the GooglePlayStore.

The Greenbushes pegmatites belong to the Lithium-Cesium-Tantalum (LCT) family (source)

Yesterday, Equitorial Exploration Corp. announced the acquisition of the Little Nahanni Pegmatite Group (LNPG) Lithium Project from Strategic Metals Ltd. This property hosts the rare but highly prolific pegmatite-type LCT (Lithium-Cesium-Tantalum), which the world’s largest active lithium mine, Greenbushes in Australia, is also hosting (at an average grade of 2.8% Li2O).

LNPG’s best rock samples from spodumene-bearing pegmatites assayed between 1.74% and 3.77% Li2O. Channel samples returned up to 1.59% Li2O across 10 m. Drilling in 2007 resulted in 2 significant lithium-enriched intervals including 1.2% Li2O over almost 11 m and 0.92% Li2O over 18 m. Hence, this property is already somewhat advanced with significant lithium grades demonstrated at surface with sampling and at depth with drilling.

Strategic Metals has just completed a 2-week program consisting of mapping, prospecting and channel sampling. The program was designed to evaluate grade, size and density of lithium-bearing pegmatites within 4 of the 7 known dike swarms. Results are expected shortly.

Strategic Metals’ compensation for the sale is 7.5 million shares plus 2.5 million warrants of Equitorial, along with a 2% NSR. Thus, Strategic Metals appears to be comfortable in selling this project against equity, whereas Equitorial currently has nearly 53 million shares in the market and as such may control in excess of 10% of the company.

For Android smartphones, an APP (in English) is available from Rockstone Research in the GooglePlayStore.

Outcropping spodumene-rich pegmatites occur in dike swarms on the LNPG Property

Outcropping spodumene-rich pegmatites occur in dike swarms on the LNPG Property

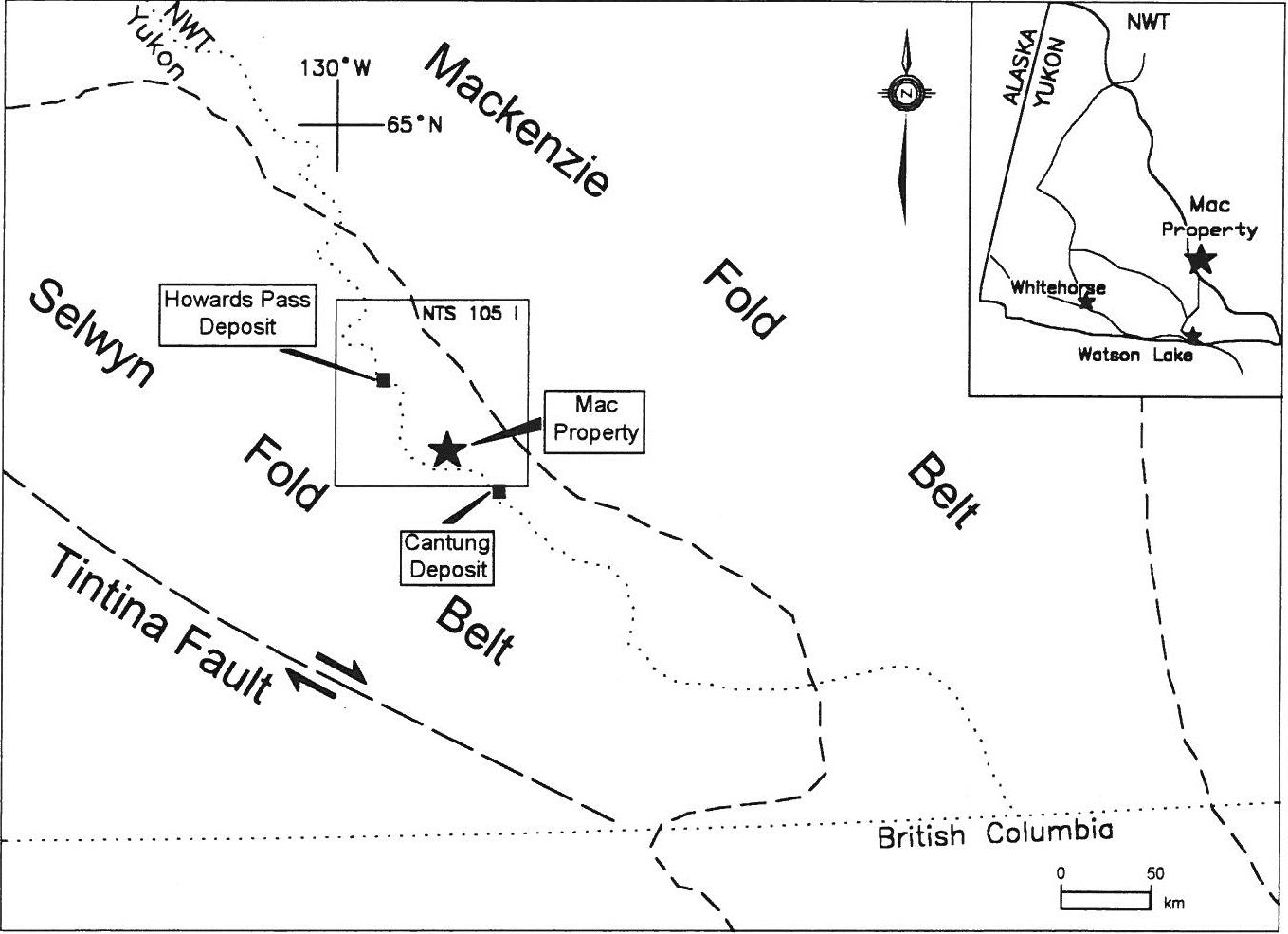

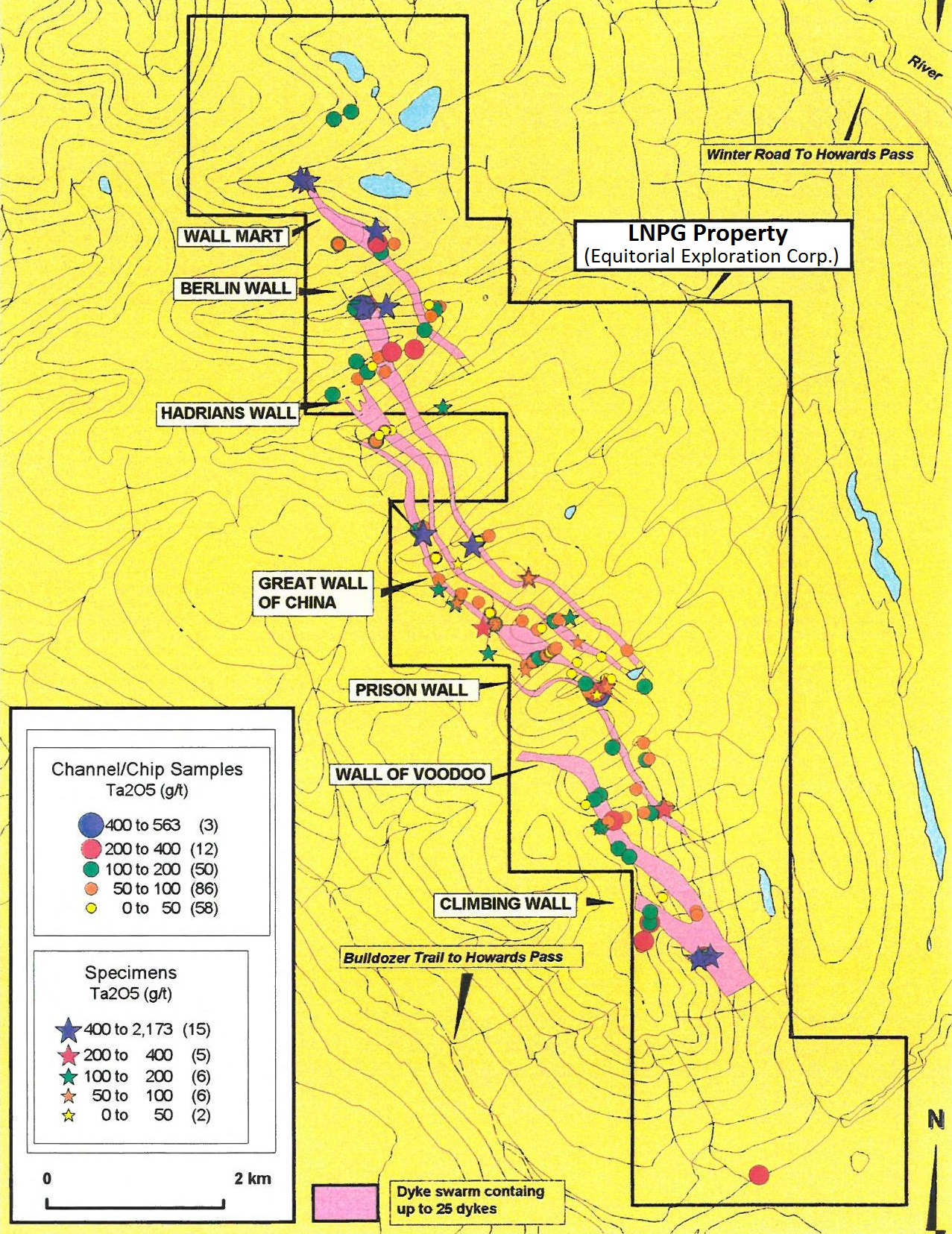

The LNPG Property covers a very large dike swarm (13 x 2.5 km) that is strongly enriched in lithium, tantalum and tin. The property is located 37 km northwest of a recently closed tungsten mine (Cantung). A gated road that extends northwest from Cantung passes within 5 km of the LNPG Property. This road is projected to be the main access road for the Howard‘s Pass Project, one of the world‘s largest undeveloped zinc-lead deposits (Selwyn Chihong Mining Ltd. of China has spent more than $100 million in the last 10 years exploring this deposit and has recently completed a pre-feasibility study).

The area of the LNPG Property was explored mainly during the tantalum boom in the late 1990s and early 2000s. Although lithium is by far the most abundant metal in the dike swarm,

no serious effort was made to evaluate the abundance because brine deposits adequately supplied lithium demand at that time. With increased demand, hardrock mining of spodumene has emerged as an increasingly important alternative source of lithium.

Spodumene is a major component of several of the dikes comprising LNPG. The best channel samples averaged

1.59% Li2O over 10 m, while the best drill intercepts graded

1.2% Li2O over nearly 11 m and

0.92% Li2O over 18 m. However,

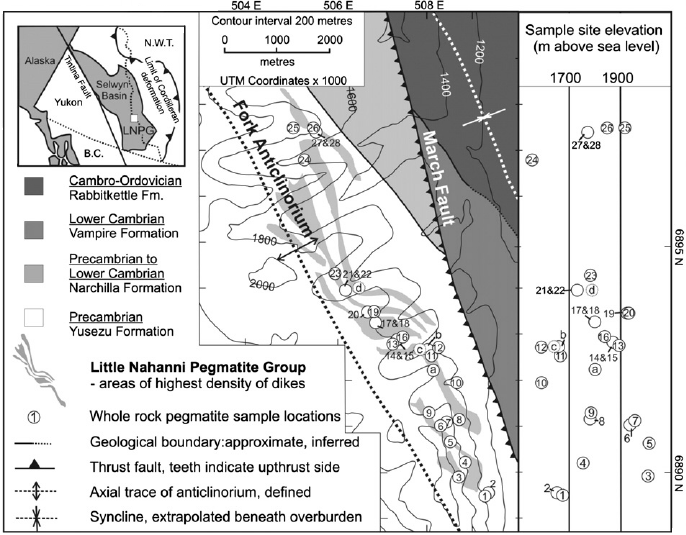

neither the trenching nor the drilling targeted lithium. The dike swarm comprises approximately 200 dikes, some of which are traceable along strike for lengths of up to 5,000 m. The dikes have not been deeply eroded and, based on field measurements, some appear to rapidly thicken or coalesce at depth. Tantalum and tin are potentially significant by-products. Only 8 very widely spaced drill holes have tested the pegmatite system.

Rockstone is excited by this rare but highly prospective LCT-type deposit acquisition and is looking forward to cover the company during its upcoming results from the just completed 2 week program consisting of mapping, prospecting and channel sampling. The program was designed to evaluate grade, size and density of lithium-bearing pegmatite dikes within 4 of the 7 known dike swarms. Based on the results, a drill program will be designed to test the high grade lithium dikes.

Excerpts of USGS‘s publication “A Preliminary Deposit Model for Lithium-Cesium-Tantalum (LCT) Pegmatites“ (2013):

- These [LCT pegmatite] deposits are an important link in the world’s supply chain of rare and strategic elements, accounting for about one-third of world lithium production, most of the tantalum, and all of the cesium (USGS, 2011).

- LCT pegmatites typically occur in groups, which consist of tens to hundreds of individuals and cover areas up to a few tens of square kilometers (Cerný, 1991).

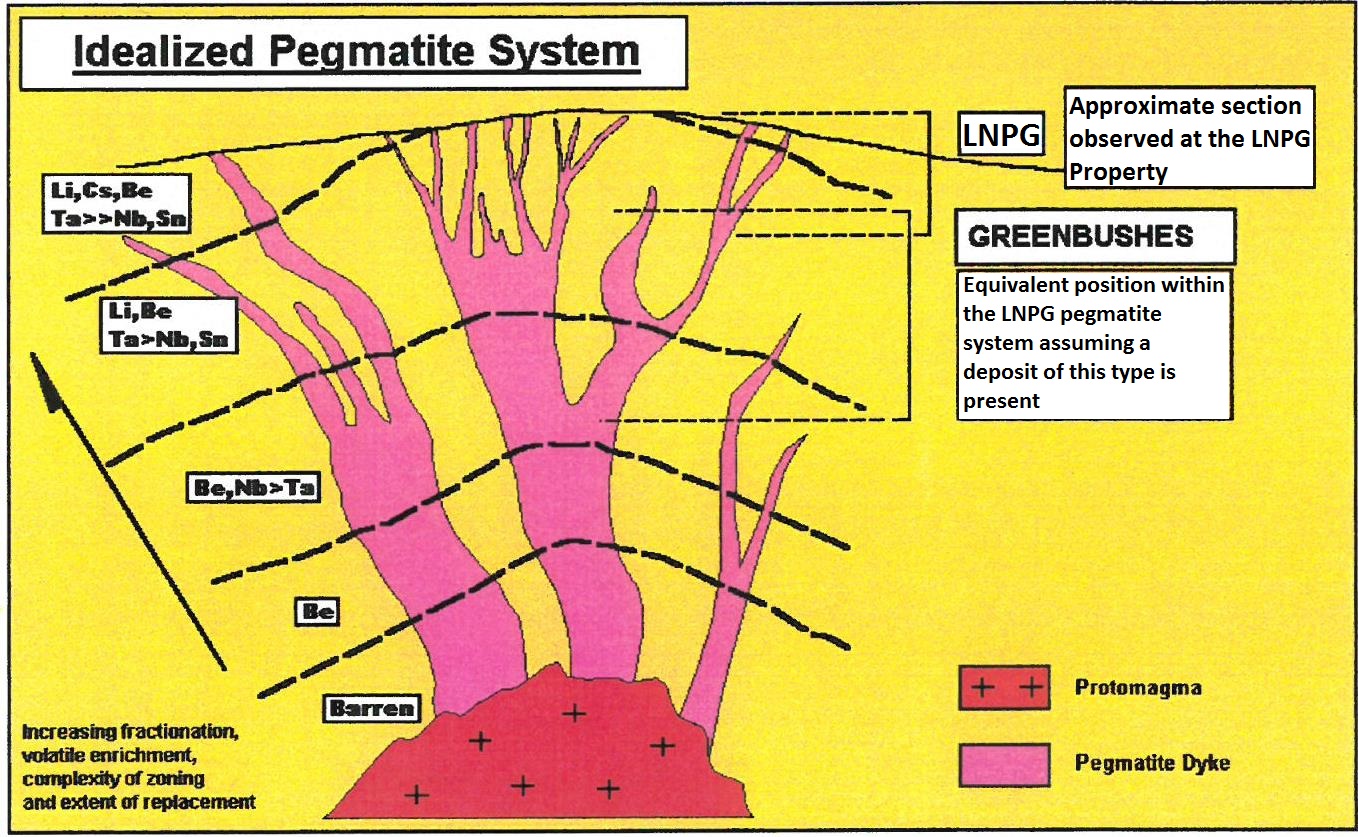

- LCT pegmatites are enriched in the incompatible elements lithium, cesium, tin, rubidium,and tantalum, and are distinguished from other rare-element pegmatites by this diagnostic suite of elements. The melts from which LCT pegmatites crystallize are enriched in fluxing components including water, fluorine, phosphorus, and boron; these reduce the solidus temperature, viscosity, and density while increasing the bulk diffusivity of the melt. Pegmatites can thus form thin dikes and massive crystals.

- Individual pegmatites have various forms including tabular dikes, tabular sills, lenticular bodies, and irregular masses. Even the biggest LCT pegmatite bodies are much smaller than typical granitic plutons. One of the largest and richest pegmatites, Greenbushes, is only 3-km long and a few hundred meters across (Partington and others, 1995). Most LCT pegmatites are much smaller than this.

- Above world map shows selected LCT pegmatites or pegmatite districts of the world. The following tonnages are expressed as million tonnes (Mt) of ore, at the indicated percentages of the oxides of tantalum and lithium, Ta2O5 and Li2O. Giant deposits include Tanco in Canada (2.1 Mt at 0.215% Ta2O5), Greenbushes in Australia (70.4 Mt at 2.6% Li2O), and Bikita in Zimbabwe (12 Mt at 1.4% Li2O). The United States was once a major producer of lithium from pegmatites; among the important districts were King’s Mountain, North Carolina, and the Black Hills, South Dakota.

- The diversity of valid mineral species in the most evolved LCT pegmatites is impressive; at Tanco, for example, 105 minerals have been identified (London, 2008). Huge crystals are another hallmark of LCT pegmatites. The biggest spodumene was 14 m long; the biggest beryl, 18 m; and the biggest potassium feldspar, 49 m (Rickwood, 1982). These are all the more remarkable because pegmatites are believed to have crystallized in a matter of days to years (London, 2008).

- In areas of good bedrock exposure, LCT pegmatites are readily recognized: they are lightcolored rocks with enormous crystals. Granitic pegmatites are relatively resistant and tend to stand above their surroundings.

Photographs from the LNPG Property: A = view to northeast from Cirque 2; B = ?eld setting of pegmatites (dikes ~1 m wide); C = megacrystic minerals with long crystal axes perpendicular to dike/country rock contact; D = mineral banding in dike shown in B, E and F outlined and annotated photographs of a megacrystic dike and pegmatite/aplite banding respectively. (Source)

Photographs from the LNPG Property: A = view to northeast from Cirque 2; B = ?eld setting of pegmatites (dikes ~1 m wide); C = megacrystic minerals with long crystal axes perpendicular to dike/country rock contact; D = mineral banding in dike shown in B, E and F outlined and annotated photographs of a megacrystic dike and pegmatite/aplite banding respectively. (Source)

Hardrock vs. Brine

Production costs from brines are somewhat lower with $2,000-3,000 USD/t, yet with current prices well above $10,000 USD/t, hard-rock lithium mining has become a very lucrative business as well, so far primarily in Australia. Hardrock lithium deposits have the advantage of a short and direct path to production, one that is not influenced by weather or dependent on new technologies that still must prove viability on a commercial scale.

In contrast to lithium brine deposits, hard-rock deposits offer certainty of simplicity and size. On top of that, pegmatites can be moved from an exploration to development project extremely quickly, given the simplicity of a spodumene pegmatite and the volumes of historic information on the methods to process these ore bodies.

Spodumene-bearing pegmatites continue to be an important supply of lithium globally, despite the advent of low-cost production from lithium brine deposits in South America in the mid-1990’s. As the demand for lithium increases, pegmatite deposits around the world are gaining more focused attention as a viable, stable, and long-term supply source. Further, in many lithium pegmatite districts, other rare and specialty-metals have been recovered, including tin, beryllium, tantalum, and niobium which are often associated with spodumene pegmatite deposits.

The world’s largest active lithium mine is the

Greenbushes Mine in Australia, with reported reserves (as of September 2012) of 61.5 million t at 2.8% Li2O. The mine produces lithium from spodumene bearing pegmatite and has been in operation since 1985. In 2015, the global lithium market (in lithium carbonate equivalent or “LCE”) is estimated to have been approximately 171,000 t, for which the Greenbushes Mine accounted for 55,000-60,000 t, or some 35% of the market (source: Deutsche Bank, May 2016).

Joe Lowry, lithium expert and market veteran, recently noted:

“The addition of several new spodumene players (Mt Cattlin, Mt Marion, Pilbara and at least one new player in Quebec) by the end of the decade will continue to increase the hard rock share of the market over the next few years. This is probably a good time to mention a “mini myth” – let’s call it a “sub myth”: brine based lithium is the “best” source of lithium. Yes, lithium chemicals produced from world class brine are lower cost than hard rock based production; however, it is clear that the advantages of spodumene have greatly exceeded the cost disadvantages in recent years. It has been the growth of “high cost” spodumene capacity that has kept lithium supply in balance with demand over the past few years and will keep it in balance with demand over the past few years and will keep it in balance for at least the next three years.”

Comparisons

In past decades, most of the world’s supply of lithium has come from brine sources. However in recent years there has been an increase in demand for lithium, which has resulted in the increased production of lithium from spodumene deposits. A number of spodumene mines are operating or currently under development globally, including

Talison Lithium Ltd., Pilbara Minerals Ltd. and

Altura Mining Ltd. in Western Australia and

Nemaska Lithium Ltd. in Québec, Canada.

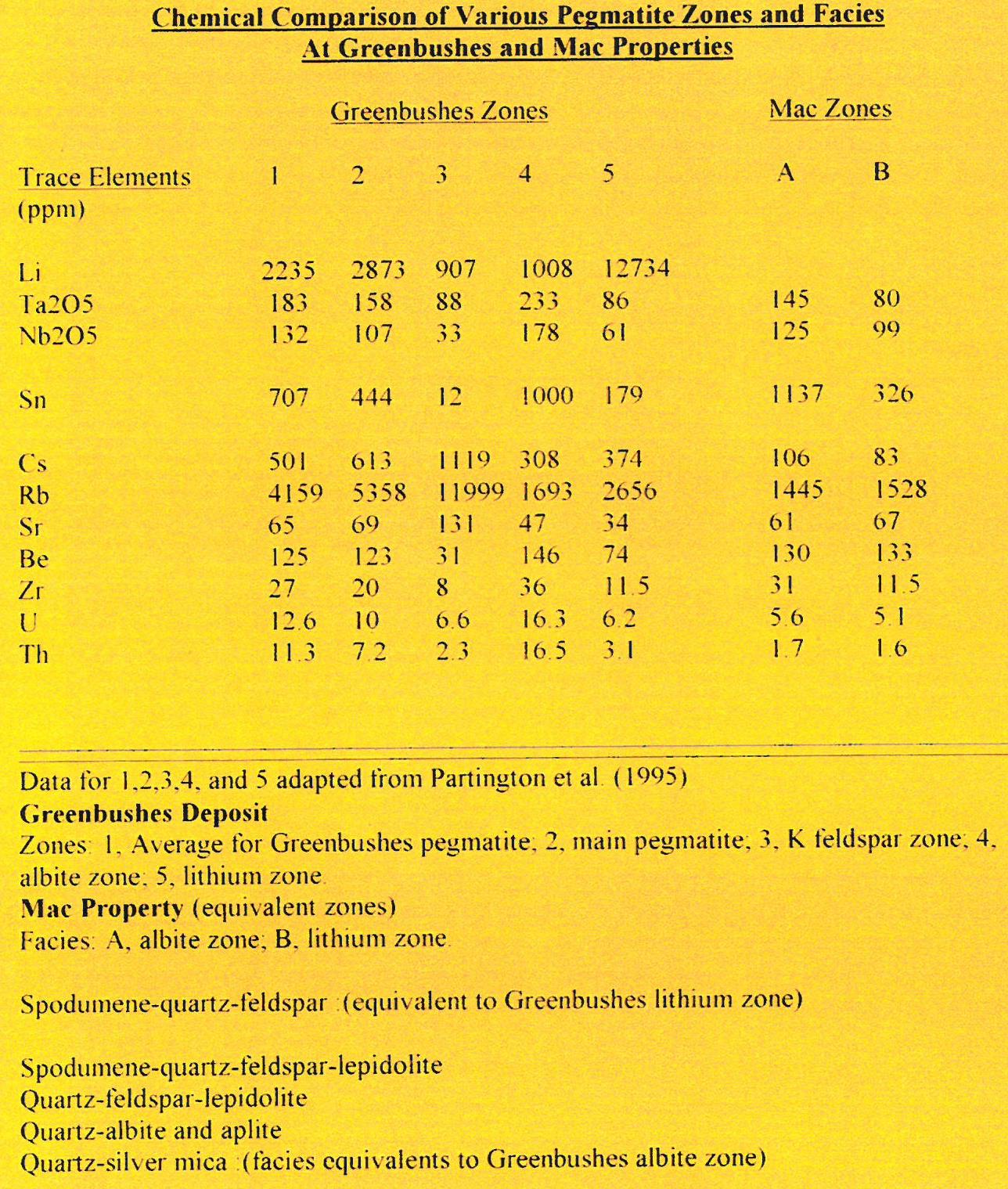

Greenbushes vs. LNPG (formerly known as the Mac Zones/Property):

The

Greenbushes Mine (Talison Lithium Ltd.; acquired by Rockwood/Albemarle and China‘s leading lithium company, Tianqi) has been producing lithium for over 25 years and is the world‘s largest active lithium mine. It produces 315,000 t of lithium concentrate per year. At Greenbushes, the pegmatite consists of a large main zone over 3 km long and up to 300 m wide with numerous smaller pegmatite dikes and pods flanking the main body. The Greenbushes pegmatites are mineralogically zoned in a lenticular interfingering style along strike and down dip. The lithium zone is over 2 km long and enriched in spodumene, which often makes up 50% of the rock.

The

Pilgangoora Lithium-Tantalum Deposit (Pilbara Minerals Ltd.; market capitalization: $557 million AUD) is an emerging Australian strategic metals producer. Pilgangoora contains the world‘s largest new hardrock lithium deposit and the second largest spodumene resource (

indicated +

inferred:

80 million t @ 1.26% Li2O) and one of the largest tantalite resources (

42 million t @ 0.02% Ta2O5 containing 18 million pounds of Ta2O5; assumed recoveries of 47%). Many of the pegmatites are very large, reaching over 1,000 m in length and 200-300 m in width. This globally significant project (open-pitable) is set to become a low-cost supplier of lithium and tantalum for global markets for many decades to come.

Recently, the

Pilgangoora Lithium Deposit (Altura Mining Ltd.; market capitalization: $197 million AUD) has been confirmed as a significant new major discovery (

26 million t @ 1.23% LiO2), ranking alongside the best international hardrock lithium deposits. Production is forecasted to start in Q3 2017.

The

Whabouchi Deposit (Nemaska Lithium Inc.; $344 million CAD market capitalization) has a feasibility study for the deposit and a hydromet plant, revised in January 2016:

Measured:

13 million t @ 1.6% Li2O

Indicated:

15 million t @ 1.54% Li2O

Inferred:

4.7 million t @ 1.51% Li2O

The

LNPG Project (Equitorial Exploration Corp.; market capitalization: $4 million CAD) extends some 13.5 x 2.5 km along the local height of land and comprises of 7 en echelon dike swarms. The 2001 exploration program consisted of geological mapping, prospecting and channel/chip sampling at various locales along the LNPG. The property is located in southwestern NWT, 2 km northeast of the Yukon border and 35 km northwest of the Cantung mine and mill site.

Access: By all season road from Watson Lake via the Robert Campbell Highway. A winter road to Howard‘s Pass is located 2 km north of the LNPG Property. A bulldozer trail passes within 1 km of the southern portion of the claim block.

LNPG‘s regional geological setting: Situated in the Selwyn Basin which is part of the Selwyn Fold Belt. This geological corridor is host to major mineral deposits and prospects (e.g. Cantung and Mactung tungsten deposits, Howard‘s Pass, Tom and Jason lead-zinc deposits). The property is underlain by Upper Proterozoic to Lower Cambrian sediments, locally intruded by granite pegmatite dikes which are termed the Little Nahanni Pegmatite Group (LNPG). The dikes are chemically and chronologically distinct from other intrusions in the region.

Below pictures: The Greenbushes Mine in Western Australia, jointly owned by US-based Rockwood/Albemarle and China’s Sichuan Tianqi Lithium Industries (sources: click on pictures). The pegmatite deposit intrudes along a major northwest regional fault zone. It is approximately 2,525 million years old. The pegmatite consists of a large main zone over 3 km long and up to 300 m wide with numerous smaller pegmatite dikes and pods flanking the main body:

Below pictures: The Greenbushes Mine in Western Australia, jointly owned by US-based Rockwood/Albemarle and China’s Sichuan Tianqi Lithium Industries (sources: click on pictures). The pegmatite deposit intrudes along a major northwest regional fault zone. It is approximately 2,525 million years old. The pegmatite consists of a large main zone over 3 km long and up to 300 m wide with numerous smaller pegmatite dikes and pods flanking the main body:

Company Details

Equitorial Exploration Corp.

Suite 1400 – 1111 West Georgia Street

Vancouver, BC, Canada V6E 4M3

Phone: +1 604 689 1799

Email: info@equitorial.ca

www.equitorial.ca

Shares Issued & Outstanding: 52,752,571

Canadian Symbol (

TSX.V): EXX

Current Price: $0.07 CAD (July 26, 2016)

Market Capitalization: $4 million CAD

German Symbol / WKN (

Frankfurt): EE1 / A14SME

Current Price: €0.035 EUR (July 26, 2016)

Market Capitalization: €2 million EUR

For Android smartphones, an APP (in English) is available from Rockstone Research in theGooglePlayStore.

Disclaimer: Please read the full disclaimer within the full research report as a PDF (here) as fundamental risks and conflicts of interest exist.

FULL DISCLOSURE: Rockstone Research is a Stockhouse Publishing client.